Gas prices across Europe/the UK continue to drift lower amid comfortable global supply dynamics, unseasonably mild weather (and forecasts of more to come), subdued demand, solid renewables outputs, plentiful US LNG arrivals degasifying at European/UK ports, and optimism amongst market participants that next year will bring more (not less) geopolitical stability.

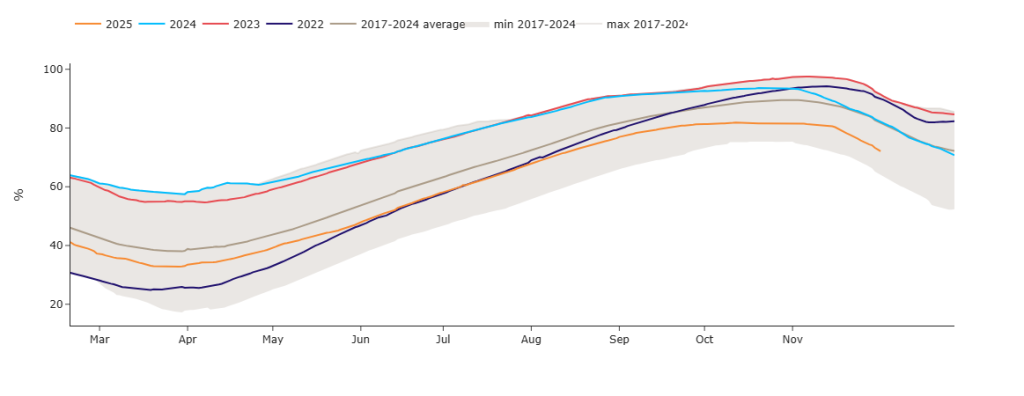

Net withdrawal has begun and so European storage levels have rolled over (please see chart below).

European storage levels are at 74% versus the 7-year average of 82% – further easing fears of any potential winter shortages.

Given the UK’s limited gas storage facilities, subdued demand has resulted in regular exports into Europe.

Asian demand for LNG also remains weak (particularly China), ensuring that more supply heads to Europe, alleviating competition for cargoes (and keeping a lid on values).

French nuclear availability is steady in the run up to the heating season, mitigating gas-for-power burn across the continent.

Traders continue to eye the bearish impact of the return of Russian gas flows if/when peace talks bring about an end to Russian sanctions.

All in all, the prevailing bearish tone of energy markets is being driven by healthy supply outstripping subdued demand.

Monthly Day-Ahead averages for December so far are at 71p/therm (or 2.4p/kwh exc. non-gas).

ELECTRICITY & CARBON

Electricity Seasonal Forwards are down versus 1/week/1-month/3-months/6-months ago.

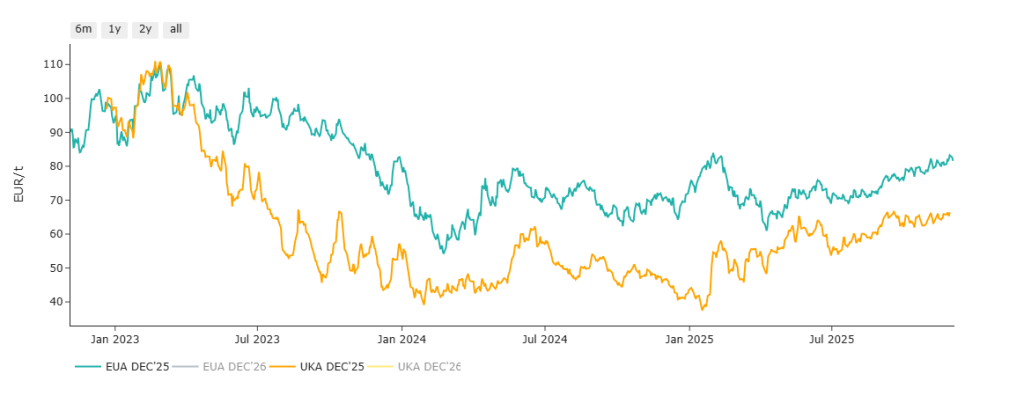

On the Carbon side of things, UKAs are trading below key resistance at £57/tn, and have carved out a falling trend channel with £55.50/tn still a viable target to the downside, thereafter £54/tn.

Please see below chart detailing the comparative discount of UKAs versus EUAs (with UKAs evidently less bullish this last week after speculators failed on six separate occasions since mid-Sep to break above the upper extremity of a long-term rising trend channel).

Today’s UK electricity generation mix is neutral in nature, neither bullish not bearish – specifically, renewables are contributing 47%, thermal at 30% (gas and coal) and low carbon at 15% (nuclear and imports).

Monthly Day-Ahead averages for December so far are at £77/mwh (or 7.7p/kwh exc. non-energy).