High wind outputs are limiting gas-for-power burn.

Norwegian scheduled maintenance is all but over for another year.

Following this summer’s stockpiling drive, European storage fullness is at 83% versus the 5-year average of 93% – just in time for the heating season!

Despite lingering conerns over weather forecasts and geopolitical banana skins, market participants are undoubtedly confident that we have enough in the tank to make it through the winter months.

We’ll also keep a close eye on Asian demand – though China’s spot purchases of LNG have fallen significantly Y-o-Y – inevitably freeing up more cargoes for Europe (and limiting associated price battles).

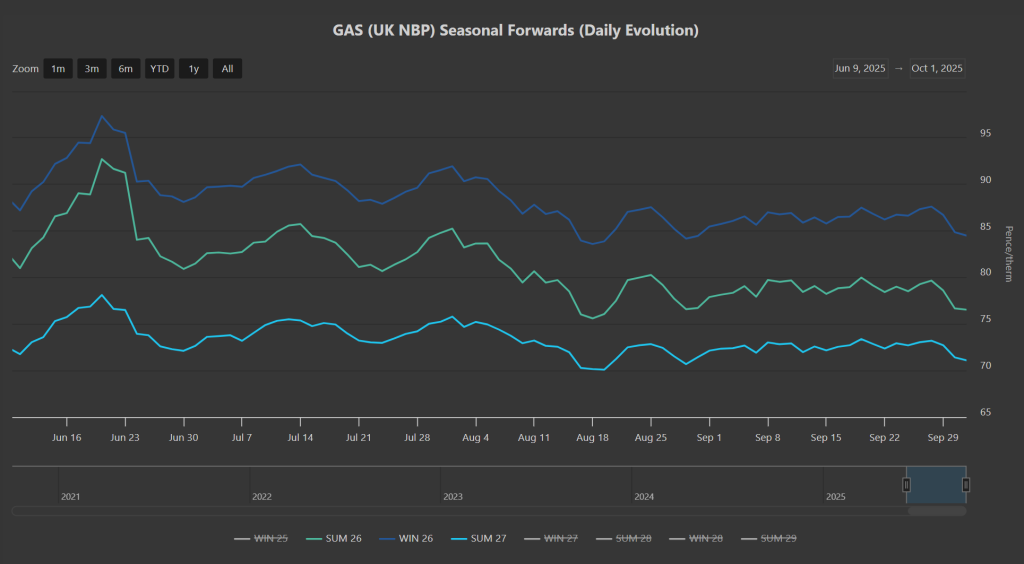

Monthly Day-Ahead averages for September came in at 79p/therm (or 2.7p/kwh exc. non-gas).

Monthly Day-Ahead averages for October so far are at 72p/therm (or 2.4p/kwh exc. non-gas).

In short, we’re enjoying a late summer lull off the back of benign fundamentals with the front 3-Seasons drifting lower (please see chart below).

ELECTRICITY & CARBON

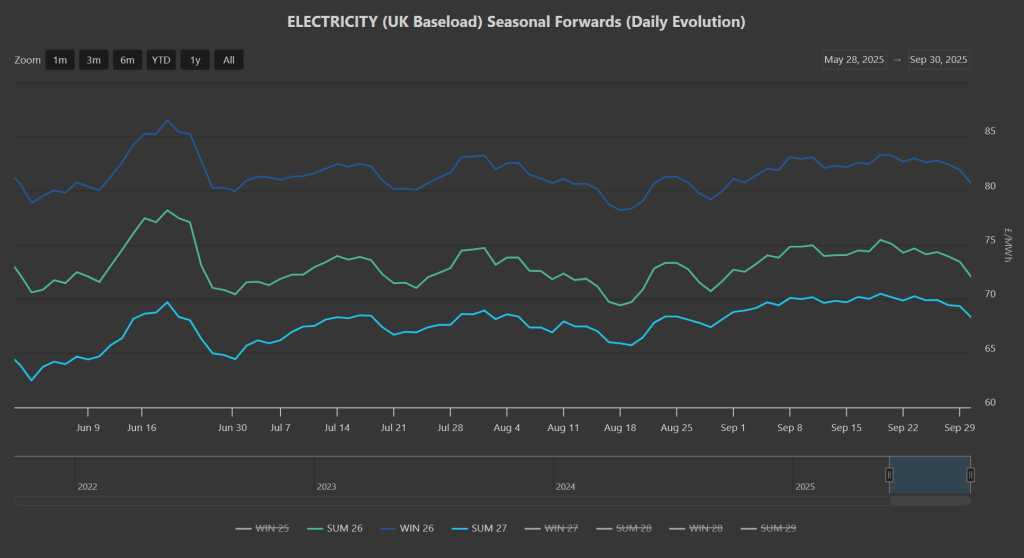

Electricity prices are seeing a more modest drop-off compared to gas – nonetheless, the front 3-Seasons are rolling over despite the prospect of winter supply tightness around the corner.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices remain at £57/tn.

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 56%, thermal at 17% (gas and coal) and low carbon at 16% (nuclear and imports).

Monthly Day-Ahead averages for September came in at £67/mwh (or 6.7p/kwh exc. non-energy).

Monthly Day-Ahead averages for October so far are at £52/mwh (or 5.2p/kwh exc. non-energy).