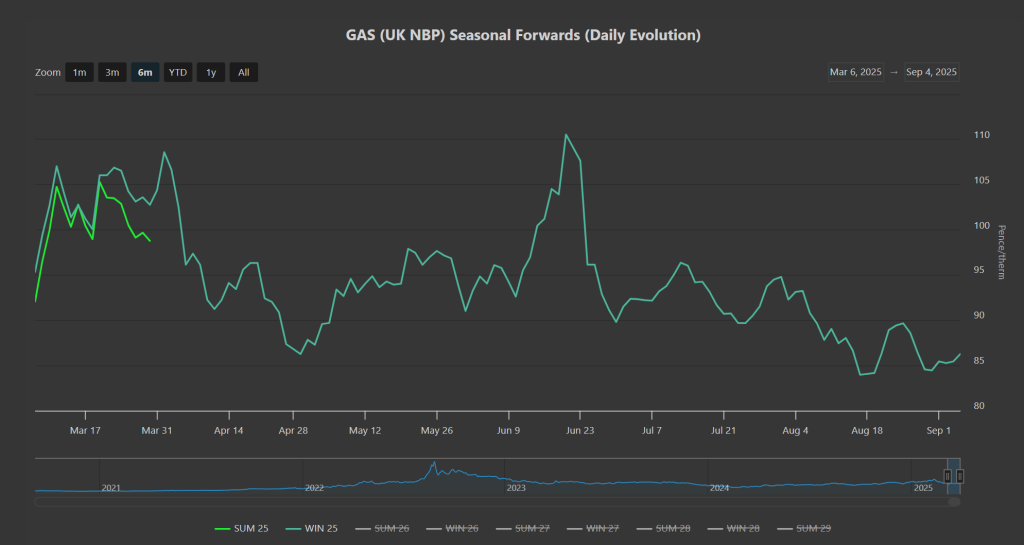

Notably, and by way of illustrating how volatility has decreased further over the summer period, prices now for Winter-25 delivery are at a 12.5% discount versus the offers we saw for Summer-25 delivery back at the end of Mar ’25 (please see chart below).

Markets are marginally up today off the back of poor wind outputs, and cooler temperatures forecast for the weekend.

The main talking point amongst market participants is the impact of Russia into China gas transit – both pipeline (beefing up the existing ‘Power of Siberia’ pipeline) and LNG (the second ever delivery of LNG from the US sanctioned Arctic LNG 2 export terminal in Russia is expected to degasify in the coming days at Beihai import terminal in China).

On the face of it, more gas flowing into the global system should be a bearish driver regardless of where it’s coming from, or where it’s going – so all eyes are on Trump’s reaction to China shrugging off US sanctions and instead deepening trade relations with Putin.

Certainly, China’s recent show of force at a parade with Xi Jinping, Putin and Kim Jong-Un front and centre, makes clear that China believes it can weather Trump’s tariffs – so it would seem likely that Russia will continue to deliver more and more gas into China.

Escalations by Ukraine forces have seen missiles launched at key Russian infrastructure – an oil refinery in Ryazan and an oil depot in Luhansk.

As such, fears of the extent of Russia’s reprisals are stoking some bullish momentum on near-term delivery – hence today’s supportive tone.

European storage fullness is now at 79% versus the 5-year average of 89% – with injections slowing (in the main) due to the climax of the Norwegian pipeline maintenance season.

Any late buyers of Winter-25 delivery are strongly encouraged to get in soon before winter conditions kick-in (and storage injections flatten come October).

Monthly Day-Ahead averages so far have been at 79p/therm (or 2.7p/kwh exc. non-gas) since the start of the month – so, very low volatility persists.

ELECTRICITY & CARBON

Prices have firmed a little today in line with firmer gas Forwards.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices have broken to the topside off the back of the impending close to the summer season – prices having broken above further resistance levels and are at £56.16/tn on the mid-price.

As per the chart below, prices are now observing an upwards trend channel, with the next meaningful resistance level at £57/tn.

Despite poor wind outputs across Europe, today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 42%, thermal at 17% (gas and coal) and low carbon at 22% (nuclear and imports).

Any late buyers of Winter-25 delivery are strongly encouraged to get in soon before winter conditions kick-in (and gas storage injections flatten come October).

Monthly Day-Ahead averages for the month so far are at £72/mwh (or 7.2p/kwh exc. non-energy) – which happens to be the Monthly Day-Ahead average for the whole summer to date (reflecting very low volatility this season).