Markets found support yesterday driven by forecasts of colder, stiller weather conditions.

The gas system was short at open (demand outstripping supply).

Expect increased withdrawal from storage, as well as reduced exports via the Interconnector to the continent (to meet heating and gas-for-power generation demand).

Temperatures will drop to below seasonal norms into next week and stay that way until at least the third week of Jan ’24.

Markets are trading lower this morning, with still solid wind outputs keeping a lid on any upside moves.

Further out, bullish momentum persists with risk of colder weather across Europe and the UK, and of course, heightened tensions across the Middle East.

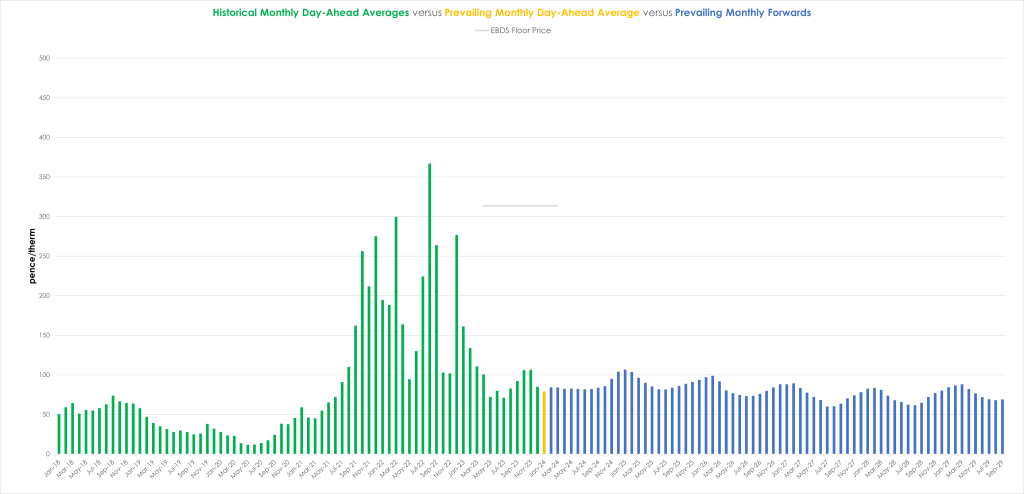

Monthly Day-Ahead averages are on target to achieve 79p/therm (or 2.7p/kwh).

ELECTRICITY

Looking to the continent, European short-term delivery prices went on a tempered bull-run yesterday, against a backdrop of falling temperatures and renewable outputs (while firmer fuels prices provided additional support to the market).

Expect more of the same next week, with colder/stiller conditions forecast (increasing reliance on storage withdrawal/gas-for-power-burn)- though solar production looks good, as does French nuclear availability – which should offset bullish momentum to a degree.

Following yesterday’s bullish rally, prices dropped off again in the afternoon mirroring gas and carbon markets as participants evidently regarded hydro and gas storage levels sufficient to endure next week’s cold spell without too much risk of shortage – plus six French nuclear reactors are now scheduled to come back online.

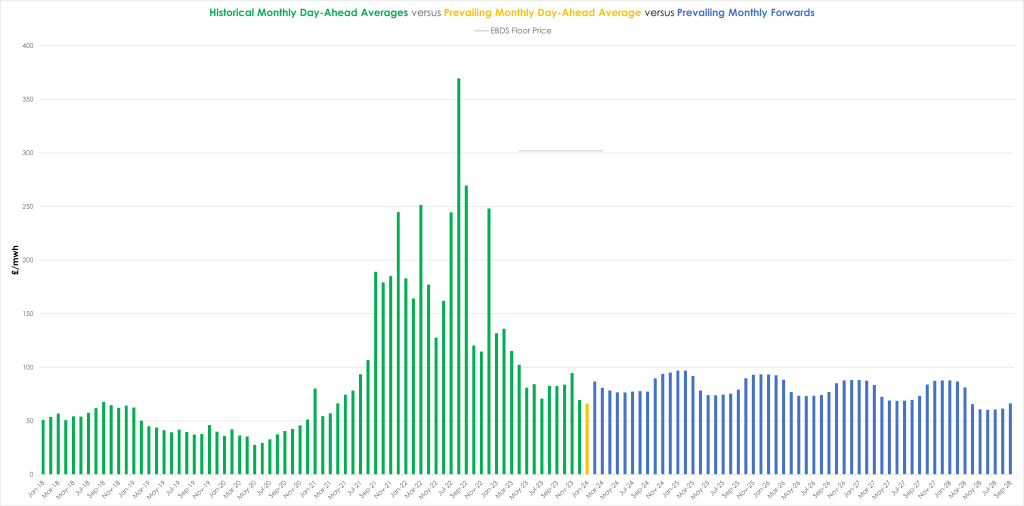

Back in the UK, monthly Day-Ahead averages are on target to achieve £69/mwh (or 6.9p/kwh).