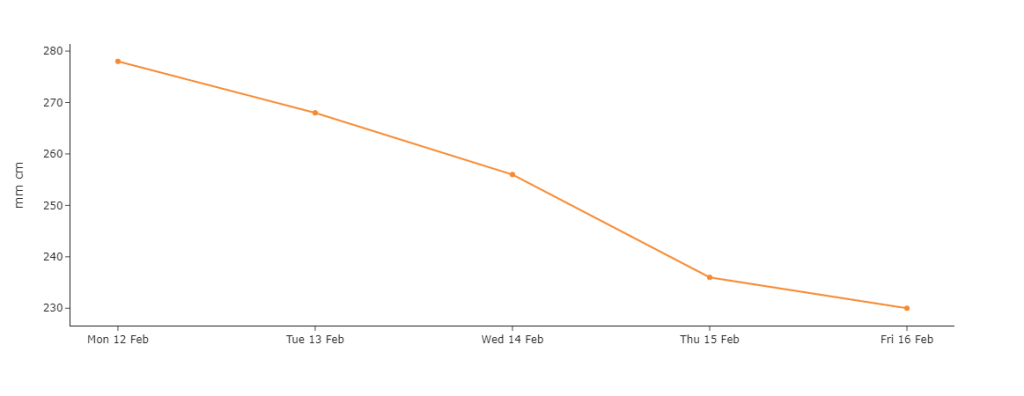

Demand is forecast to fall throughout the week (see chart).

Higher temperatures and wind outputs saw prices open lower this morning despite a marginally short UK system (demand outstripping supply).

Other key drivers remain bearish with Norwegian flows at capacity (no outages) and even higher temperatures expected as we approach the weekend.

Whilst geopolitical risk is stopping the markets from falling off a cliff, the impacts of Ukraine and Red Sea LNG transit problems on the supply/demand dynamic are evidently limited.

With Summer-24 now on the horizon (only 49 days away), historically high European gas storage (67% fullness versus the 5-year average of 54%) and weak demand (against a backdrop of favourable weather conditions) continue to weigh on prices.

Monthly Day-Ahead averages are on target this month (so far) to achieve 70p/therm (or circa. 2.4p/kwh).

ELECTRICITY & CARBON ALLOWANCES

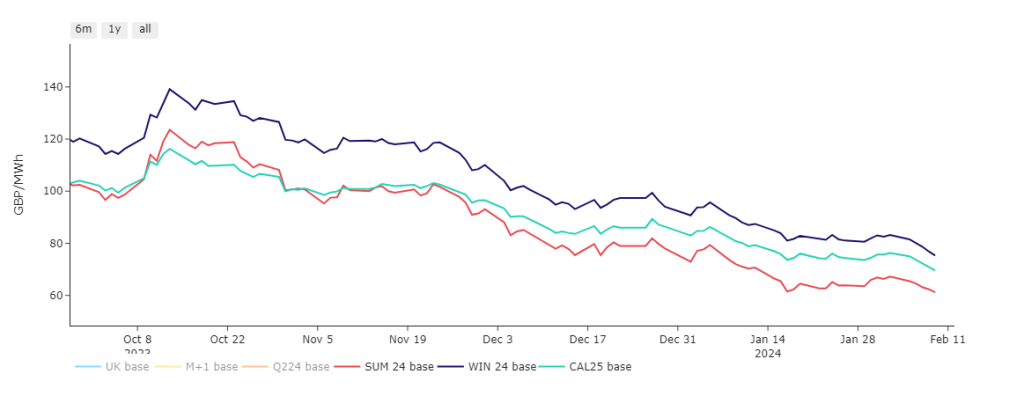

In mid-Oct ’23, Summer-24 delivery was briefly more expensive than CAL25 (calendar year ’25 delivery) reflecting a spike in short-term risk-premiums (see chart).

This risk-premium has now abated, with CAL25 now at a clear premium to Summer-24 (though still at a discount to Winter-24), reflecting the market’s belief that Summer-24 delivery is now soft (and growing softer) and next year as a whole is likely to be less expensive than Winter-24 (until further notice!)

Looking to the continent, short-term delivery prices have received some support from weaker renewable production, constrained French nuclear availability, and cooler temperatures.

Conversely, the market is facing pressure from declining fuel and emissions prices.

A rebound of wind, solar and nuclear production expected in the coming days (combined with temperatures rising back up to nearly 8°C above normal by Thursday) will likely weigh on near-term delivery prices as the week progresses.

Down the curve, bearish sentiment continues to prevail amid sustained demand destruction and comfortable supply dynamics.

On the European/UK carbon markets, bears are holding their own versus dip-buyers, with compliance players (Industrial & Commercial) seemingly waiting for further price drops or gradually accumulating spot stock for future surrenders.

Compliance buyers’ volumes don’t provide enough support to halt the carbon prices’ downtrend – so expect more downside if gas prices continue their slide!

Back in the UK, our generation mix is very bearish with renewables contributing 50% and gas-for-power burn at 32%.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £59/mwh (or 5.9p/kwh).