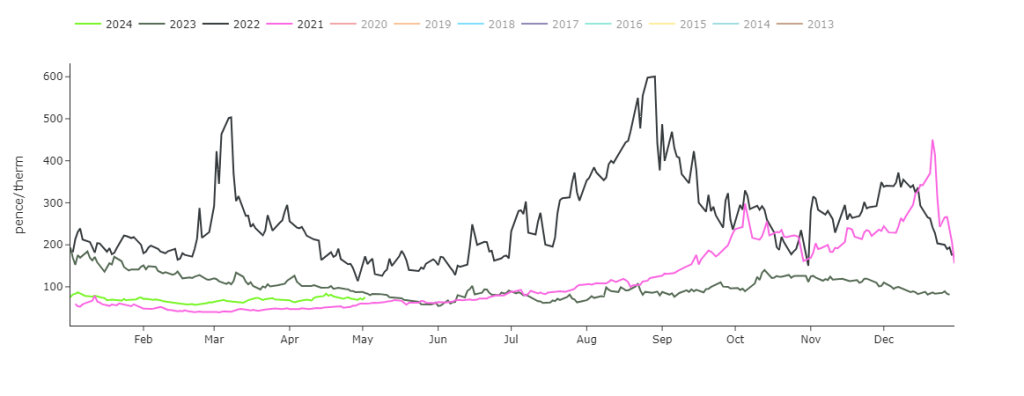

Month-Ahead prices so far for 2024 are comfortably below 2023, way below 2022, and marginally above 2021 (see chart).

Prices are up today off the back of supply tightness due to the Ukrainian conflict threatening the remaining imports from Russia into North Western Europe.

Shipments are down 6% m-o-m.

Russia’s targeted attacks of Ukraine’s energy infrastructure and gas storage is also heightening concerns that excess supplies will not make it into Europe during Winter-24.

Offering additional bullish momentum, Asian LNG prices rose this week on forecasts for higher cooling demand over the coming summer.

This most recent price rally is also underpinned by the potential impacts of Middle East tensions as well as weakness in U.S. feedgas demand (natural gas that’s delivered for liquefaction via pipeline to be converted into LNG).

Demand forecast is marginally up today, with a small increase in heating consumption and higher gas-for-power burn due to lowered wind outputs.

Norwegian flows to the UK/NW Europe remain in good shape and are still above the 5-day moving average – notwithstanding the ongoing seasonal scheduled outages at Aasta Hansteen, St. Fergus and Kollsnes gas fields.

European MRS (mid-range inventories) have enjoyed a little injection, now at 63% versus the 5-year average at 43%.

In short, markets still have the jitters, and whilst lower temperatures and patchy wind outputs persist, there’s no appetite amongst market participants to take the market lower.

In these conditions, any bullish driver (no matter how insignificant) moves the market disproportionately higher.

Monthly Day-Ahead averages for April achieved 74p/therm (or 2.5p/kwh).

ELECTRICITY & CARBON

Looking to the continent, short-term delivery electricity prices rebounded yesterday.

Whilst wind outputs have revised upwards for this coming weekend, they still look set to be below seasonal averages today and throughout next week.

Solar looks patchy still despite a warm bias forecast for next week, but the outlook looks chilly thereafter – limiting the bearish impact of short-term temperature increases.

As such, residual loads (the remaining demand for electricity that cannot be covered by wind and solar power) will likely remain elevated until the end of next week, supporting prices and increasing thermal generation (gas and coal burn).

Down the curve, prices are up again though the move could fairly be regarded as overcooked amid still dampened demand and recent renewable overperformance.

On the Carbon markets, we saw a strong move upwards on the EU-ETS (European Mandatory Allowances) yesterday off the back of strong auction interest and forecasts of weaker renewables outputs – with prices achieving a 2-week high.

Breaking the psychological €75/tn level to the upside will likely open the door to an extended bullish rally.

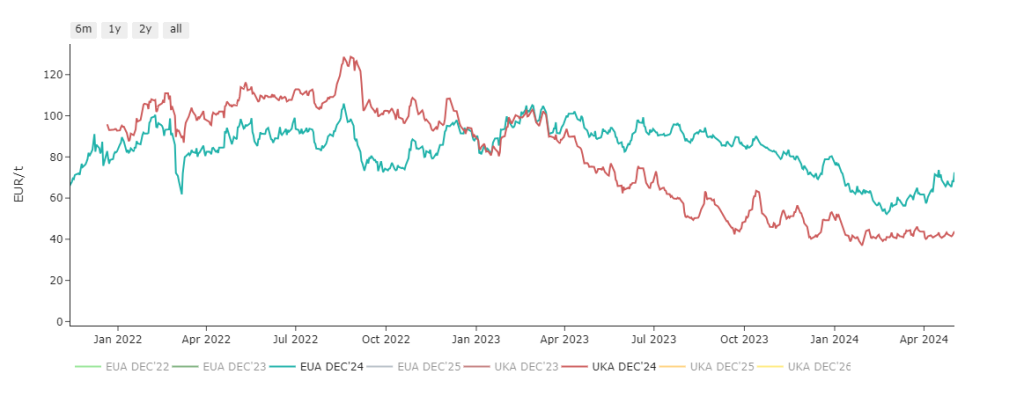

Back in the UK, Dec-24 contracts for UK-ETS are circa. £37/tn – UKAs remain at a significant discount to EUAs (see chart).

Our electricity generation mix is fairly neutral today with renewables contributing 32%, thermal at 22% (gas and coal) and low carbon at 27% (nuclear and imports).

Monthly Day-Ahead averages for April achieved £69/mwh (or 6.9p/kwh).