Last week finished on a bearish note, with Day-Ahead down by 4.5p/therm on the day (Fri vs Thurs).

Losses tracked European markets amid bearish pressure from summer levels of demand coupled with the scaling down of Norwegian maintenance over the coming days – likely resulting in higher flows to the UK/Europe (with flows now above the 5-day moving average).

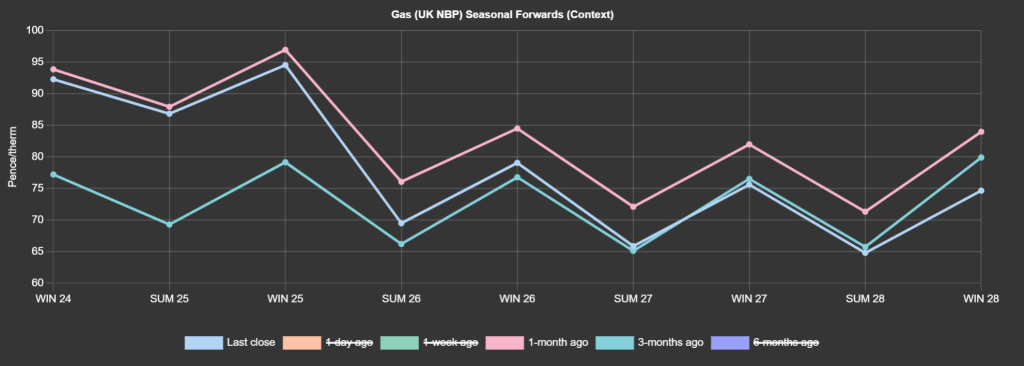

Seasonal Forwards are lower than 1-month ago, but still at a significant premium versus 3-months ago (before Middle East tensions escalated/Freeport LNG went offline/EU sanctions of Russian LNG) – see chart.

Context-wise, Norway has gone a long way toward replacing big chunks of Russia’s historical gas flows, having provided 30% of Europe’s gas since Russia’s invasion of Ukraine (with more than 100 billion cubic meters of gas being exported in 2023).

At the time of writing, the supply/demand balance to the UK remains in better shape than our European counterparts – which has prompted our Day-Ahead value to improve its relative discount when measured against European benchmarks.

The UK’s marginally more favourable supply/demand dynamic reflects ample supply to support healthy storage injections and improved exports to the Continent.

If the spread between UK Day-Ahead and European Day-Ahead (TTF) persists, the price differential will facilitate interconnector (IUK) exports into Europe.

Wind forecasts have seen an upwards revision to start the week but expect a drop off in renewable generation towards the back end of the week.

We’re again seeing a decline in LNG sendouts at South Hook (back down to 8mcm/d where it was just a couple of weeks ago).

Temperatures above seasonal norms and historically high gas storage levels continue to reduce the UK’s LNG demand – with only 1 cargo degasifying in May so far (though 3 more are expected).

Market participants still have the jitters over news that the EU will be sanctioning Russian LNG (giving rise to worries over supply tightness).

Monthly Day-Ahead averages are on target this month to achieve 72p/therm (or circa. 2.45p/kwh).

ELECTRICITY & CARBON

Looking to the continent, near-term delivery prices are weighed by improving solar and wind outputs, and forecasts of higher French nuclear availability as the week progresses.

On the carbon markets, Friday’s trading seems to highlight the strong resistance around 75€/t for EUAs (European Allowances), with bullish momentum failing to break higher to the topside.

As such, we’re likely to see some downside this week due to the evident lack of sufficent fundamental support.

UKAs (UK Allowances) are trading at £37/tn (Dec-24 benchmark).

Our electricity generation mix is bearish in nature today with renewables contributing 40%, thermal at 21% (gas and coal) and low carbon at 23% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £69/mwh (or 6.9p/kwh).

Monthly Day-Ahead averages for the month are now marginally higher than offers for Month-Ahead (June) at £65/mwh (or 6.5p/kwh) – perhaps reflecting a softer outlook as summer conditions start to take hold.