As per our bulletin earlier this week, numerous elements remain supportive and are in danger of ruining the bearish summer party that looked on the cards following the significant falls in price we experienced between Dec ’23 to Feb ’24.

On the bullish side, risk persists that the long-term contract between OMV/Gazprom could be rescinded and subsequently impact other European companies (SPP in Slovakia/MVM in Hungary).

Flows via Ukraine account for circa. 50% of the total remaining Russian pipeline imports into Western Europe – payments to Gazprom are expected to be made on 20th of each month – so tensions will build as we approach the date…

Above average hurricane activity is being touted across the Atlantic Basin (between 1st Jun to 30th Nov), posing a risk to LNG facilities and associated cargoes headed to degasify across Europe/UK.

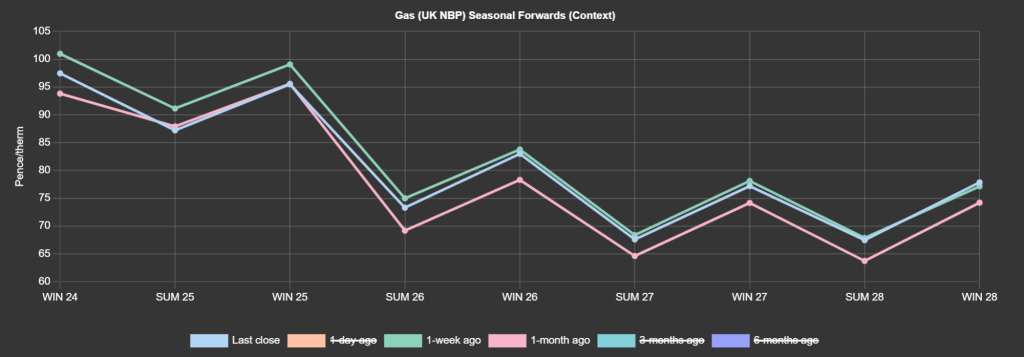

As of this morning however, Seasonal Forwards are down on the week (see chart) – due mainly to Norwegian flows being expected to rebound strongly today with nominations above the level reached before the Nyhamna outage causedby the cracked pipeline.

Repairs to the damaged pipeline are seemingly completed now.

UK demand is down today (116mcm from 128mcm) – this has ensured our system holds length (supply outstripping forecasted demand).

UK temperatures are expected to stay below seasonal norms for the next week or so, with low pressures now being forecast.

Thankfully, wind outputs are expected to hold above seasonal norms over this cold spell which should offset any extra demand from the LDZ (heating demand).

The consensus amongst Industrials continues to be one of scaling-in whilst adopting a wait-and-see approach to any remaining open volumes for Winter-24/winter-25.

116 days of Summer-24 remain (with 68 days now used up) – so we’ve got the best part of two thirds of Summer-24 still to come.

Whilst it’s conceivable we’ve already seen the bottom of summer pricing, it’s not panic stations just yet.

The consensus approach amongst clients is increasingly one of scaling-in the front Seasons (Winter-24/Summer-25/Winter-25) , so as to mitigate loss of summer value.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24).

Monthly Day-Ahead averages are on target this month to achieve 82p/therm (or circa. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

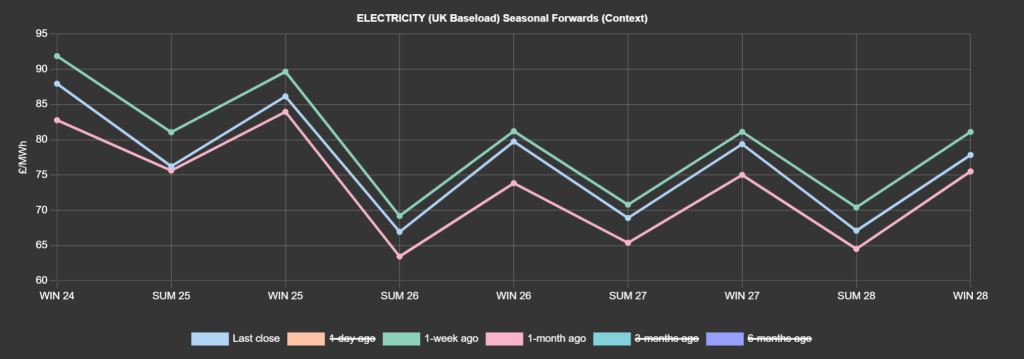

UK Seasonal Forwards are down on the week, but still up on the month (see chart).

Looking to the continent, European near-term delivery prices traded sideways yesterday.

On the Carbon markets, it was also a quiet day.

Participants are likely waiting on the June options expiry, as well as keeping an eye on the long-awaited EU elections which began yesterday.

At the time of writing, Carbon is softening – no doubt weighed by fading gas prices given the close correlation between the fossil fuel and it’s punitive cousin.

Back in the UK, UKAs (UK Allowances) continue to drop off a little – now trading at circa. £47/tn (Dec-24 benchmark) – having broken above the highs printed on 25th Mar ’24.

Our electricity generation mix is bearish in nature today with renewables contributing 53%, thermal at 5% (gas and coal) and low carbon at 27% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £71/mwh (or 7.1p/kwh excluding non-energy).