Month 4 (of 6) of Winter-24 draws to a close on a bullish note.

Primarily front-end prices have been driven up this week by unscheduled Norwegian outages, forecasts of cold spells in Europe for early February, and sustained withdrawal depletion giving rise to fears of stock replenishment in time for the onset of Winter-25 – please see monthly Forward chart below.

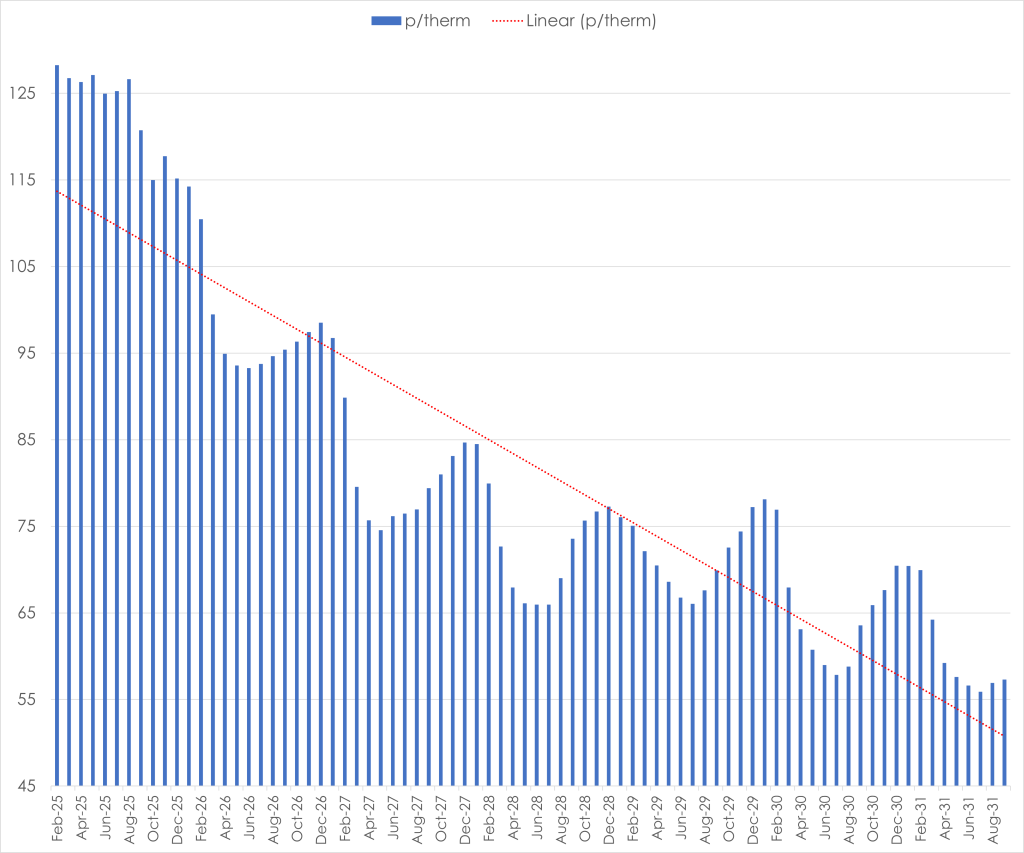

As such, the risk-premium at the front of the curve means the comparative value on offer at the back is at nearly a 60% discount – wintry conditions indeed.

So are we in for more of the same over the next couple of months in the run up to Summer-25?

Well, even though European LNG imports are increasing (to counter the increased demand caused by wintry conditions), the market evidently wants to price in the risk that China LNG imports (currently down) may increase after the Lunar New Year holiday (29th Jan to 4th Feb).

Notably, rumours swirl around the corridors of the European Commission (according to an FT article) that Russian gas may resume flows through Ukraine as part of peace talks – of course, were Russian flows to return to Europe as a whole in the event of a wider agreement engineered by Trump, then European prices would fall off a cliff – nonetheless, the European Commission was careful to reiterate yesterday that it would continue with its plans to phase out Russian gas imports from Europe’s energy mix by 2027.

The benchmark Asia JKM prices remain down (-0.49% for Mar-25 delivery prices to €46.72/MWh), which has further widened the spread against European prices and maintains Europe as the preferred destination for LNG spot cargoes (the Japan Korea Marker (JKM) is a price index LNG across Northeast Asia reflecting the values delivered to Japan, South Korea, China, and Taiwan).

Winter is always a difficult time for I&C buyers as they eye hedges for the coming seasons – right now, storage levels at 55% are just below the 7-year average which is why Summer-25 delivery has been made more expensive than Winter-25 delivery as lots of gas will need to be secured over the Summer-25 period to ensure the mandated requirement of 90% fullness is achieved by 1st Nov-25.

Certainly, hedging now would mean settling for high prices before the full impact of summer conditioning is felt.

As such, buyers are waiting on the sidelines to see how things develop over the coming weeks (though as the chart below clearly shows there’s still plenty of comparative value on offer beginning Summer-26).

Monthly Day-Ahead averages for this month so far are at 122.620p/therm (or approx. 4.184p/kwh excluding non-gas) – the average having remained at or above 120p/therm for the entire month.

ELECTRICITY & CARBON

European electricity markets have been bullish this last few days off the back of declining renewables generation forecast for Feb.

This reduction and the expected pick up in demand due to falling temperatures will inevitably result in an increased reliance on gas for power burn across Europe – though it’s likely that much of this risk is now priced-in.

Contrary to UK gas markets, Winter-25 electricity prices remain at a traditional premium to Summer-25 (though the shape is flattening to increasingly mirror the currently skewed/backwardated gas curve shape).

However, thereafter, Seasonal Forwards beginning Summer-26 remain at a significant discount.

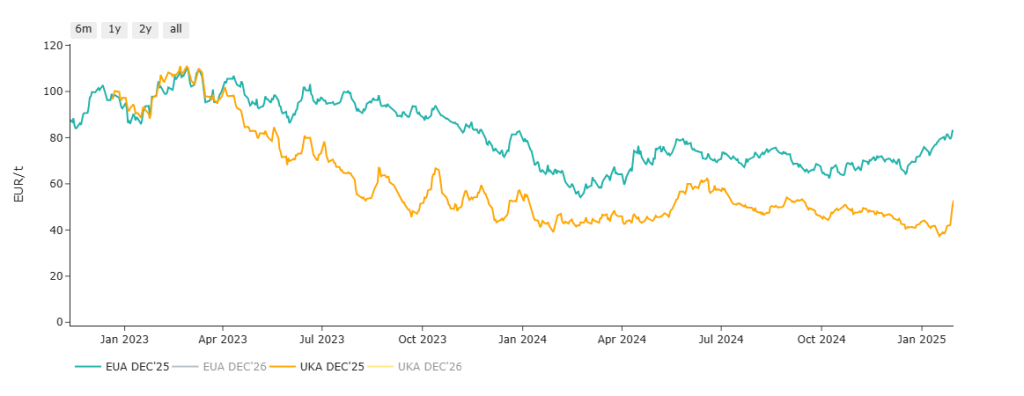

On the carbon markets, UKAs went on a rally following Keir Starmer’s comments in the FT that EUAs and UKAs should be combined to form one market – prices still remain inflated having risen 30% to £45.05/tn from their lows of £31.87/tn back on 17th Jan-25.

No doubt making the unpopular UK PM even more unpopular with UK heavy emitters who were quite happy with the status quo prior to Starmer’s comments (given that UKAs have been at a discount to EUAs since late Mar-23 (please see chart below detailing comparative values for Dec-25 UKA delivery).

Today’s UK’s electricity generation mix is very bullish/price supportive with renewables contributing 15%, thermal at 53% (gas and coal) and low carbon at 17% (nuclear and imports).

Monthly Day-Ahead averages for this month so far are at £118.060/mwh (or 11.81p/kwh excluding non-energy) – the average having stayed stubbornly above £100/mwh since week 2.