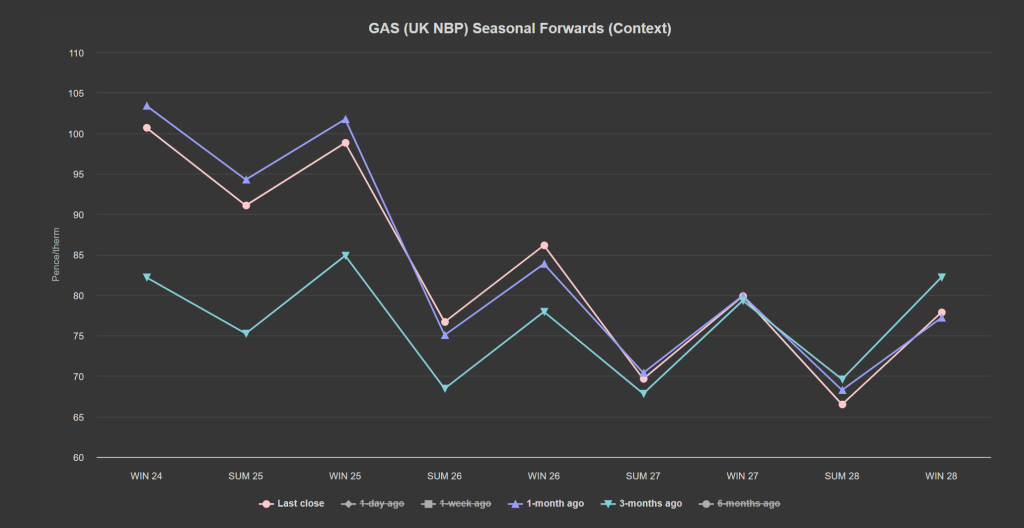

Front-end Seasonal Forwards are now down on the month (though still up versus 3-months ago) – see chart.

With more convincing summer conditions now upon us, not surprisingly, prices have softened to end the week.

Due to higher temperatures, demand is down – and so supply, as a dynamic, is up.

Today, lower gas for power demand is loosening the balance and injections into storage are likely over the coming days if the weather holds as predicted.

On the supply side, the outage at Visund is expected to complete earlier than orginally forecast – which is contributing additional bearish momentum.

The outage at Wheatstone LNG terminal is expected to complete at the end of the month too.

As a further impact of (the long awaited) summer conditioning, solar outputs are expected to see a sharp uptick across Europe/UK over the coming week.

Unfortunately for bears, wind outputs will remain depressed (and below seasonal norms).

European inventories are at 74% versus the 5-year average of 60%.

Norway supplies circa. 30% of Europe’s gas supply.

Notably, daily production throughout 2024 indicates a steady increase y-o-y which is higher than the 2% growth that analysts had predicted.

We’re 81 days into Summer-24 (102 days remaining).

Strong warmth is expected next week – the UK will see temperatures peak at 5 degrees above seasonal norms by Wednesday.

Overall, expect neutral to bearish price action into next week (assuming we don’t see any geo-political threats to supply stability).

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24).

Monthly Day-Ahead averages are on target this month to achieve 83p/therm (or circa. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices only inched up yesterday as forecasts of weaker solar generation in Germany were mostly offset by prospects of slightly strong wind, higher French nuclear generation, lower demand along with fading fuels and emissions prices.

Next week, expected weak wind generation, despite a gradual increase, will contrast with strong solar output.

Additionally, increased nuclear availability in France could further pressure the market.

Down the curve, electricity and emissions prices closely tracked the gas market yesterday – holding for the first hours of trading before dropping off to end the session due comfortable supply and stock levels, particularly from Norway.

Nevertheless, the session confirmed the return of the strong correlation between emissions and gas prices.

On the Carbon markets, prices are bearish today – following the fading gas markets.

Back in the UK, UKAs (UK Allowances) have fallen back more than 10% in the last few days – now trading at circa. £45/tn (Dec-24 benchmark) – having failed to break above the upper extremity of the confirmed price channel, with momentum indicators in overbought territory and rolling over (as predicted in our report last week).

Our electricity generation mix is bearish in nature today with renewables contributing 51%, thermal at 10% (gas and coal) and low carbon at 31% (nuclear and imports).

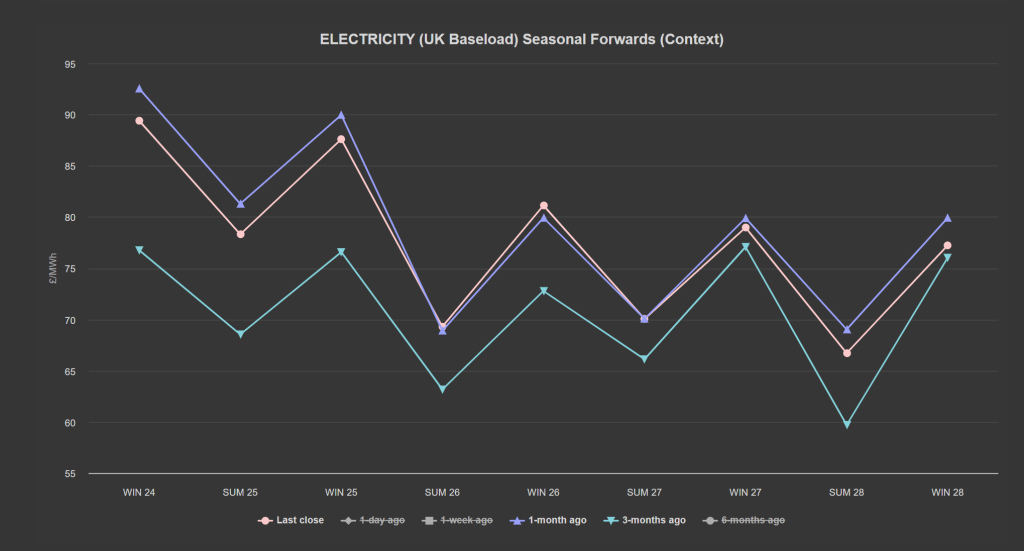

Monthly Day-Ahead averages are on target this month to achieve £71/mwh (or 7.1p/kwh excluding non-energy).