Prices remain balanced, with neither bulls nor bears having the upper hand.

Fundamentally, key drivers are overwhelmingly bearish – supply is strong; demand is above seasonal norms but falling; renewables outputs are strong and limiting gas-for-power burn.

On the bullish side, markets remain supported by an undercurrent of geopolitical risk and a forecasted heatwave at the back end of next week (which is likely to increase cooling demand across Europe).

In other news, the UK’s Easington gas terminal (handling up to one-third of our supply) came back online yesterday (following a period of unscheduled maintenance), easing supply tightness across the system.

As such, the UK system opened long today (supply outstripping demand forecast) amid great wind outputs.

Across Europe, we’re hearing very positive noises as to the likelihood that storage will be replenished in time for the next heating season (Winter-25), with European fullness now at 59% versus the 5-year average of 70%.

LNG vessels degasifying at European/UK ports are in good shape with 15 arrivals in the last week and 10 on the way – coupled with Norwegian pipeline flows holding steady above the 10-day moving average, we should be seeing falling prices.

The fact that overwhelmingly bearish drivers are failing to take the market lower should give buyers pause.

Have we reached a market bottom? Given underlying geopolitical risk, can the market go lower over the next couple of months (before the inevitable winter increases beginning Sep/Oct)?

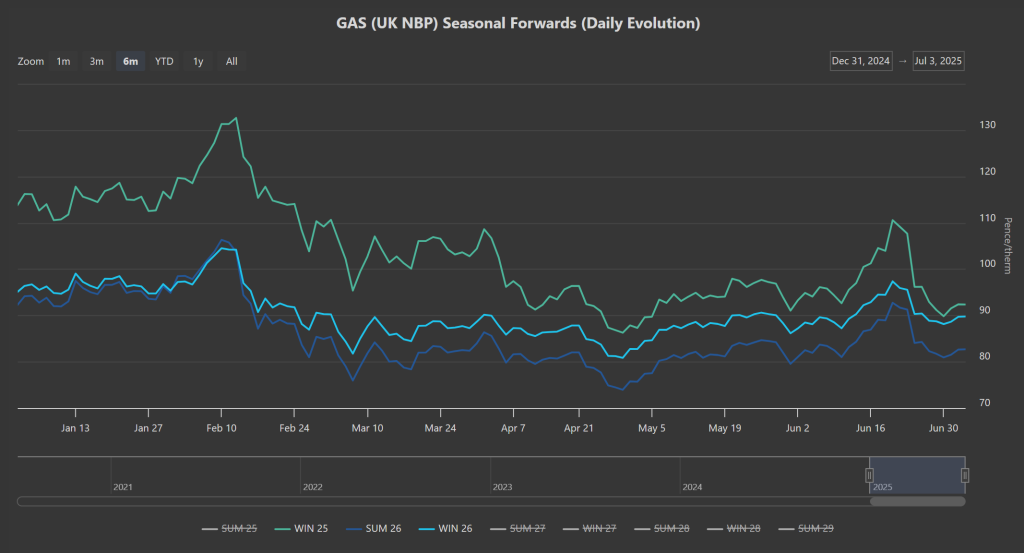

Well, focussing on the front 3 seasons for a second, the most recent market lows happened at the end of April BEFORE the US dropped bombs on Iran (please see chart below).

Surely, if benign conditions persist (and Asian demand remains subdued, and supply remains strong), then market participants will likely have another crack at breaking below April’s lows – if attempts to take the market lower fail, then buyers would be wise to consider closing out significant winter volumes (before the bulls take a hold of the market).

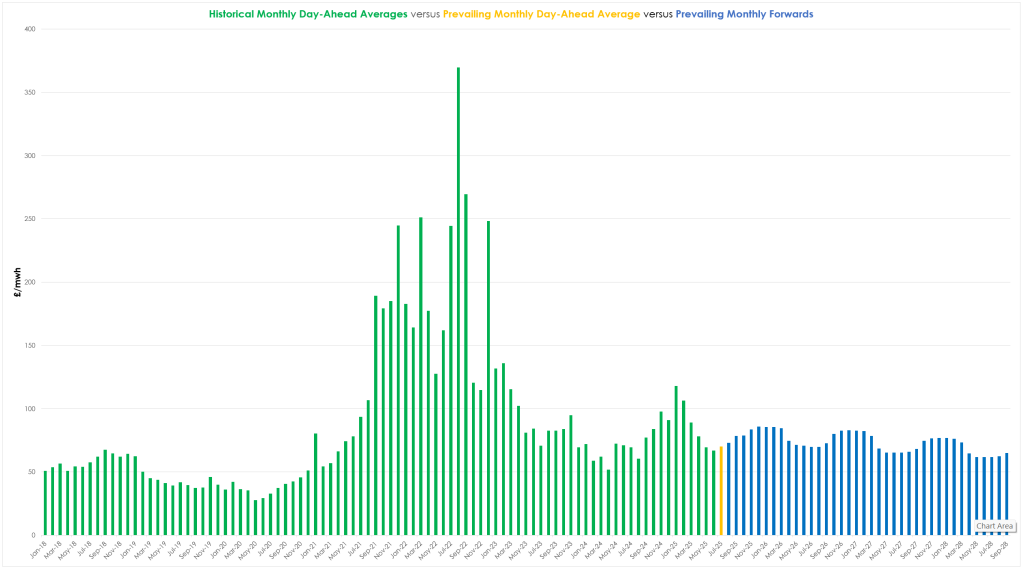

Monthly Day-Ahead averages for the month so far are holding very steady at 78p/therm (or approx 2.6p/kwh excluding non-gas).

ELECTRICITY & CARBON

Electricity prices are consolidating in a tight range.

Winter-25 is at £85/mwh (last printed 30th May) – so down 12% versus the highs of 19th Jun; and up 8% versus the lows of 29th Apr.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

As such, prices have dropped steeply in line with European/UK gas falls.

At the time of writing, Dec ’25 UKA benchmark prices are at £47.75/tn on the mid-price (a drop of 13% versus 13th Jun) – next meaningful area of support is £44/tn but rumour has it that significant BUY orders are building at £45/tn – so a prudent trade would be a BUY entry at £45.50/tn (so as to not miss the opportunity to get in).

Today’s UK electricity generation mix is bearish in nature reflecting benign ‘summery’ weather conditions, limiting gas-for-power burn – specifically, renewables are contributing 61%, thermal at 9% (gas and coal) and low carbon at 15% (nuclear and imports).

Monthly Day-Ahead averages for the month are falling day-by-day – currently at £70/mwh (or approx 7p/kwh excluding non-energy).