Norwegian pipeline flows are holding steady above the 10-day moving average.

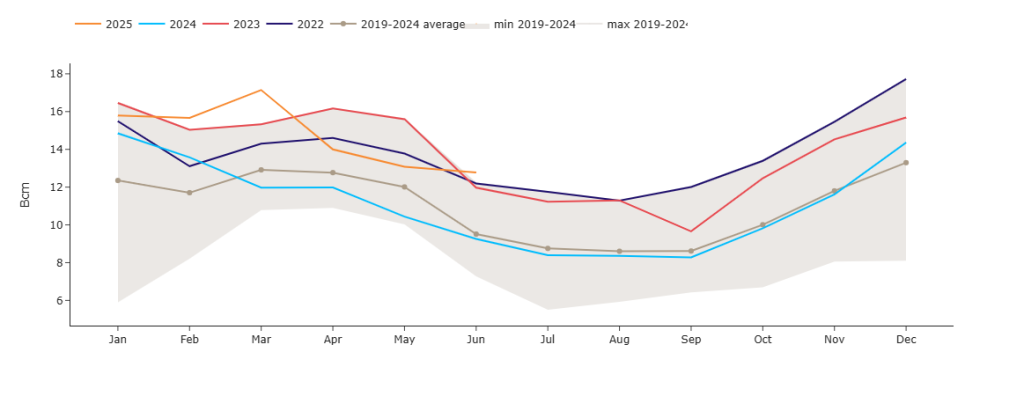

LNG arrivals into Europe are higher at this point in the summer than at any time in the previous 6 years – please see chart below.

The JKM-TTF spread continues to favour European destinations over Asia (JKM is a benchmark price for spot LNG deliveries across Asia, whilst TTF is the major European natural gas trading hub. The spread between these two prices indicates the relative attractiveness of supplying LNG to either destination).

Negotiations between the US and Europe look likely to result in a 15% tariff being imposed by the US on the majority of European imports – so impacts on LNG transit should be minimal.

All in all, it’s as you were – prices are at equilibrium, and whilst it’s difficult to see how markets could fall much further, it’s equally as difficult to see why they might rise abruptly!

That having been said, risk remains that Europe’s efforts to replenish storage in time for Winter-25 will fall short.

However, this looks unlikely, with fullness at 66% verus the 5-year average of 73%.

UK temperatures are set to remain above seasonal norms well into August – renewables outputs should therefore limit gas-for-power burn.

Industrials have been making the most of the steady prices this last week or so, with most having hedged the lion’s share of Winter-25 volumes.

Monthly Day-Ahead averages for the month so far have spent the whole week at 81p/therm (or approx 2.7p/kwh excluding non-gas) – a reflection of very flat near-term risk.

ELECTRICITY & CARBON

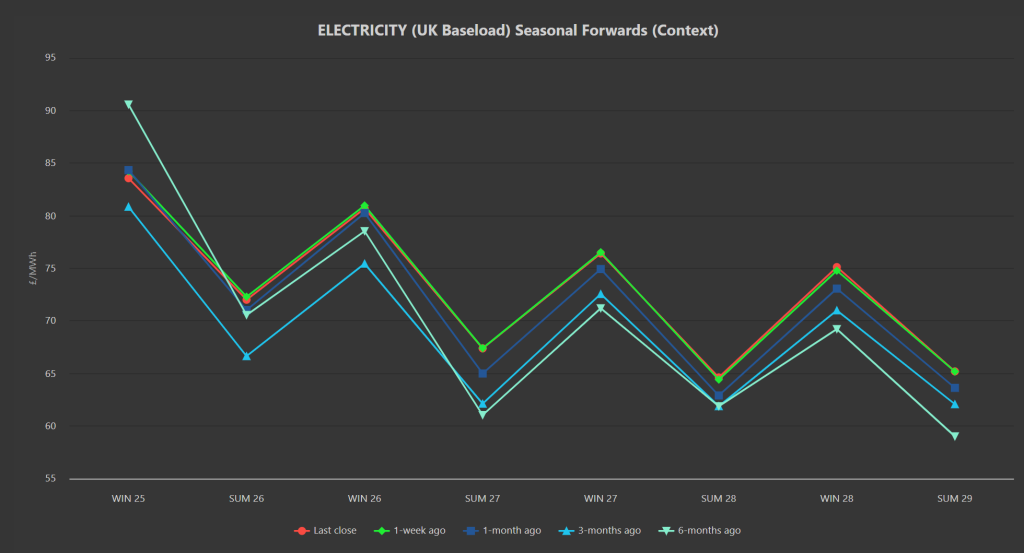

Winter-25 is down versus 1-week/1-month/6-months ago, but still up versus 3-months ago (the Feb lows) – please see chart below.

Winter-25 closes the week at £84/mwh (or 8.4p/kwh).

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are at £50.36/tn on the mid-price.

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 45%, thermal at 15% (gas and coal) and low carbon at 28% (nuclear and imports).

Monthly Day-Ahead averages for the month so far have spent the whole week at £79/mwh (or approx 7.9p/kwh excluding non-energy) – a reflection of very flat near-term risk.