On balance, despite the relentless volatility since the impacts of the US/Israeli offensive began back on 28th Feb, prices are on track to end the week marginally down.

On the bearish side of things, optimism persists that a deal can be reached, and normal transit via the Strait of Hormuz will resume.

On the bullish side, market participants have one big eye on pending supply tightness amid summer pressures to replenish storage in time for Winter-26 (and the heating season, come November).

Right now, it looks as though the ceasefire will be extended for another 60 days.

Accordingly, oil futures have fallen by around 2% today, and look on track for their steepest weekly decline since early April.

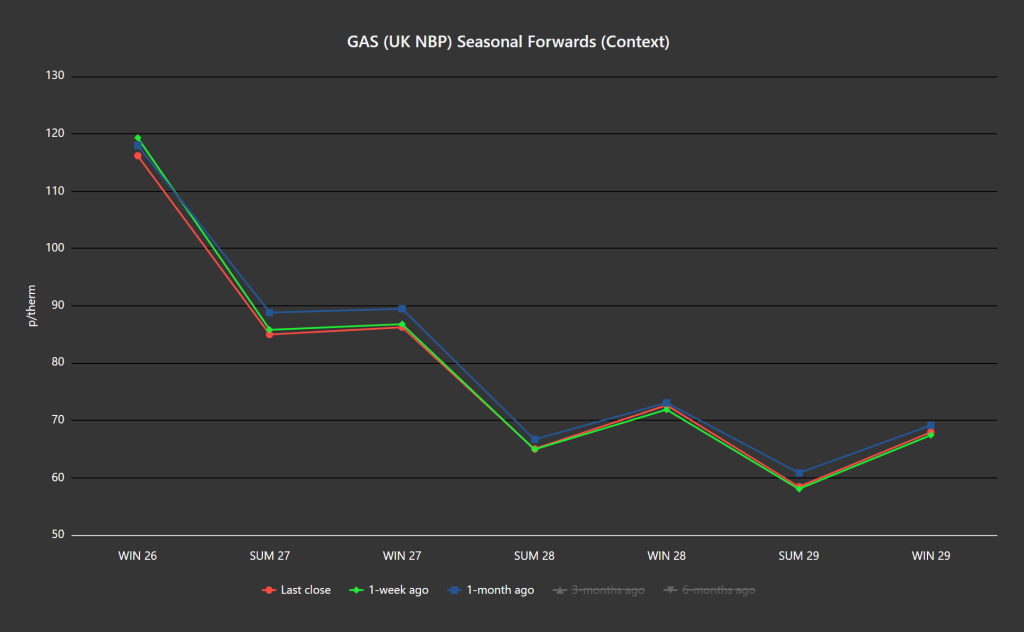

As per the chart below, Seasonal Forwards are barely altered versus 1-week/1-month ago – reflecting that, noise aside, the market is just treading water pending a resolution to the crisis.

On the FLEX side, most clients are now heavily hedged for Jun-26 delivery (so as to mitigate against the Trump Administration’s unpredictability).

Monthly Day-Ahead Averages for the month are holding steady at 117p/therm (or 4 p/kwh exc. non-gas).

ELECTRICITY & CARBON

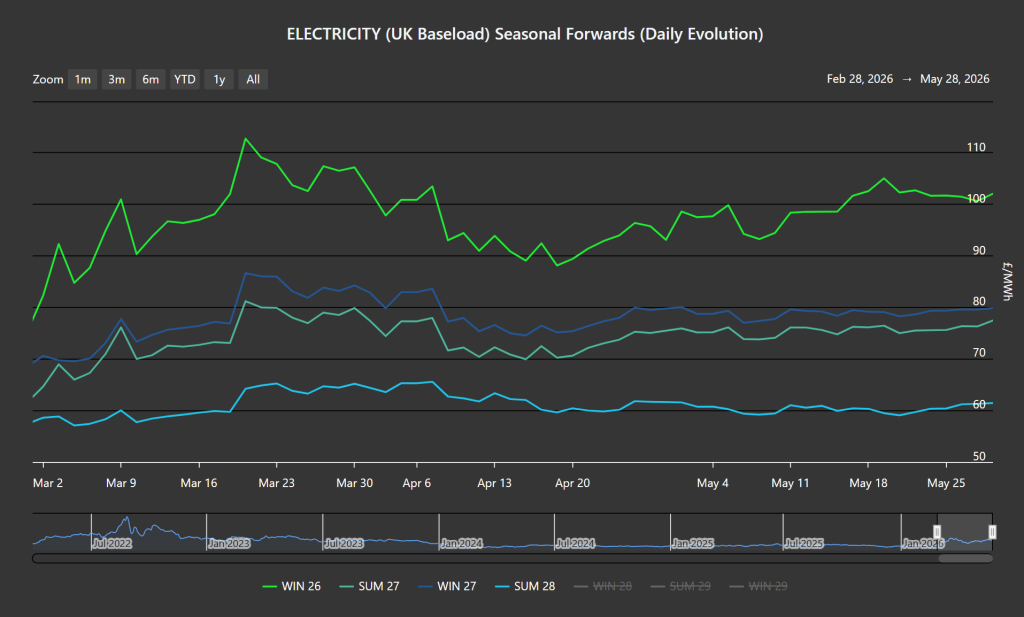

Whilst UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb, nonetheless, the last week has seen front end prices back above the psychological level of £100/mwh.

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 63%, thermal at 8% (gas and coal) and low carbon at 17% (nuclear and imports).

The chart below details the daily evolution of the front 4-Seasons beginning late-Feb.

Summer-28 is at a 44% discount to Winter-26 – reflecting that all the risk remains front-loaded.

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets.

However, correlation shifted to equities throughout March (which continue to enjoy a strong, tech-led upwards momentum).

At the time of writing, UKA mid-price Dec ’26 delivery has sky-rocketed to £58.10/tn (and the spot is at early 57s) amid rumours that the EUETS/UKETS linkage looks increasingly likley (meaning UKETS will need to rise to parity).

On the FLEX side, most clients are now heavily hedged for Jun-26 electricity delivery (so as to mitigate against the Trump Administration’s unpredictability).

Monthly Day-Ahead Averages for UK electricity for May so far are holding steady at £100/mwh (or 10 p/kwh exc. non-energy).