UK NBP gas mirrored European markets yesterday – a little bullish off the back of supply tightness.

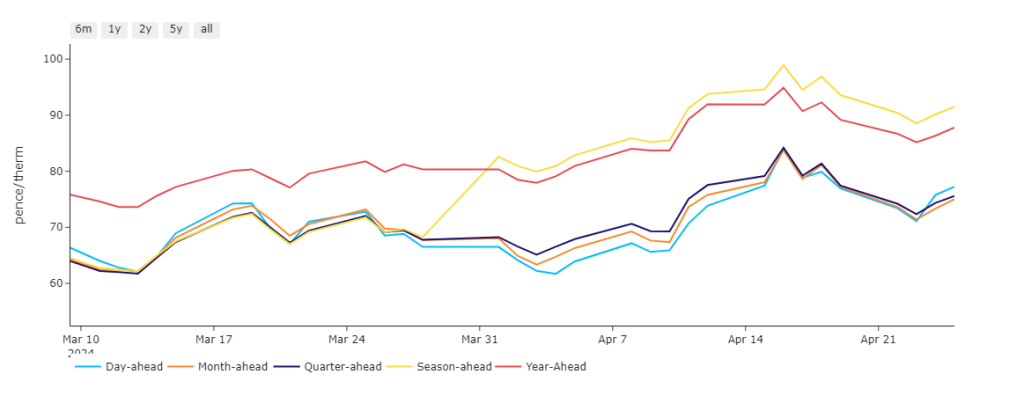

Season-Ahead is at a marginal premium to Year-Ahead, though Day/Month/Quarter-Ahead are at parity and at circa. 17% discount versus Winter-24 (see chart).

However, into the weekend, total demand is forecasted down by 44mcm/d (million cubic metres per day) off the back of rising temperatures and strengthening wind speeds.

Near-term delivery is on the slide today, in the main due to falling demand.

Encouragingly, LNG arrivals to the UK/Europe are circa. 10% above the 30-day average (easing worries over supply).

Unfortunately, production at Freeport LNG remains low with ALL three trains still anticipated to require unscheduled maintenance.

As we reported last week, Freeport looked to have overcome technical problems – however, problems persist.

Geopolitically, there’s very little noise out of the Middle East – be it news of escalation or peace negotiations – as such, risk of another flare up will continue to offer price support.

All in all, a mixed bag – hence the sideways price action.

Monthly Day-Ahead averages are on target this month to achieve 72p/therm (or 2.4p/kwh).

ELECTRICITY & CARBON

Looking to the continent, near-term delivery prices have been supported over the last couple of weeks by temperatures below seasonal norms (increasing heating demand).

It’s interesting to note the geographical differences across Europe – cold in the SW, warm in the NW (centred around the Netherlands).

Prices therefore are easing in the warmer regions.

Windy conditions are expected for the coming week and should be much higher than the seasonal average.

Solar generation is also likely to be high over Central Western Europe – though confidence in a sustained period of renewables outputs is weak – so the benign fundamentals could dissipate rapidly!

On the Carbon markets, EUAs (European Allowances or EU-ETS) continued to rebound yesterday after retesting the €65/tn level on Wednesday (supported by the 20-day moving average).

Back in the UK, Dec-24 contracts for UK ETS are circa. £37/tn.

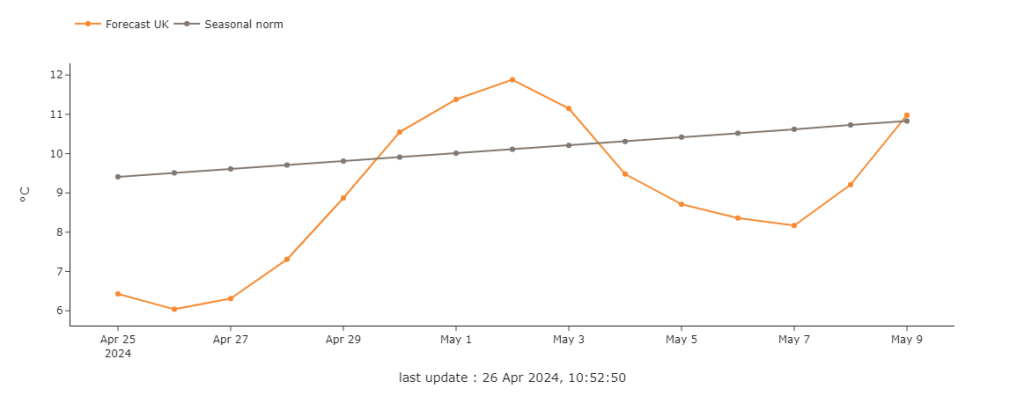

Temperatures are expected back above seasonal norms come 30th April (see chart).

Our electricity generation mix is a little bullish in nature today with renewables contributing 20%, thermal at 36% (gas and coal) and low carbon at 28% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £50/mwh (or 5p/kwh).