As the dust settles following the news of Trump’s return, market participants are absorbing the anticipated impacts of the new adminstrations’ policy shifts (beginning Jan-25).

Will gas prices fall in response to higher US production?

Well, LNG firms across the US are now expecting the green light on export permits off the back of Trump’s promises to limit red tape.

Also, cracks are appearing in the German coalition government, raising doubts that the levy (on German gas flowing out of, or through Germany ) will in fact be abolished before 2025 after all – at least, if an election is to take place, it seems unlikely that the levy will be removed as quickly as had been forecasted (meaning higher transit costs for Germany’s neighbours).

The supply-demand dynamic is taking on a wintry tone, with the heating season nearly upon us, front month/quarter/season delivery is looking increasingly supported.

Several European countries are experiencing their first meaningful withdrawals of Winter-24 amid predictions of lower temperatures and still conditions.

European storage fullness has dropped to 94% (versus a 5-year average of 92%) reflecting a gradual rise in heating demand and gas-for-power generation (in the absence of solid renewables outputs).

The UK’s gas will likely remain at a premium versus Europe’s as the winter progresses – otherwise, we’ll not attract the cargos.

This premium is exacerbated by structural problems in the UK’s gas system resulting in high transmission costs and, of course, a lack of storage compared to Europe – meaning the UK needs to offer a much higher price to secure supply.

As a rule of thumb, UK gas prices ordinarily trade at a discount to European prices during the summer, but remain at a premium in winter when the infrastructure creaks.

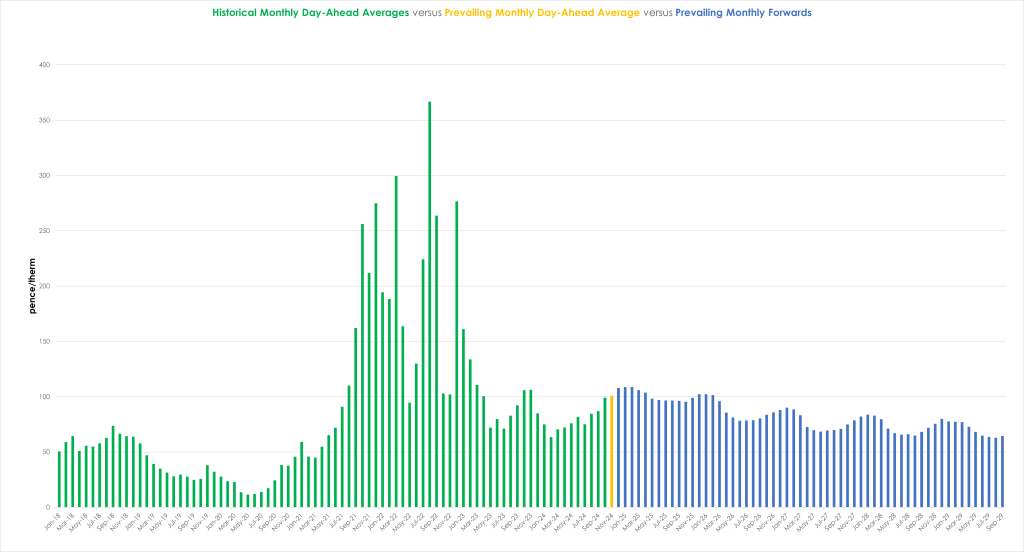

Monthly Day-Ahead averages so far this month are on target to achieve 101.067p/therm (or approx. 3.449p/kwh excluding non-gas).

ELECTRICITY & CARBON

On the continent, EUAs remain a little bullish mirroring gas prices amid lower temperatures forecast, as well as low wind and hydro power generation.

The Dec ’24 delivery benchmark opened slightly higher at €63.78/tn and has risen to €67.75/tn at the time of writing.

Following Wednesday’s auction, the market dipped off the back of an average cover ratio of 1.68 (the cover ratio being defined as the number of allowances bid for, divided by the number of allowances auctioned).

Back in the UK, UKAs have yet to retest the lows of 8th Oct – currently sitting at £38.40 on the mid-price.

Our electricity generation mix is bullish in nature today with renewables contributing 14%, thermal at 55% (gas and coal) and low carbon at 20% (nuclear and imports).

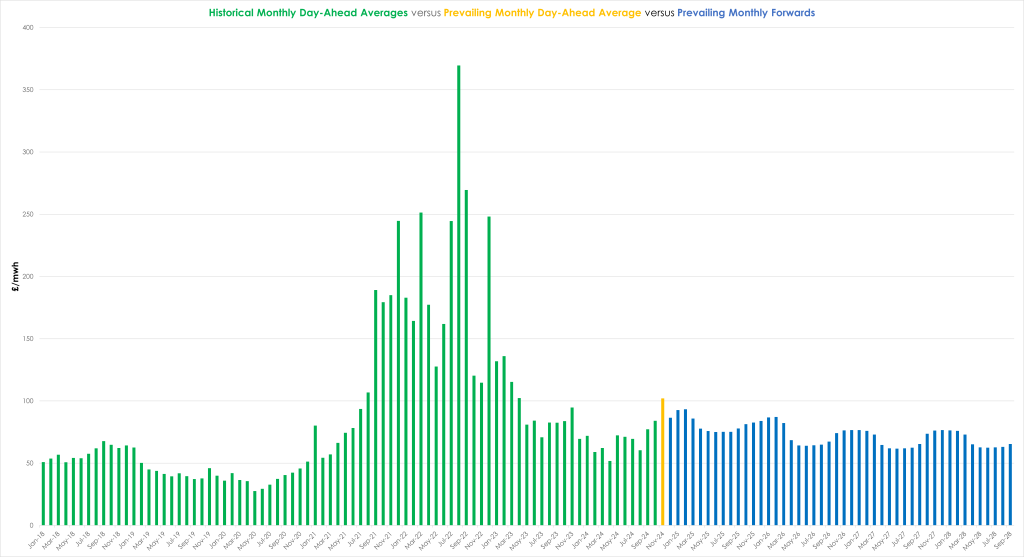

Monthly Day-Ahead averages so far this month are on target to achieve £102.117/mwh (or 10.21p/kwh excluding non-energy)