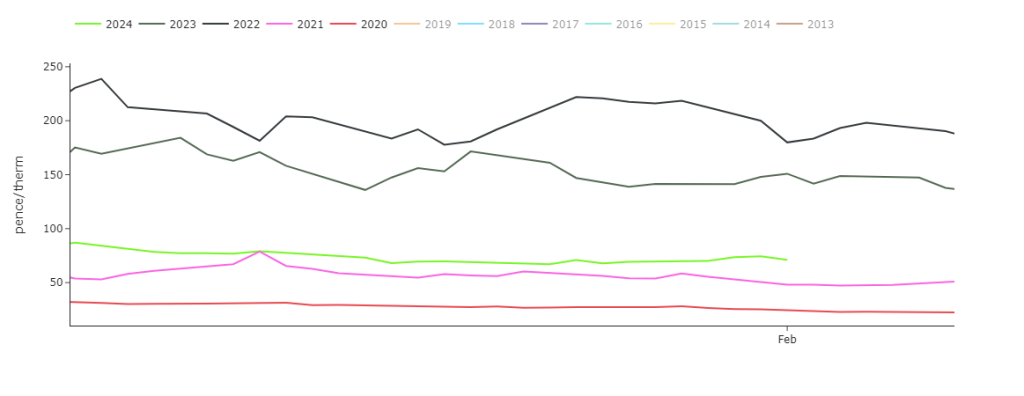

Looking at the bigger picture, Month-Ahead prices are now within touching distance of those printed at this time of year in 2021, and way below those printed in 2022 & 2023 (see chart).

It’s been another day of sideways price action, with contracts all the way down the curve neutral (with just a little downside bias).

Prices remain soft off the back of wet and windy forecasts for most of February – though temperatures may fall below seasonal norms toward the end of the month.

For the first time in a week, the UK system was long at open (supply outstripping demand).

Whilst conditions are overwhelmingly bearish, prices are supported at prospects of a cold spell at the end of the month and ongoing geopolitical risk across the Middle East.

Notably (and bizarrely), LNG coming out of Russia finding its way to European ports, has risen m-o-m to its highest level since March-22!

European gas stocks remain at historically high levels (70% versus 5-year average of 55%).

Monthly Day-Ahead averages are on target this month (so far) to achieve 69p/therm (or circa. 2.35p/kwh).

ELECTRICITY & CARBON ALLOWANCES

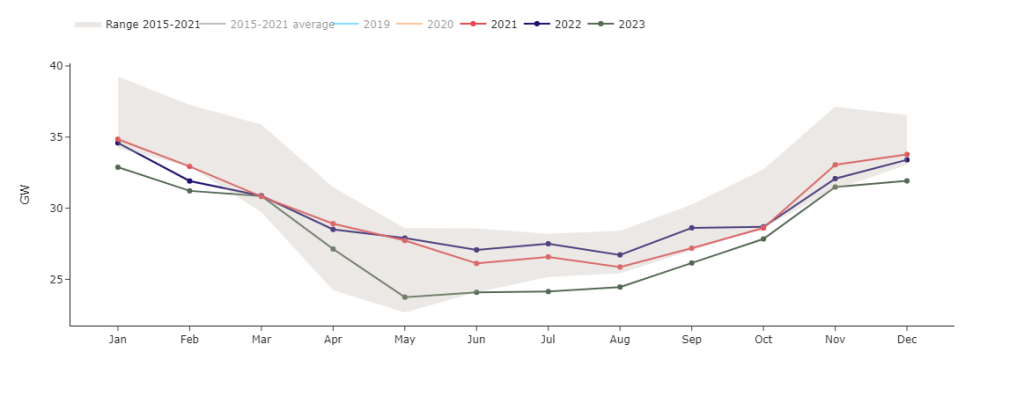

Monthly UK average power load shows demand at the lowest levels for 9 years (see chart).

Looking to the continent for signals, we’re seeing flip-flopping weather forecasts indicating warm and (very) windy in the short-term then cold and wet into the latter half of the month.

Short-term wind outputs are likley to pressure prices close to zero over the weekend – most likely falling into negative values on Sunday.

Down the curve, there’s been little change all week with the bearish momentum having run out of steam for the time being.

On the European carbon markets however, the Dec-24 benchmark has been dragged lower by short term windy weather dropping residual load on the power markets across NW Europe.

Back in the UK, UKAs have spent all week correcting northwards following Monday’s record low (£31.30/tonne) – at the time of writing, we’re back above £38/tonne.

Of course, this reversal in price is most likely caused by the sheer value on offer at these levels – lest we forget, back in Aug ’22, Dec-24 delivery was printing above £100/tonne!

Notably, the EUA versus UKA premium has dropped to just over £15/tonne – the lowest since July 2023.

Our generation mix today is very bearish – 53% renewables and only 8% gas-for-power burn.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £56/mwh (or 5.6p/kwh).