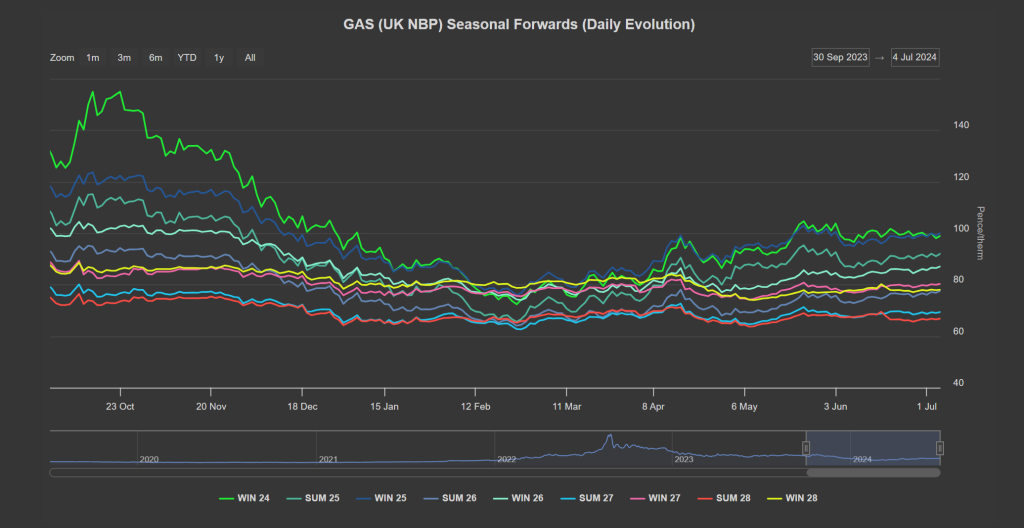

Whilst Winter-24 delivery has enjoyed the biggest relative decrease since Dec ’23 (compared to all other Seasonal Forwards), it continues to meander sideways at the psychological price level of circa. 100p/ therm (where it’s been trading since 21st May ’24) – see chart.

The UK system opened long this morning and comfortably supplied despite an unplanned outage at Oseberg (Norway) having removed 7.5mcm/day (and the outage at Visund field having been extended by a further week taking another 7.4mcm/day offline).

On the demand side, Total UK demand is up 7mcm off the back of slightly weakened wind outputs.

Despite threatening to warm up, temperatures are again below seasonal norms today – we’re told to expect more of the same next week (with a brief return to seasonal average on Wednesday before cooling into the weekend).

Nonetheless, prices are marginally down this morning pressured in the main by high European storage levels (78% versus the 5-year average of 64%).

The General Election results came as no surprise with Labour winning a landslide – markets had already priced in the result.

We’re 96 days into Summer-24 with the onset of Winter-24 now 88 days ahead.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24) – though LNG delivery remains tight against a backdrop of sustained high temperatures across Asia (and the associated cooling demand).

Monthly Day-Ahead averages so far this month are on target to achieve 78p/therm (or circa. 2.65p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices yesterday cleared much lower than over the past few weeks thanks to a wind event that is crossing NW Europe.

The combination of high wind and solar outputs are putting a lot of stress on the grid during the day increasing the phenomenon of oversupply and, of course, price dips as a result.

On the Carbon markets, prices inched up to close at €70.76/tonne having failed to break above resistance at €71.6/tonne during the session.

As such, logic dictates that a retest of underlying support at €70/tonne is on the cards (speculators hate equilibrium!)

The COT (Commitment of Traders Report) for the week ending 28th Jun ’24 was published yesterday.

It showed an increase in net-shorts positions from investment funds by 16.6% or (3 million tonnes) following the downward move from last week.

Back in the UK, UKAs (UK Carbon Allowances) followed our prediction that prices were due to fall (as indicated by RSI divergence) – now trading at circa. £46/tonne.

Prices are now in a confirmed ascending trend channel testing the mid-line – congestion is building at £40/tn as a strong area of support – so a retest of this level is likely if EUAs can pick up some bearish momentum.

Our electricity generation mix is bearish in nature today with renewables contributing 47%, thermal at 12% (gas and coal) and low carbon at 25% (nuclear and imports).

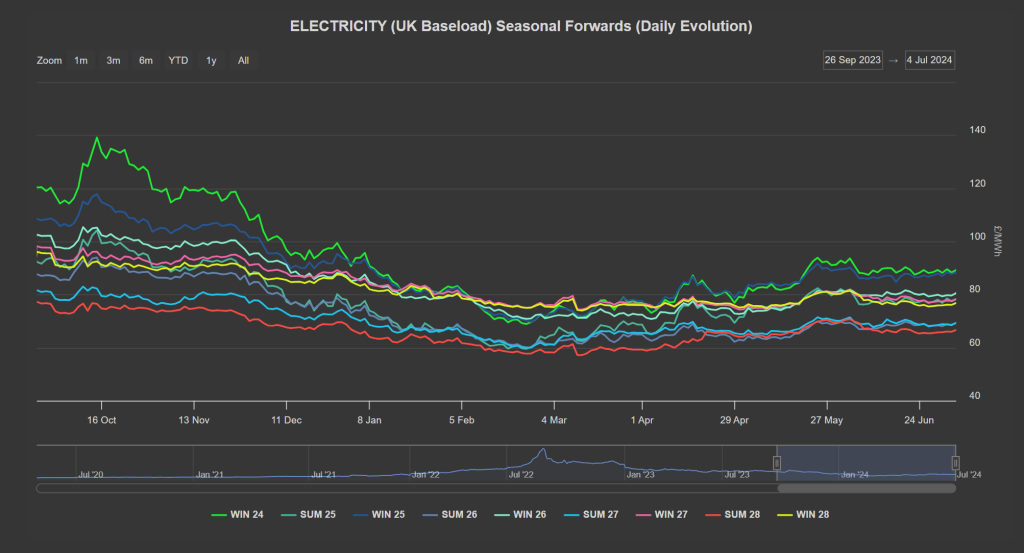

Monthly Day-Ahead averages so far this month are looking very summery, and are on target to achieve £56/mwh (or circa. 5.6p/kwh excluding non-energy).