Both near- and far-term delivery prices traded sideways yesterday, generally closing (very marginally) down on the day.

Fundamental key drivers are mixed, with a two-day extension of the Teesside outage on the bullish side, and on the bearish side, a much looser UK balance is expected next week – enabling storage injections.

Norwegian exports have been rerouted from Europe to the UK, with Vesterled pipeline flows having jumped up by 20mcm/d.

The Teesside outage is likely to complete over the weekend bringing 10mcm/d capacity back online.

Lower temperatures for next week means a higher gas-for-power demand starting Monday (up by 12mcm/d).

All these factors combined should mean our balance will be looser (due to the expected higher Norwegian exports and increased domestic production over the weekend).

This morning, prices are marginally down again off the back of a long system (supply outstripping demand forecast).

Summer conditions have allowed injections into European MRS (mid-range storage) with the latest figure now at 76% versus the 5-year average of 62%.

LNG arrivals to Europe/UK are very thin on the ground with Asia taking the lion’s share to generate electricity for cooling demand – at the time of writing, the UK is only expecting one LNG vessel to degasify in early-to-mid-July.

The scarcity of LNG import is fundamentally supportive – market bears will be hoping to see higher LNG arrivals toward the back-end of Summer-24 (to coincide with the second-half of European/UK scheduled gas maintenance).

Otherwise, withdrawals from storage may be required (subject to weather impacts and associated demand).

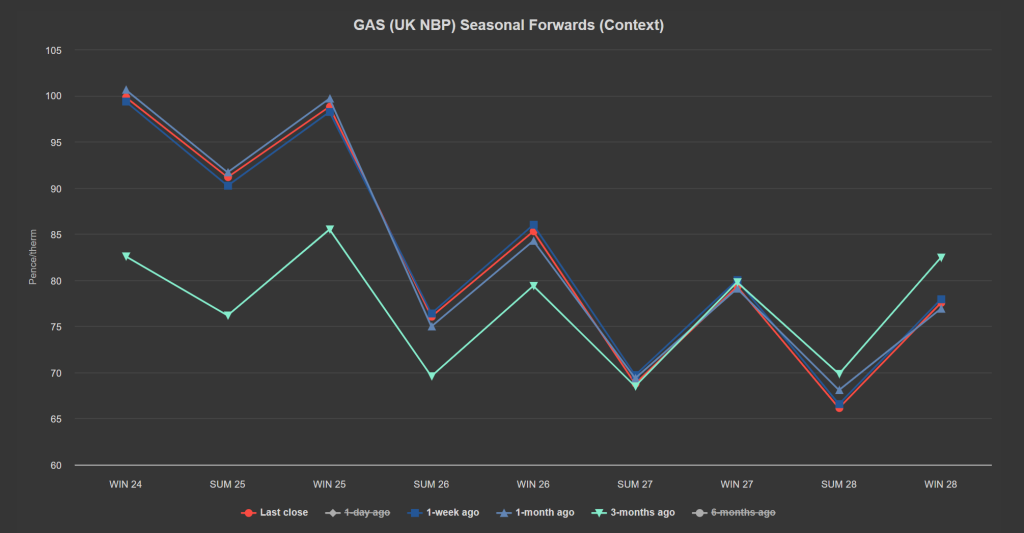

In short, whilst Seasonal Forwards remain up versus 3-months ago, they’re relatively unchanged versus 1-week/1-month ago (see chart).

We’re 89 days into Summer-24 (95 days remaining) with the onset of the 2nd half of Summer-24 only a few days away.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24) – though improved LNG import would ease supply/demand tensions.

Monthly Day-Ahead averages are on target this month to achieve 82p/therm (or circa. 2.8p/kwh excluding non-gas).

Looking to the continent, European near-term delivery prices fell as expected yesterday – driven down by a combined rise of wind and solar generations.

Next week will see mixed fundamentals – weather forecasts point toward stronger wind outputs offset by a drop in solar production early in the week.

Noise aside, fundamental key drivers remain comfortable.

On the Carbon markets, EUAs continued their downtrend yesterday ending the day at 66.67€/t, -0.26€/t from Wednesday.

Prices could now head toward the 60€/t mark driven in the main by speculators progressively building back a significant short position.

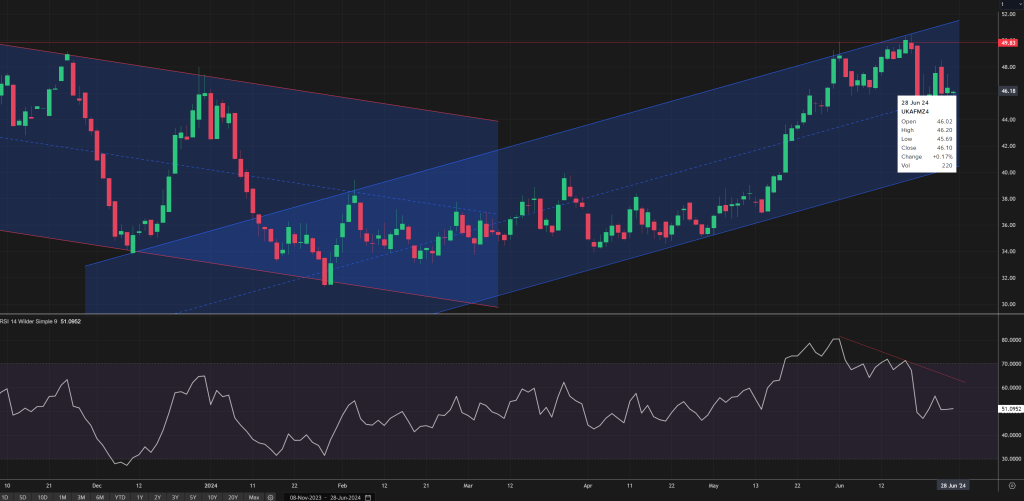

Back in the UK, UKAs (UK Carbon Allowances) followed our prediction that prices were due to fall as indicated by RSI divergence (see chart) – now trading at circa. £46/tonne.

Prices are now in a confirmed ascending trend channel testing the mid-line (see chart) – congestion is building at £40/tn as a strong area of support – so a retest of this level will likely result in a bounce.

Our electricity generation mix is bearish in nature today with renewables contributing 61%, thermal at 10% (gas and coal) and low carbon at 19% (nuclear and imports).

Electricity monthly Day-Ahead averages are on target this month to achieve £71/mwh (or 7.1p/kwh excluding non-energy).