The EU’s determination to further reduce Russian gas flows is likely intended to give Europe scope to negotiate delivery of more US LNG (so as to soften Trump’s tariff attack).

However, until such a time as more US LNG is made available, market participants are regarding the loss of Russian gas flows (primarily to Slovakia and Hungary) as contributing to supply tightness – and so, price supportive.

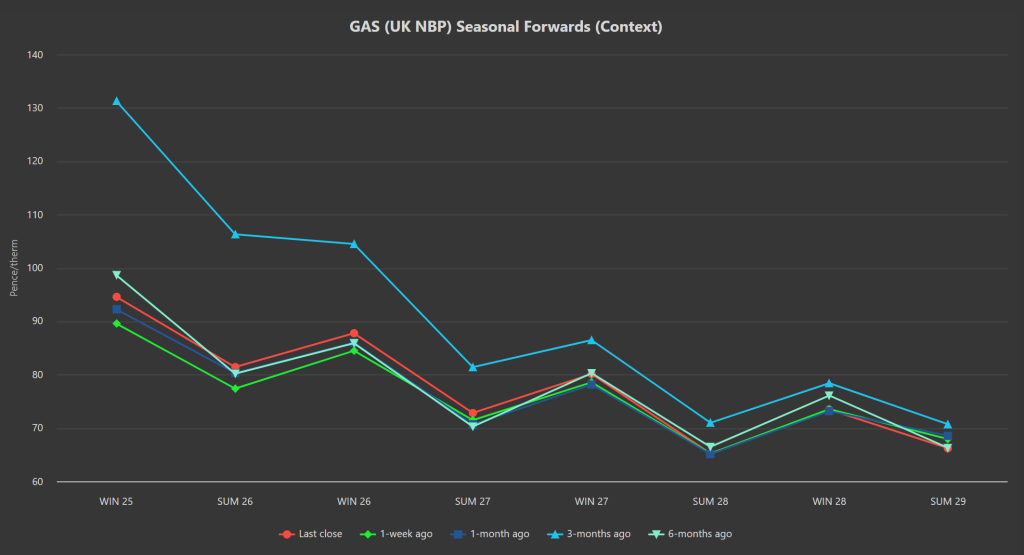

As such, we’ve seen a steady rise in prices over the course of the week with delivery all the way down the curve marginally up on the week/month (please see chart below).

The EU knows full well that an inevitable outcome of the US and Russia reaching a bilateral ‘peace’ agreement (at Ukraine’s expense) would be the resumption of Russian flows (someway,somehow).

In pre-empting such an outcome by reasserting the EU’s commitment to sanctions against Putin’s aggression, they’re ensuring that Europe gets a seat at the negotiating table with Trump on their own terms.

Unfortunately, such a move is at the expense of European/UK energy buyers, for whom prices will stay high so long as Russian flows are kept out of the European system (and additional US LNG delivery remains to be confirmed).

The EU’s other gambit (to keep a lid on bullish momentum) has been to tentatively propose a loosening of storage targets in time for Winter-25.

The draft law proposes reducing the fullness target from 90% to 83%, to be met at any point between 1 October and 1 December each year (until further notice).

Member states would be expected to ensure that the cumulative impacts of ‘flexibilities and derogations’ do NOT leave overall storage obligations below 75% by these dates.

On the supply side, LNG deliveries to Europe/the UK have also dropped off a little this last week against a backdrop of increased seasonal Norwegian outages (reducing pipeline flows) – so, inevitably, with supply dropping amid a cold, still few days, prices have found additional support.

With the tightening of the European gas balance in recent days, market participants are naturally concluding that Europe cannot afford a further significant drop in prices (at the risk of losing more LNG volumes to Asia) – so prices will need to remain inflated to ensure cargoes continue to head our way.

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst the going’s good – and whilst so many geopolitical variables remain outstanding.

This month’s UK gas Day-Ahead averages have risen marginally over the last fews days, and now stand at 80p/therm (or approx. 2.7p/kwh excluding non-gas).

ELECTRICITY & CARBON

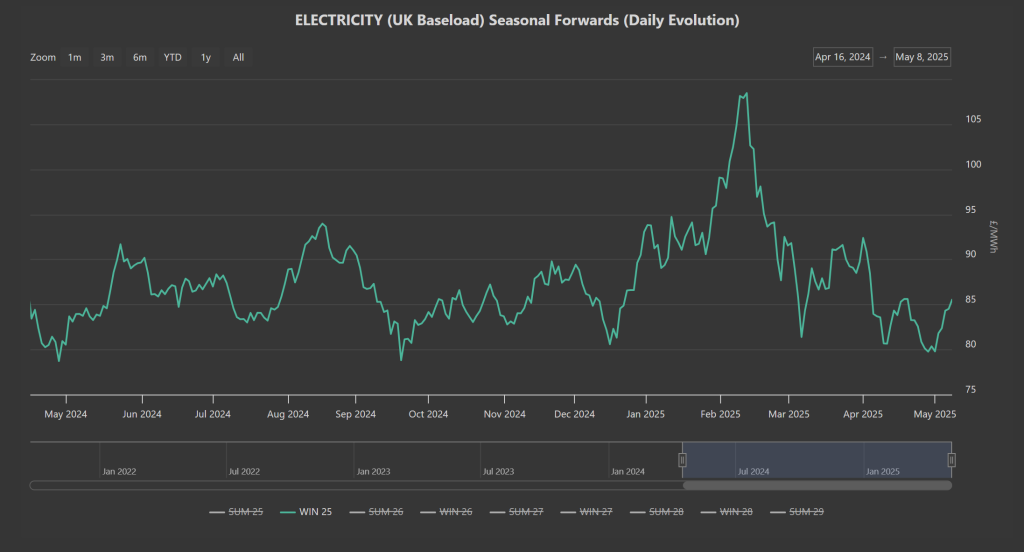

Electricity continues to mirror gas movements.

Notably, Winter-25 prices keep knocking on the door of £80/mwh but have yet to sustain a break to the downside.

Attempts to break below this new psychological level failed in Apr’24/Sep’24/Dec’24/Mar’25, then twice this month so far (please chart below).

So it’s fair to conclude that £80/mwh (or 8p/kwh) represents the market-bottom for Winter-25 right now.

On the Carbon markets, correlation away from gas and toward equities seems cemented, with prices continuing to smash through resistance to achieve higher-highs.

Likely drivers include Starmer’s determination to link European and UK Carbon markets, and so UKAs are rising toward higher EUA prices in anticipation of required parity.

Also, bullish speculators continue to eye the loss of free allocation to heavy-emitters come 2027.

Today’s UK electricity generation mix is bullish in nature reflecting cold, still conditions – with renewables contributing 19%, thermal at 33% (gas and coal) and low carbon at 27% (nuclear and imports).

So far this month, electricity Day-Ahead averages have seen an uptick this month, standing at £73/mwh (or approx. 7.3p/kwh excluding non-energy).

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst the going’s good – and whilst so many geopolitical variables remain outstanding.