Noise aside, UK prices are little changed versus 1-week ago.

European benchmark prices (TTF) are hovering around both their 20-day moving average and 1-year moving average, reflecting a balanced market – neither bulls nor bears have the upper-hand.

Whilst demand is low due to less heating requirement (off the back of above seasonal norm temperatures), faltering Norwegian flows have limited any potential price downside.

The shadow of US military action looms large across the Middle East – but amid mild weather conditions, traders’ fears over supply problems that will no doubt surface in The Strait of Hormuz (should the US attack Iran) have been suppressed for the time being.

This week has seen fluctuating prices trading in a relatively tight range, with the end of the heating season now on the horizon.

Whilst delivery prices increased on Thursday when it looked like US/Iran negotiations had stalled, any priced-in risk dropped off once it became clear that talks would continue.

In short, markets are steady, and the onset of Summer-26 is now only 32 days away.

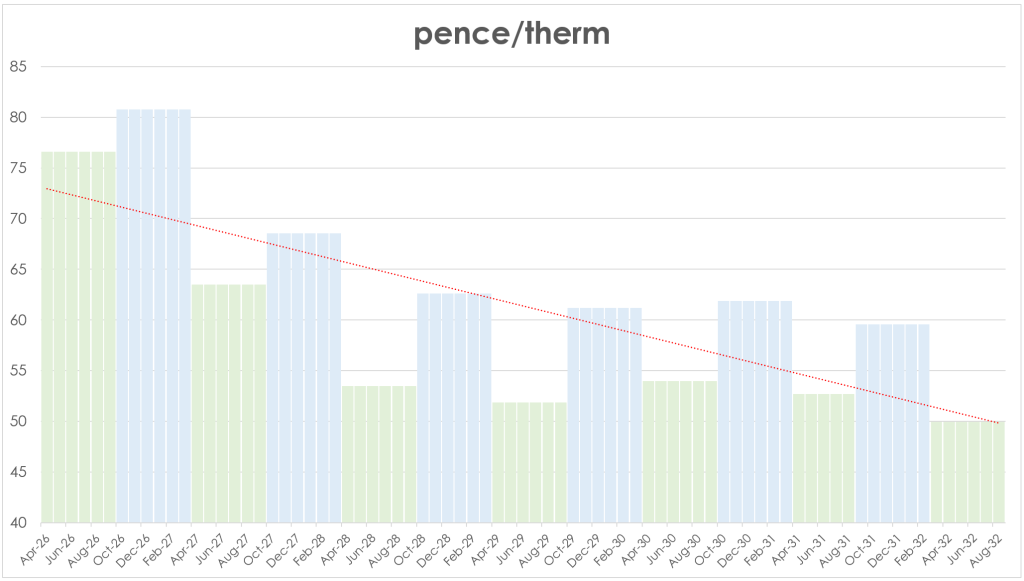

Seasonal Forwards remain steeply backwardated with some great offers further down the curve (Summer-32 is at a 31% discount versus Winter-26) – please see chart below.

As such, on the strategy side, FLEX clients continue to build modest positions further down the curve where comparatively great value persists.

Monthly Day-Ahead averages for February look set to finish the month at 81p/therm (or 2.75p/kwh).

ELECTRICITY & CARBON

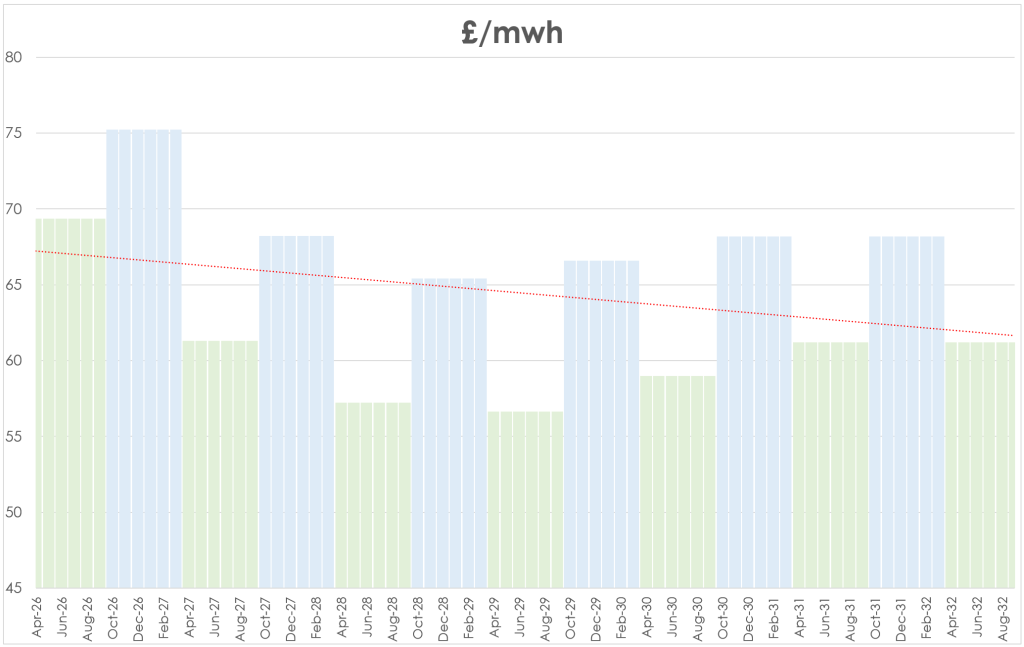

Seasonal Forwards remain steeply backwardated to mid-term (Winter-28), but then rise thereafter out to the end of the curve.

This anomaly likely reflects illiquid trading conditions beyond Winter-28 – please see chart below.

As such, we’d expect for electricity prices further down the curve to improve in-line with gas prices as we draw closer to the onset of summer conditioning, and the end of the heating season.

At the time of writing, Dec-26 UKA delivery is holding steady at £45/tn (down 35% versus mid-January).

Today’s UK electricity generation mix is bullish in nature – specifically, renewables are contributing 19%, thermal at 40% (gas and coal) and low carbon at 21% (nuclear and imports).

Monthly Day-Ahead averages for February are closing the month at £88/mwh (or 8.8p/kwh exc. non-energy).