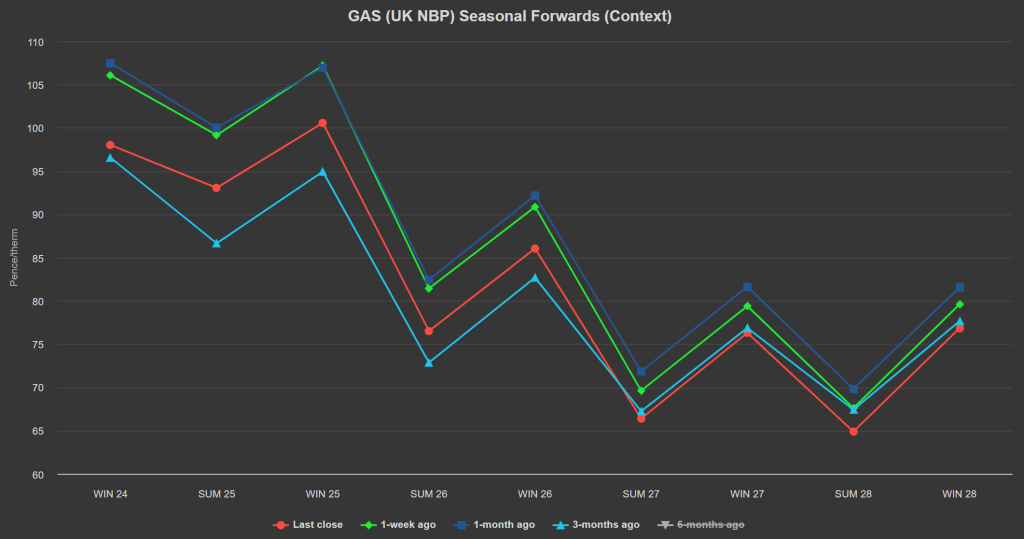

It’s been sideways price action to end the week – with Seasonal Forwards now down on the week, down on the month, but up versus 3-months ago (see chart below).

Heavy Norwegian maintenance continues to restrict supplies coming into the UK.

LDZ (heating demand) dropped off today with temperatures reaching 26°C in some parts of the UK – 5°C above seasonal norms.

Global competition for LNG has picked up again with Egypt looking to buy 20 cargos for delivery next month.

Lest we forget, Europe and the UK have come to rely increasingly on continuous global gas flows since Russia turned off the taps back in ’22.

However, strong EU storage (93% versus the 5-year average of 82%) continues to offset fears of impending supply tightness.

Industrial and domestic demand across Europe is around 20% below average levels for the 2017 to 2021 period.

We’re expecting two more LNG arrivals to degasify at British terminals before 11th September which should provide a boost to supply (amid current supply constraints caused by Norway’s flows being offline).

European LNG send-outs are forecast to be more than 20% higher in September compared to August – further evidence of a drop in cooling demand throughout Asia.

Elsewhere it appears geopolitical risk premiums are easing with tensions in the Middle East and on the Ukraine-Russia border stabilising (for now).

Clients with significantly open volumes for Winter-24 are in the minority – with most having opted to heavily hedge Positions with winter conditions now on the horizon.

Monthly Day-Ahead averages so far this month are on target to achieve 89p/therm (or approx. 3p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices are trading a in a tight range.

The weather outlook has revised colder for next week, with temperatures dropping 4°C below seasonal norms – increasing heating demand.

As further evidence of directionless trading, carbon and gas moved in opposite directions yesterday.

On the carbon markets, the benchmark Dec ’24 EUA contract has continued its slide to a six-week low – closing at €66.2/t after losing 1.1% on the day.

UKAs have idled today at around £42/tonne.

Our electricity generation mix has been neutral in nature today with renewables contributing 26%, thermal at 31% (gas and coal) and low carbon at 27% (nuclear and imports).

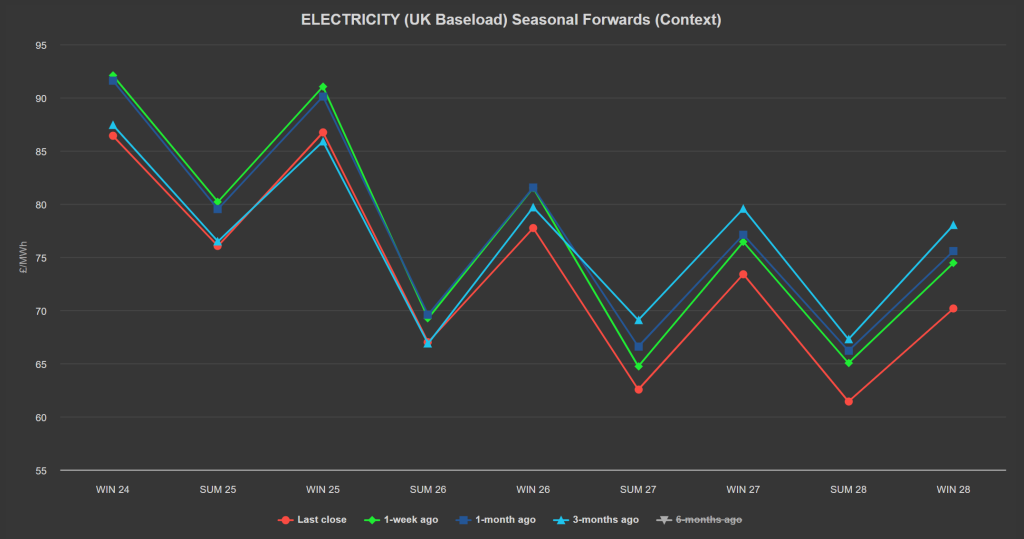

Monthly Day-Ahead averages so far this month are on target to achieve £82/mwh (or approx. 8.2p/kwh excluding non-energy).