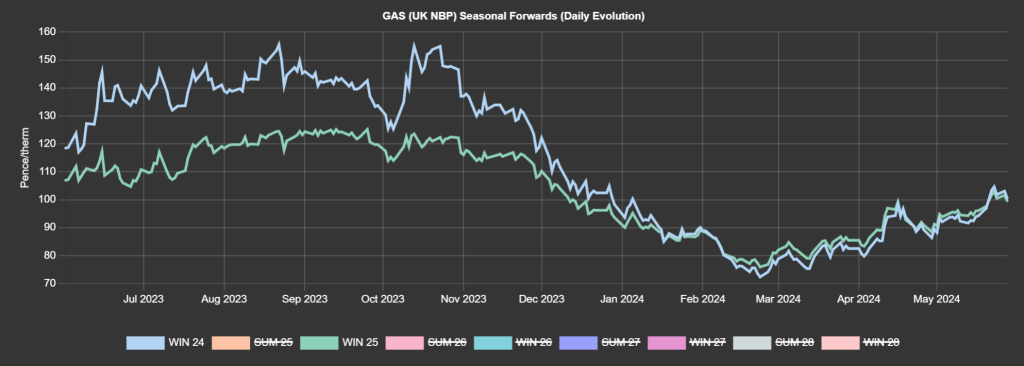

Having been at significant divergence throughout the second half of 2023, Winter-24/Winter-25 returned to parity in early 2024 and have been tracking gradually northwards in unison since the onset of Summer-24 (April) – see chart.

Prices for Winter-24/Winter-25 delivery broke through the psychological resistance level of 100p/therm on 22nd May ’24, and are hovering above to date – supported by a poor LNG arrival schedule, ongoing scheduled/unscheduled outages/maintenance and as yet unconfirmed supply risks to Austria (and potentially other European countries – at the hands of Gazprom).

Bullish drivers are being offset by strong renewable outputs across Europe and yesterday’s confirmation from Brussels that Germany has scrapped a levy on transit gas – which should see increased imports into neighbouring central and eastern European countries.

Also, high MRS (European storage at 69% versus the 5-year average of 52%) and reduced consumption are keeping a lid on any upside momentum.

At the time of writing, the UK system is balanced with below than average seasonal demand.

Although temperature forecasts have shifted lower overnight, with temperatures now expected to outturn to fall below seasonal norms for the majority of next week.

On the geopolitical side, continued conflicts in Russia and the Middle East (and associated worries over supply security) remains supportive.

On the supply side, recent outages to Freeport LNG (US) and Gorgon LNG (Australia) have disrupted global supplies throughout the week.

This was down to a combination of mechanical faults (with one of the three trains at the Gorgon facility) and reduced Freeport LNG production (down to 81%) due to power cuts.

Rising Asian LNG prices also remain supportive.

Consensus remains that Europe is on track to achieve 100% storage levels by Winter-24 (early Oct ’24).

Monthly Day-Ahead averages for May achieved 76p/therm (or circa. 2.6p/kwh excluding non-gas).

With 122 days of Summer-24 remaining, clients are beginning to look at scaling-in Winter-24 open volumes.

ELECTRICITY & CARBON ALLOWANCES

Looking to the continent, European short-term delivery prices eased to end the week, weighed by prospects of increases to hydro and wind generation (notwithstanding firmer fuels and emissions prices).

Next week, an expected rebound in solar production and French nuclear availability should keep the Day-Ahead market under pressure, although lingering weak wind outputs may offset a slight part of the weight.

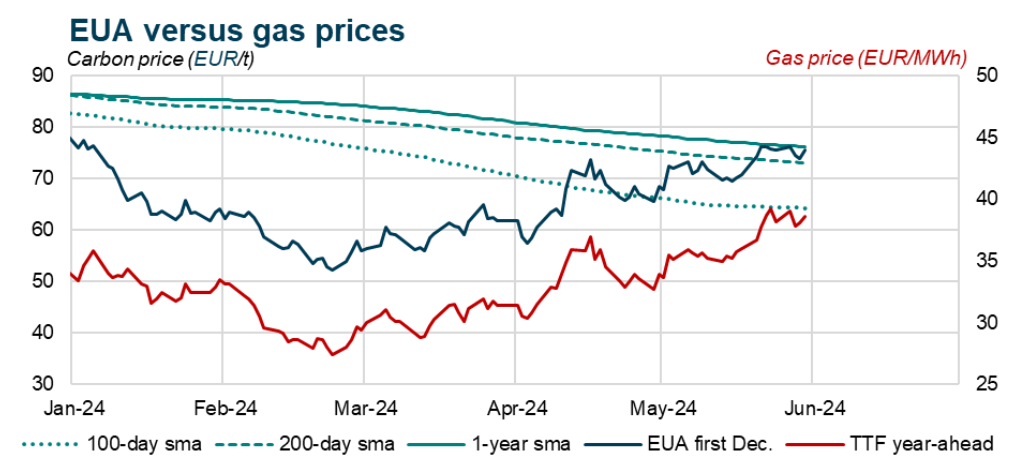

On the Carbon markets, prices continue to track the gas market (see chart).

Back in the UK, UKAs (UK Allowances) are still on a bull run – now trading at circa. £48/tn (Dec-24 benchmark) – having broken above the highs printed on 25th Mar ’24 and having breached overhanging resistance trendlines.

Our electricity generation mix is bearish in nature today with renewables contributing 49%, thermal at 8% (gas and coal) and low carbon at 29% (nuclear and imports).

Monthly Day-Ahead averages for May achieved £72/mwh (or circa. 7.2p/kwh excluding non-energy).