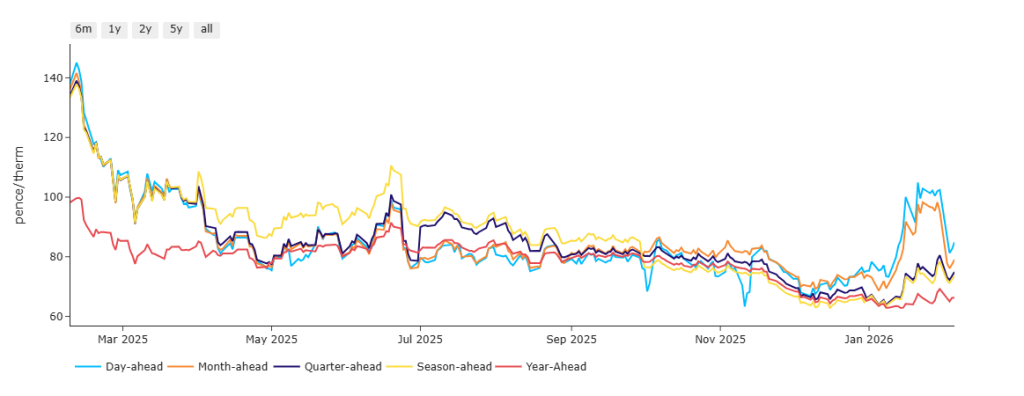

During periods of high wintry volatility, price-action charts (such as the one below) can often tell us more than the ‘noise’ (such as flip-flopping weather forecasts/unsubstantiated rumours/geopolitical incidents/fundamental drivers).

As per the chart below, near and mid-term delivery has fallen back in the last week – and last winter’s highs were posted 11th Feb ’25, so might we have already seen the highs of this winter already?

Well, it’s fair to say that prices are at a junction right now, with the benchmark TTF European Month-Ahead gas market sitting at its 1-year moving average, and European/UK price direction undecided between the bearish impact of above seasonal norm temperatures (across swathes of Europe) and the bullish impact of unnervingly low European gas storage fullness (now at 38% versus the 5-year average of 65%).

The UK system opened short this morning (demand forecast outstripping supply).

Consensus persists that chilly weather will likely sweep over northwest Europe in mid-Feb, putting pressure on storage levels with a couple of months of the heating season still remaining.

In other industry news, UK gas demand is expected to fall marginally this year, driven by a 6% drop in gas-for-power burn amid only modest increases in domestic and industrial consumption.

US and Iran held talks in Oman today – this following the US having advised US citizens to leave Iran this week.

The negotiations ostensibly centre around Iran’s nuclear intentions/capabilities – with Trump no doubt reserving the right the resort to military methods should it look like the regime is ready to topple.

On the strategy side, FLEX clients are still taking small positions further down the curve where there’s great value to be picked up.

Monthly Day-Ahead averages for the month are holding steady at 88p/therm (or 3p/kwh) following a week of auctions well below 100p/therm.

ELECTRICITY & CARBON

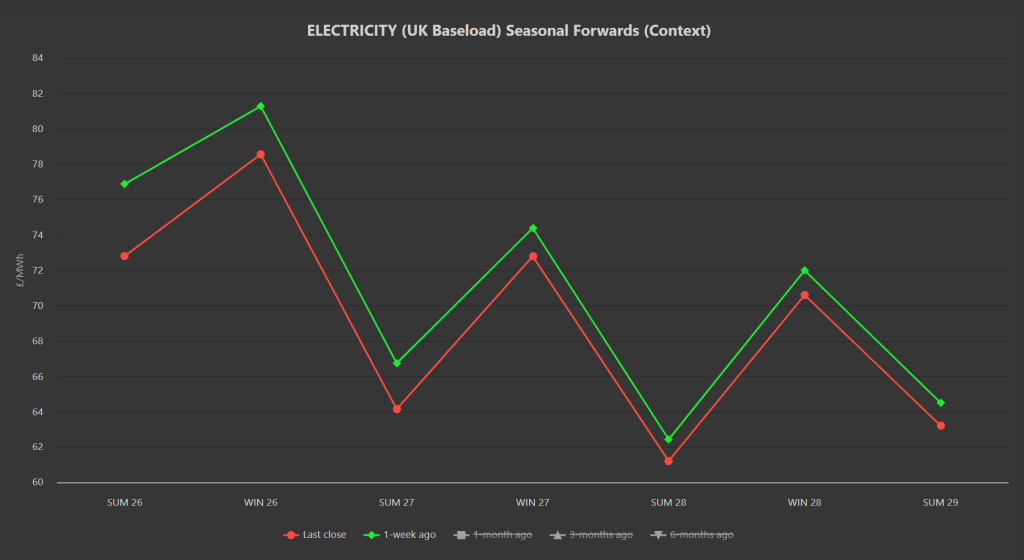

Seasonal Forwards all the way down the curve are lower on the week (see chart below).

On the Carbon side of things, both EUAs and UKAs have been in free fall this last couple of days – such is the unpredictability of emissions value given how quickly funds are piling in, then piling out.

Following last week’s dip, EUAs retested the level of resistance that had just been broken to the downside – price-action then bounced southwards reflecting a very technical sell-off .

Yesterday printed the biggest daily fall in EUAs for nearly 2 years – bearish drivers included rumours coming out of Europe that reduction targets are to be softened to protect Europe’s global competitiveness (so it would seem that the sheer volume of complaints from EU/UK emitters as to the runaway speculative nature of Carbon markets may just be finding their target).

UKAs have exceeded EUAs’ precipitous fall (given UKAs’ comparatively thin trading volumes) – at the time of writing, UKAs Dec-26 delivery are at £56.13/tn (and spot is approx. at a £2/tn discount).

Compliance buyers (whose activity in the market is eclipsed by the investment funds) can only ride the waves and are being advised to set downside targets then buy on the dips – so timing is everything.

Today’s UK electricity generation mix is neutral in nature , neither bullish nor bearish – specifically, renewables are contributing 39%, thermal at 37% (gas and coal) and low carbon at 16% (nuclear and imports).

Monthly Day-Ahead averages for the month so far remain wintry at £97/mwh (or 9.7p/kwh exc. non-energy).