Winter-24 is all but over – with the onset of Summer-25 delivery beginning on Tuesday.

With the heating season now in the rearview mirror, all eyes will be on storage replenishment over the coming months.

European inventories have been holding steady this week at 34% , reflecting a notable slowing in withdrawals against a backdrop of demand below seasonal norms driven by warmer and windier conditions.

So, looking at key drivers – gas for power burn is down; renewables outputs are up; Norwegian flows to Europe/the UK are steady at the 5-day moving average; and 13 LNG arrivals slots into Europe have already been filled for April (following 71 arrivals this month so far, and 9 more expected before month-end – which is up by 60 versus Mar-24).

As you’d expect given the healthy supply outlook, the UK system opened ‘long’ this morning (supply outstripping demand forecast).

Sergey Lavrov (Russia’s foreign Minister) has stated that talks (between Russian and the US) are ongoing around the Nord Stream pipeline as part of efforts to restore normal energy supplies to Europe (though Europe continues to argue against this being a potential outcome).

The minerals deal between the US and Ukraine is still on the table with the US (as of this morning) looking to include natural gas.

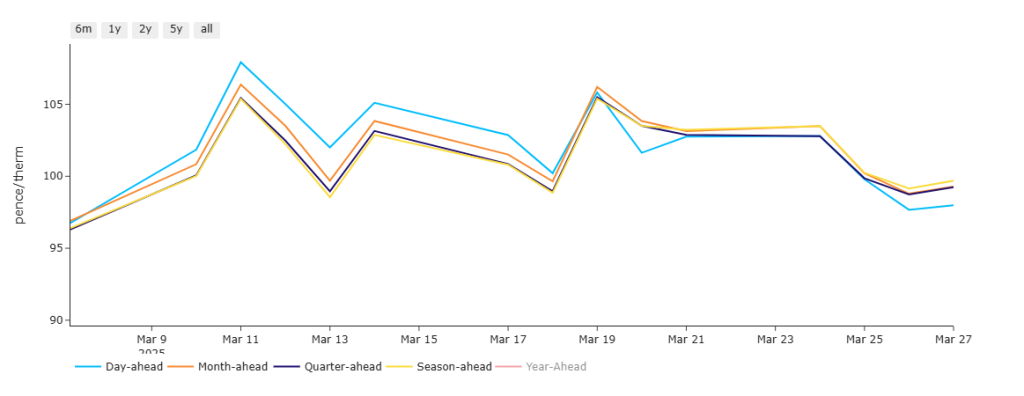

Monthly Day-Ahead averages for this month so far are on track to improve on last month’s final number (124p/therm), with averages holding steady at 102p/therm at the time of writing (or approx. 3.45p/kwh excluding non-gas).

Notably, for the first time since the end of Summer-24, as of 20th March Day-Ahead prices have fallen below Month/Quarter/Season-Ahead – reflecting a “summery” reduction to risk-premium for near-term delivery (please see chart below).

ELECTRICITY & CARBON

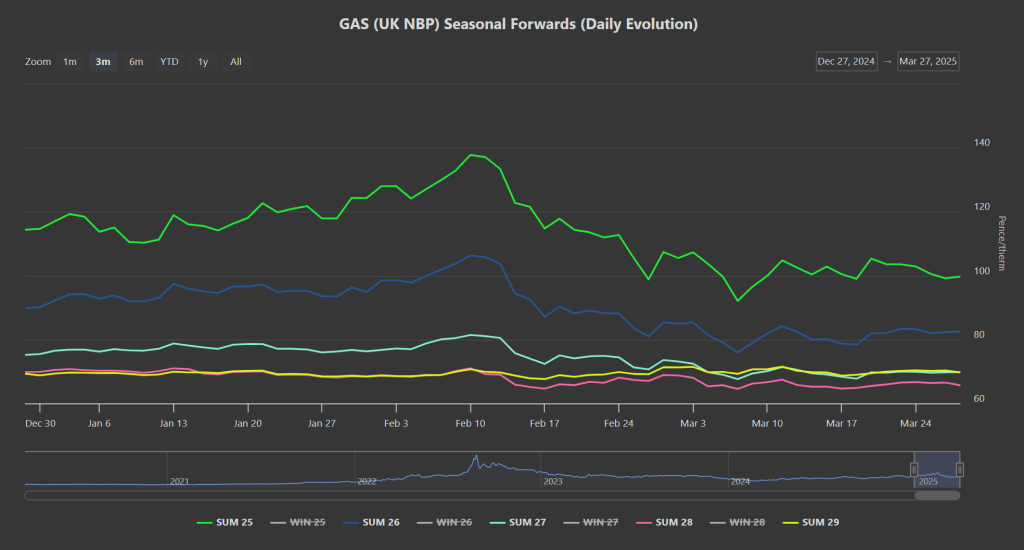

With recent falls in the Summer-26 contract, buyers will be encouraged to note that summer delivery prices down the curve are sub-£70/mwh (or 7p/kwh) beginning Summer-26 (please see chart below excluding winter prices).

As is so often the case (given the UK’s reliance on gas to generate electricity), electricity prices have spent the week tracking bearish gas moves.

Today’s UK electricity generation mix is very bearish in nature, with renewables contributing 63%, thermal at 7% (gas and coal) and low carbon at 22% (nuclear and imports).

On the Carbon markets, UKAs (UK mandatory allowances for heavy emitters) are retesting the upper extremity of a bearish trend channel first formed back on 10th Feb.

Price is now forming a triangle consolidation pattern, with investment funds still net long and seemingly unwilling to concede defeat (and let price fall to reflect falling gas prices).

UK electricity Monthly Day-Ahead averages so far for this month are holding steady below £100/mwh at £91/mwh (or approx. 9.1p/kwh excluding non-energy).