Trump’s war on Iran is pushing economies across the globe into crisis.

Whilst the US/Israel air bombardment on Iranian targets has brought about the closure of the Strait of Hormuz (and all but halted the transit of 20% of the world’s oil and gas trade), Iran’s retaliatory strikes on targets across the Arab states of the Persian Gulf are further worsening the wider impacts of the crisis.

With Qatari LNG production incapacitated by the Iranian drone strikes earlier this week, coupled with several other major producers also shutting down production along the Gulf coast, LNG volumes to the Gulf’s biggest customers in Asia have all but stopped.

As such, Asia is outbidding Europe/the UK for vessels already at sea (regardless of where they’re coming from), and these cargoes are re-routing to Northern/Eastern hemispheres where bigger profits await.

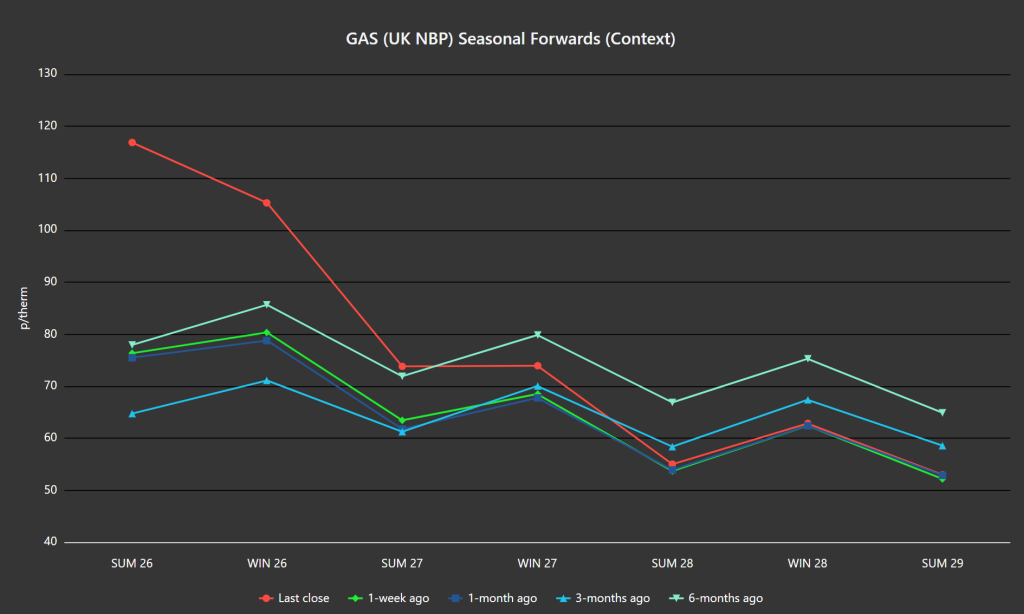

The chart below illustrates just how acutely the front 2-Seasons have spiked (Season-3 onward, prices are little changed – so, up to now, market participants are not pricing-in a long-term impact).

Notably, however, Summer-26 is at a premium to Winter-26 – of course, Europe is emerging from Winter-25 with historically depleted storage levels needing to secure significantly more seaborne cargoes over the summer than might usually be the case (inventories are now at 30% versus the 5-year avergae of 54%).

So, market mechanisms have established high prices ASAP to attract cargoes to our shores, otherwise storage replenishment over the summer will fall short, and then another crisis could develop if Winter-26 is a cold one.

Trump’s timing couldn’t have been worse for energy buyers – until last weekend, prices were on a downward trajectory with summer conditioning on the horizon.

This morning, Saad Al-Kaabi (Qatar’s Energy Minister) stated, ” If this war continues for a few weeks, GDP growth around the world will be impacted. Everybody’s energy price is going to go higher. There will be shortages of some products and there will be a chain reaction of factories that can’t supply.”

QatarEnergy has now declared ‘force majeure’ – a clause freeing it from liability for failure to supply due to events outside its control (and Kaabi believes that all other energy exporters would have to follow suit in the next few days should the war persist).

And so, Industrials across the globe that had been looking forward to a soft landing this summer, are being forced to re-assess budget forecasts in the event that the conflict grinds on.

In the main, buyers are adopting a wait-and-see approach given that Trump is prone to abrupt climb downs – though analysts fear he’s too committed at this stage to pull-back.

Prices are on track for their biggest weekly increase since the dark days of Putin’s invasion of Ukraine (and the subsequent sabotage of Nordstream).

Implied volatility in Europe’s benchmark gas futures have more than quadrupled since the start of 2026 – around the globe, questions will increasingly be levelled at the US as to where this is all headed.

Seasonal Forwards remain steeply backwardated with some great offers remaining further down the curve (Summer-29 is at a 56% discount versus Summer-26).

As such, on the strategy side, FLEX clients are being encouraged to build modest positions further down the curve where steady prices persist.

Monthly Day-Ahead averages for the month so far are rising day-on-day – currently at 116p/therm (or 4p/kwh).

ELECTRICITY & CARBON

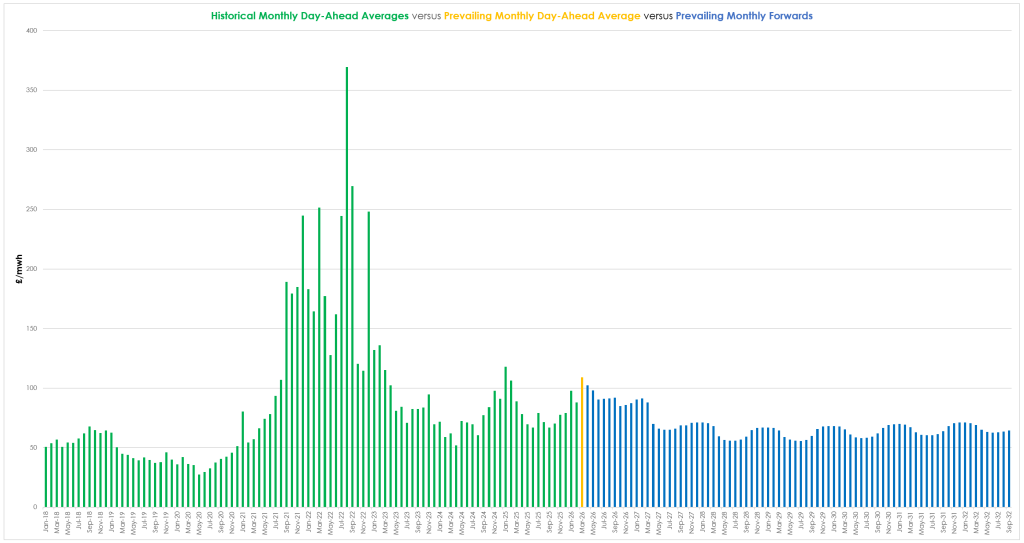

The chart below shows historical/achieved Monthly Day-Ahead averages (green); prevailing Day-Ahead average for the current month (orange); and prevailing Monthly Forwards (blue).

It’s always worth a glance as it shows clearly where we’ve been versus where we are versus where we’re going.

As you can see, whilst the current crisis is unwelcome and a significant knock to summer budgets (if the conflict persists), prices are still a long way below the severity of the crisis caused by the invasion of Ukraine etc.

At the time of writing, Dec-26 UKA delivery has fallen to low-£40s/tn (down 44% versus mid-January) – another budgeting headache for heavy emitters!

Today’s UK electricity generation mix is bullish in nature – specifically, renewables are contributing 16%, thermal at 50% (gas and coal) and low carbon at 21% (nuclear and imports).

As with gas Forwards, on the strategy side, electricity FLEX clients are being encouraged to build modest positions further down the curve where steady prices persist (given that far term delivery prices are as much as 30% below those of near-term delivery).

Monthly Day-Ahead averages for the month so far are mirroring near-term gas prices – currently at £109/mwh (or 10.9 p/kwh).