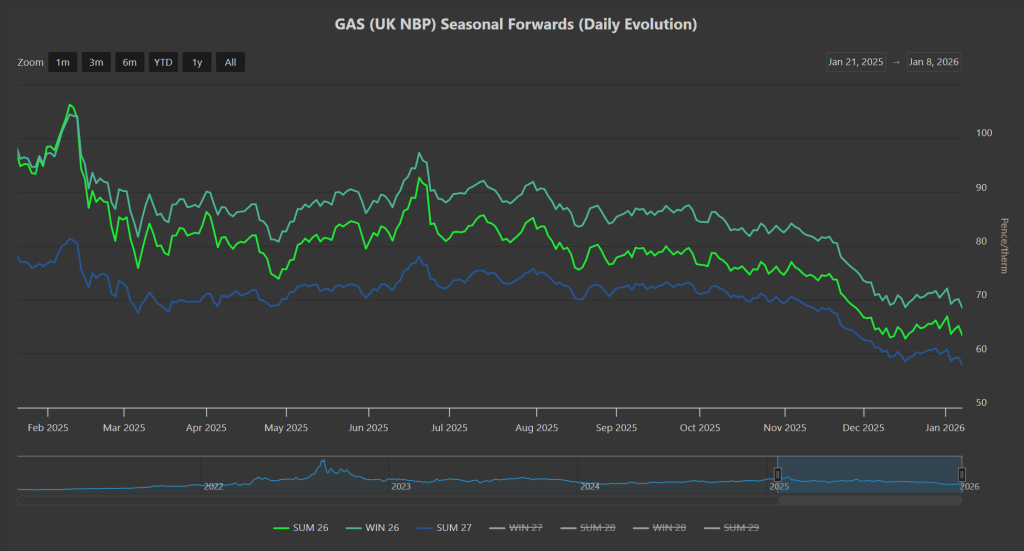

Of the front 3-Seasons (Summer-26/Winter-26/Summer-27), Summer-26 delivery prices have enjoyed the steepest decline – prices for Summer-26 delivery are now at a 40% discount versus the highs last seen in Winter-24 (please see chart below).

Prices opened lower again this morning despite the UK system being marginally short (demand outstripping supply forecast).

It looks as though prices will close down on the week off the back of milder weather forecasts resulting in lower gas-for-power burn and, accordingly, reduced storage withdrawals.

Beyond this weekend, temperatures above seasonal norms are expected to extend throughout northwest Europe.

In other news, despite the EU’s recent announcements that purchase of Russian gas by EU states will be outlawed by the end of ’26, data just released confirms that 76.1% of Russia’s Yamal exports went to the EU!

(Gas from the Yamal peninsula is exported via two separate methods: the Yamal–Europe pipeline (which goes to Poland and Germany) and the Yamal LNG project for shipping LNG.)

All in all, a quiet week to start the year, but both near-and-far term delivery prices continue to soften despite the intermittently wintry conditions.

Monthly Day-Ahead averages for January so far are holding steady at 76p/therm (or 2.6p/kwh exc. non-gas).

ELECTRICITY & CARBON

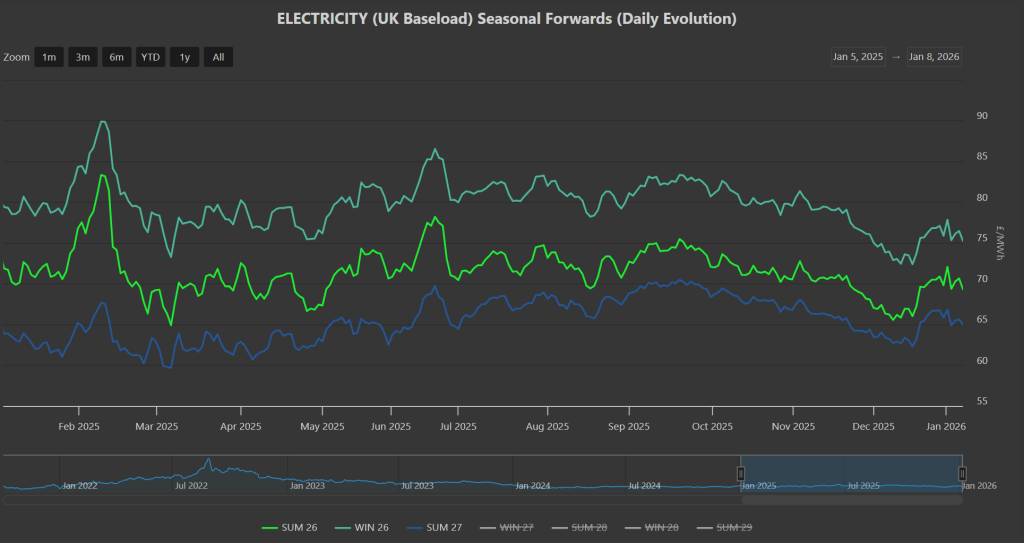

Of the front 3-Seasons (Summer-26/Winter-26/Summer-27), both Summer-26 & Winter-26 delivery prices have enjoyed the steepest decline – both are now at a 17% discount versus the highs last seen in Winter-24 (please see chart below).

Notably however, Summer-27 is barely altered versus its high last seen in Feb-25.

This reflects significantly less volatility in electricity versus the much wider swings seen in global gas prices over the last 12 months – which in turn is no doubt a reflection that electricity generation is relying less and less on gas-for-power burn (and more on renewables).

On the Carbon side of things, Dec-26 benchmark prices for UKAs are knocking on the door of £70/tn (currently at £69.25/tn on the mid-price).

UKAs “gapped-up” to the tune of 18% back in mid-December when the Dec-25 contract expired – though spot prices on the secondary market remain at an approximate £2/tn discount.

Today’s UK electricity generation mix is bullish in nature – specifically, renewables are contributing 31%, thermal at 35% (gas and coal) and low carbon at 19% (nuclear and imports).

Monthly Day-Ahead averages for January so far are looking very wintry at £104/mwh (or 10.4p/kwh exc. non-energy).