For the time being, the anomalous backwardation of Summer-25 over Winter-25 (which first appeared back on 11th Nov ’24) is no more – please see chart below.

This reflects, surely, a heightened confidence amongst market participants of Europe’s ability to replenish storage inventories over the coming summer in time for Winter-25 conditions.

As things stand, Summer-25 is now at a comfortable discount to Winter-25 (so BAU has been restored).

Markets retraced some of last week’s losses to end the week amid expectations of lower temperatures to start this week.

No doubt, a significant chunk of this bullish retracement was driven by market participants covering short positions – but also it was likely a reaction to news of Russian forces retaking some of the Kursk region (adding weight to Putin’s negotiating position).

Geopolitically, the markets could do without the intensification of Russian attacks on Ukrainian gas production infrastructure, which only serves to further weaken prospects for a ceasefire.

On the demand side, (as expected) temperatures are set to fall back below seasonal norms by the end of the week, supporting near-trm delivery prices.

This coupled with wind outputs below seasonal norms with inevitably result in higher gas-for-power burn and the associated pressure on withdrawals.

Storage is now at 36.8% (below the 2018 to 2024 average) – but above this point in 2021 and 2022.

For month-ahead LNG deliveries at least, (due to falling prices) Europe is losing its attractiveness compared to Asia – further highlighting what a difference it would mke to supply/demand dynamics were Russian flows be reintroduced to the European system.

Monthly Day-Ahead averages for this month so far are on track to improve on last month’s final number (124p/therm), with averages at 102p/therm at the time of writing (or approx. 3.48p/kwh excluding non-gas).

ELECTRICITY & CARBON

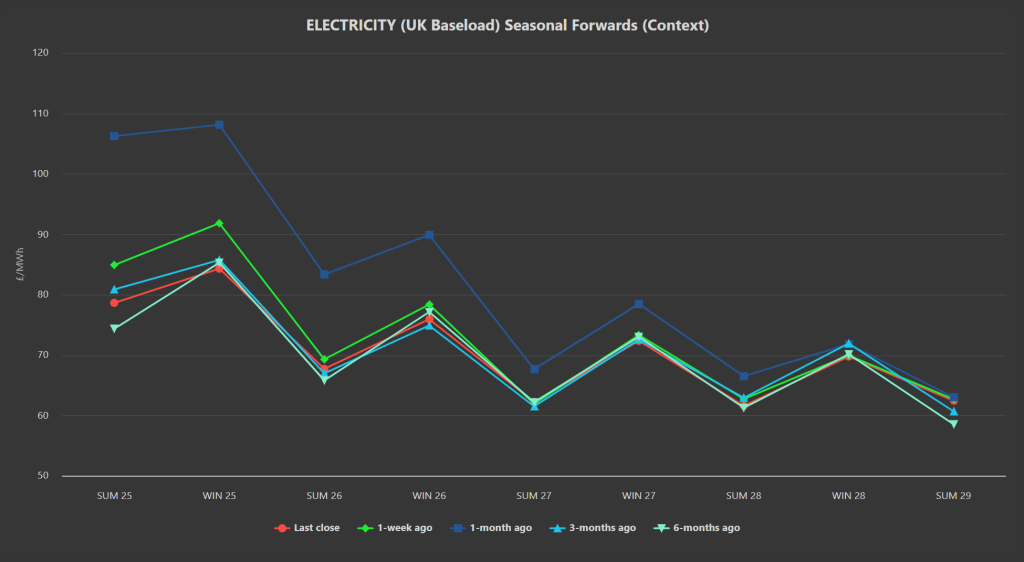

Seasonal Forwards are now down on the week, the month, 3-months ago – and commensurate with 6-months ago (please see chart below).

As you’d expect, electricity prices have followed much of the gas retracement we saw during Friday’s session.

Following this weekend’s benign weather conditions, market participants are now eyeing the impending cold spell,

Global economic data is increasingly pointing toward a slowdown (amid ongoing Trump tariff threats) – should lower interest rates fail to stimulate improved activity, demand will inevitably fall.

Today’s UK electricity generation mix however, is bearish in nature with renewables contributing 53%, thermal at 12% (gas and coal) and low carbon at 22% (nuclear and imports).

The Carbon markets remain closely correlated to fossil fuel prices – so as you’d expect given recent price falls, EUAs and UKAs are mirroring.

Talk of Starmer’s intentions to merge EUAs/UKAs has gone from the headlines, and UKAs resumed their bearish bias with a confirmed downward trend channel forming back on 10th Feb.

Prices (now at £39.35/tn on the mid) fell out of the bottom of the long-term bullish trend channel on 20th Feb, then retested this resistance level from beneath on 27th Feb, rejecting to the downside.

If prices sustain a break below £39/tn, the next target below is £37/tn as per the high of 3rd Jan.

UK electricity Monthly Day-Ahead averages so far for this month are back below £100/mwh and sliding – now at £90/mwh (or approx. 9p/kwh excluding non-energy).