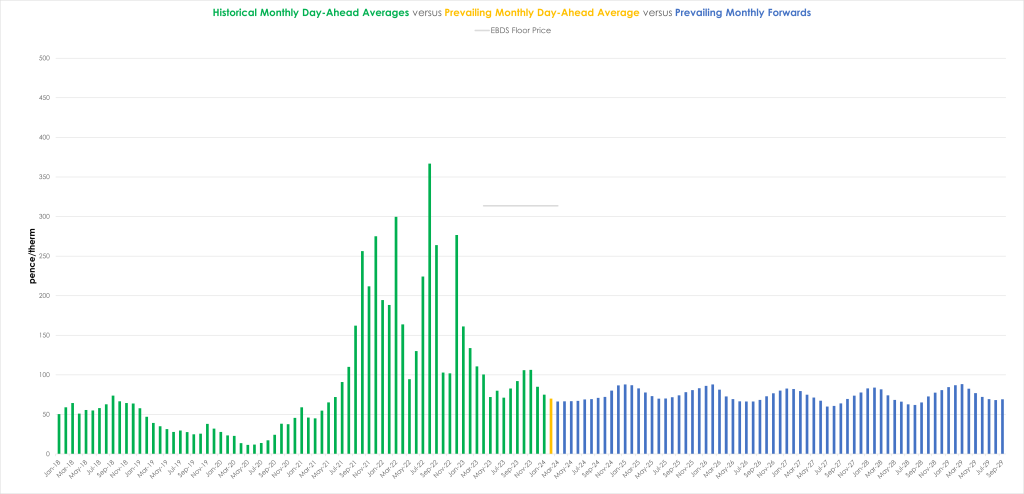

Near-term monthly delivery prices are now at levels commensurate with monthly Day-Ahead averages printed Summer-2018 (see chart).

At the time of writing, prices all the way down the curve are lower versus yesterday’s close off the back of wet and windy weather conditions.

For the first time this week, the UK system was long at open (supply outstripping demand).

Flip-flopping forecasts persist – we’re now told (by some) to expect temperatures to remain mild next week but there’s no meaningful consensus amongst forecasters.

However, all seem to agree that today will by circa 5°C higher than yesterday.

In short, today’s bearish bias is due to temperatures being above seasonal norms, solid wind outputs, high gas storage, Norwegian outages having ended (and flows being way above the 5-day average), UKCS flows having increased to their highest level for the week.

Rumours are now circulating that the long touted February cold spell might not materialise!

Whilst geopolitical risk is stopping the markets from falling off a cliff as summer approaches, the impact of Ukraine and the Red Sea problems on the supply/demand dynamic seem to be limited.

Monthly Day-Ahead averages are on target this month (so far) to achieve 70p/therm (or circa. 2.4p/kwh).

ELECTRICITY & CARBON ALLOWANCES

Near-term monthly delivery prices are now at levels commensurate with monthly Day-Ahead averages printed Summer-2018 (see chart).

Looking to the continent, European near-term delivery prices have faded (as expected) for the last working day of the week – pressured in the main by prospects of rebounding wind generation and lower demand.

Next week, prices may find some support from weaker wind outputs and French nuclear availability – although a noticeable increase of solar generation should offset any meaningul bullish momentum.

Forward markets remain heavily influenced by weather with successive warmer revisions to mid-February temperature forecasts exerting downward pressure on prices yesterday and continuing to do so this morning.

Fundamental drivers remain very comfortable and a significant rebound/upside testing seems unlikely at this time.

Carbon prices remain in near oversold territory across the technical momentum indicators (RSI/MACD/Stochastics).

Speculators have stopped adding to their short positions since mid-January, suggesting bearish trend exhaustion and imminent profit taking.

Nonetheless, carbon remains within the coal to gas switching range, suggesting that as long as gas prices continue to fall, emissions prices could very easily follow.

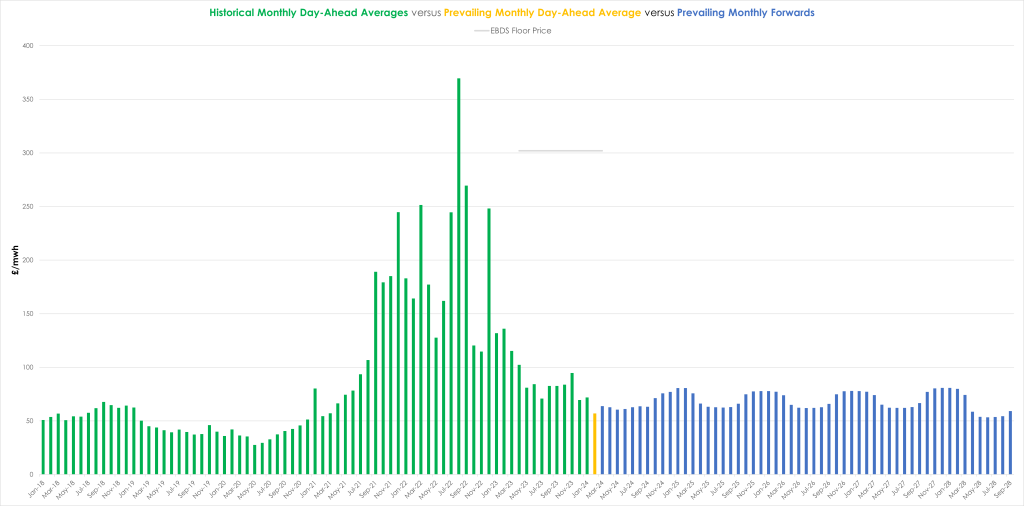

Back in the UK, our generation mix is bearish with renewables contributing 44% versus 23% gas-for-power burn.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £57/mwh (or 5.7p/kwh).