Despite the last few days’ hysteria over storage injection fears for next summer, prices are closing down on the week, up on the month.

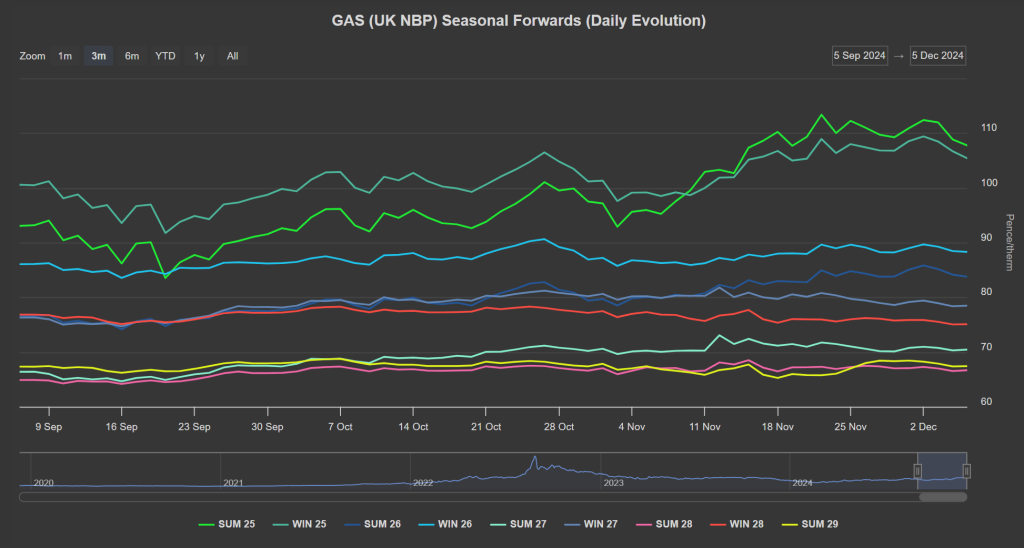

Summer-25 remains at a marginal premium to Winter-25, but it’s small potatoes, and there’s plenty of Winter-24 ahead of us for the tangled order of Forward prices to unravel themselves (see chart below).

Prices opened lower today, continuing yesterday’s direction of travel, amid weaker demand, milder weather forecasts and an increasingly encouraging LNG arrivals schedule (12 before month end).

This morning’s decline can also be attributed to reports that, despite US sanctions, Russia has amended gas payment policies, enabling international purchasers to pay for supply via a third party.

This (very convenient) workaround has inevitably put pressure on prices by taking the heat out of bullish fervour (and easing worries over supply tightness once the Ukraine/Russia transit deal comes to an end this month).

Serbia gets more than 60% of its gas from Russia, however it’s come to light that Serbia is looking for a comparable deal from Azerbaijan, establishing a new route to an LNG terminal in Greece – another example of Europe diversifying away from reliance on Russian export.

European storage is sitting at 84% (versus the 5-year average of 87%) – so not too far off the pace but a 3.3% decrease from the previous week due to withdrawals.

Back in the UK, Storm Darragh is bringing strong winds and rain this evening, potentially making it tricky for LNG arrivals to our shores to degasify (temporarily tightening supply).

So far this month, Monthly Day-Ahead averages are on target to achieve 117.02p/therm (or approx. 3.992p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent for price direction, mild conditions are forecast in the coming days, to be followed by a colder north-easterly flow across CWE (Central Western Europe) early next week.

Windy conditions are forecast until mid-next week across the UK and CWE – limiting gas-for-power burn.

Limited solar generation is forecast in the coming days, especially Monday given the remnants of the low-pressure system.

The run-of-river production will likely increase due to expectations of heavy rain – though the impacts could be delayed due to the risk of low altitude snowfalls.

A 24-hour strike by French energy workers only marginally affected nuclear, hydro and gas-fired generation, with little impact on prices (amid healthy supply and solid nuclear availability).

On the Carbon markets, EUAs (European Allowances) continued their slide yesterday, tracking TTF (European gas benchmark) prices amid still and mild weather conditions (limiting heating demand).

The Dec ’24 benchmark EUA contract reached a high of €68.69/tn early in the morning but then retraced its gains before noon.

The auction settled at €67.6/tn and the main (secondary) contract continued its downtrend in the afternoon, reaching a low of €66.91/tn, before closing the day at €67.34/tn (-0.77%).

Back in the UK, UKAs (UK Allowances) are back on the slide on low volumes (see chart below).

At the time of writing, UKAs are at £35.17 having broken below the most recent lows of 27th Nov – so more comparative value back on the table for Compliance buyers.

The UK’s electricity generation mix is bullish in nature today with renewables contributing 25%, thermal at 38% (gas and coal) and low carbon at 18% (nuclear and imports).

Monthly Day-Ahead averages for the month so far are on target to achieve £94.909/mwh (or 9.49p/kwh excluding non-energy).