Markets are treading water following days of tumbling prices.

We’re marginally up versus Wednesday’s lows, as bears reduce their short exposure pending a hoped-for loosening of EU storage targets.

So far though, the EU has only announced flexibility in the “pace” of storage replenishment (with the mandated 90% fullness by 1st Nov ’25 remaining in place until further notice).

As such, market participants were forced to bake-in the according demand for gas (in order for storage operators to hit their targets) – hence the marginal increases this last couple of days.

With Summer-25 now only a month away, temperatures on the continent are set to rise above seasonal norms by the end of the week (easing heating demand and withdrawals).

Summer-25 delivery is down on the week, the month, and 3-months ago (please see chart below).

Unfortunately, the warmer conditions are not expected to be accompanied by decent wind outputs – with renewables generation looking patchy.

On the supply side, Norwegian flows remain strong with no unplanned outages limiting capacity.

LNG outlook is solid with the UK expecting 5 cargoes in the first week of March, and Europe expecting 10 cargoes over the same period.

Nonetheless, the JKM spread (the benchmark comparison showing the prices that Asia is prepared to pay for gas versus Europe) has inevitably grown tighter given recent falls in European/UK prices.

As such, rumours abound that some cargoes originally intended for Europe have followed the money to Asia over the past few days.

Remember though, that Asian buyers are not prepared to buy LNG at any price – if prices rise sharply again, they will reduce their imports (and likely resort to coal for thermal generation etc).

Monthly Day-Ahead averages for this month so far have fallen from the highs in the 2nd week at 137p/therm to 124p/therm to end the month (or approx. 4.2p/kwh excluding non-gas).

ELECTRICITY & CARBON

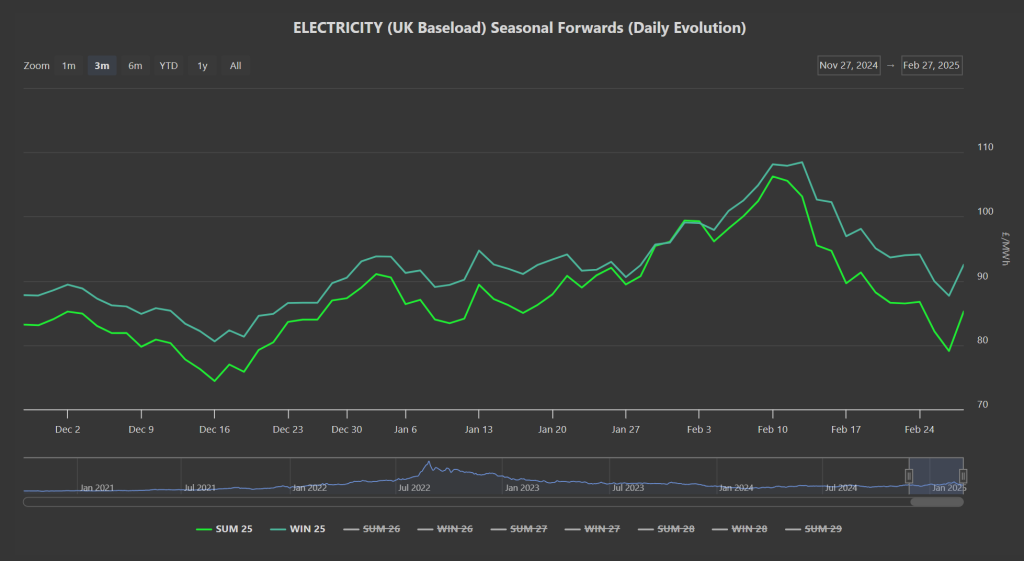

Summer-25 delivery has diverged from Winter-25 nicely (since 10th Feb ’25) with Summer-25 now at a 9% discount to Winter-25 (please see chart below).

The last few days have seen a marginal increase to mirror gas prices (amid poor renewables outputs increasing thermal generation).

Notably, France is working to expand their solar capacity, easing some renewables concerns with summer conditions within touching distance.

This will of course give rise to decent non-thermal generation (even if there is low wind).

The Carbon markets remain closely correlated to fossil fuel prices – so as you’d expect, EUAs and UKAs have been soft over the last few days.

Talk of Starmer’s intentions to merge EUAs/UKAs has gone from the headlines, and UKAs have resumed their bearish bias.

Prices (now at £42.87/tn) have fallen out of the bottom of the long-term bullish trend channel with a new descending channel having been confirmed.

Today’s UK electricity generation mix is bullish in nature with renewables contributing 18%, thermal at 48% (gas and coal) and low carbon at 23% (nuclear and imports).

Monthly Day-Ahead averages so far for this month have fallen from a high of £119/mwh to £106/mwh to end the month (or approx. 10.6p/kwh excluding non-energy).