Markets have drifted sideways today, and finished little changed on the week.

The last few days have seen multiple instances of Republicans joining with Democrats in the House of Representatives to vote against the policies of the Trump Administration.

Whilst only time will tell if their efforts to unpick Trump’s omnipotence will come to anything, it’s nonetheless significant that Republican support for the war in Iran is undeniably fading.

Lawmakers are pressing the Trump administration to justify ongoing secret diplomacy, challenging the official stance that the military conflict has been won/successfully concluded.

During congressional hearings, members of the House and Senate challenged Secretary of State Marco Rubio, asking why diplomacy is necessary if the war is allegedly “won”.

In a 215 to 208 vote to adopt the “war powers resolution”, the House passed a measure that seeks to halt the Administration from taking further military action – and so, Trump will need to withdraw US forces, or seek congressional approval to continue his increasingly vague operation in the Gulf.

Perhaps sensing that US support for Trump is wavering, the Iranian regime have today reaffirmed their support for Hezbollah and demanded that Israel withdraw from southern Lebanon, otherwise no deal with the US and the Strait remains closed!

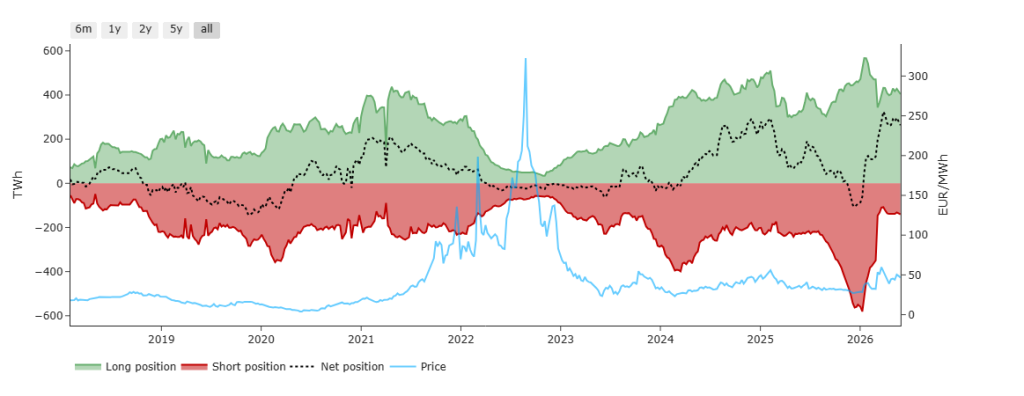

Not surprisingly then, as per the chart below, Investment Funds have further sold-off their long positions in TTF (the European gas benchmark) for the second week in a row.

On the supply side, European storage numbers are starting to show signs of strain – fullness is now at 41% versus the 5-year average of 63% (so worryingly off the pace).

On the FLEX side, as has been the case all summer, traders will be looking to trade the front-month and/or balance of Summer-26 prices in the dips as the month progresses – pending a final resolution to the crisis, after which prices will likely fall (steeply).

Monthly Day-Ahead Averages for May came in at 116.355 p/therm (or 3.97 p/kwh).

Monthly Day-Ahead Averages for June so far are at 118.967 p/therm (or 4.06 p/kwh exc. non-gas).

ELECTRICITY & CARBON

UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb – primarily due to summery conditions, solid renewables outputs (meaning lower gas-for-power generation).

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 48%, thermal at 10% (gas and coal) and low carbon at 21% (nuclear and imports).

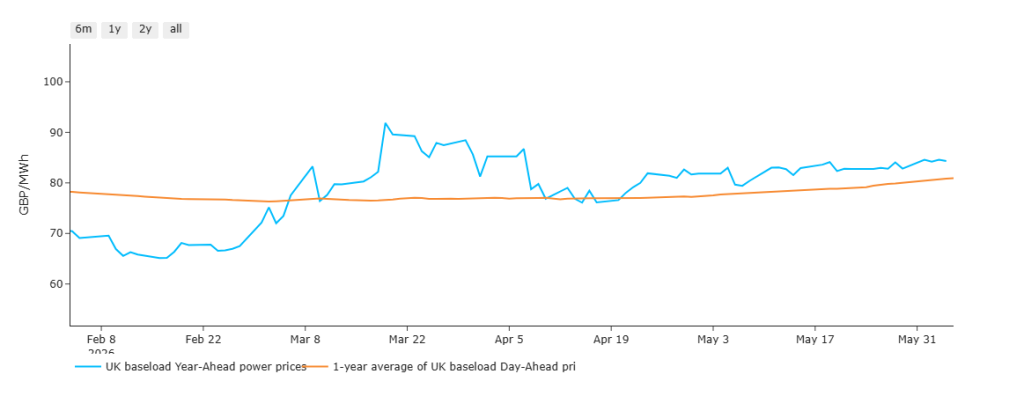

The chart below details UK electricity Year-Ahead prices versus the 1-Year Average of Day-Ahead prices since late-Feb.

By way of explantion, when the blue line is above the orange line, mid-term delivery prices are at a premium to an average of the last 12 months.

As you can see, prior to the onset of the US/Israeli offensive, prices were enjoying a soft-landing heading into Summer-26 – thereafter, Year-Ahead has remained consistently at a premium despite the otherwise ‘summery’ conditions.

Whilst the blue line remains above the orange line, it’s fair to conclude that prices are not as good as they should be (were it not for bullish geopolitical drivers).

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets.

However, correlation shifted to equities throughout March (which continue to enjoy a strong, tech-led upwards momentum).

At the time of writing, UKA mid-price Dec ’26 delivery is at £55.53/tn (and the spot is at mid 54s) amid rumours that the EUETS/UKETS linkage looks increasingly likely (meaning UKETS will need to rise to parity).

On the FLEX side, as has been the case all summer, traders will be looking to trade the front-month and/or balance of Summer-26 prices in the dips as the month progresses – pending a final resolution to the crisis, after which prices will likely fall (steeply).

Monthly Day-Ahead Averages for May came in at £103.069/mwh (or 10.307 p/kwh exc. non-energy).

Monthly Day-Ahead Averages for June so far are at £92/mwh (or 9.2 p/kwh exc. non-energy).