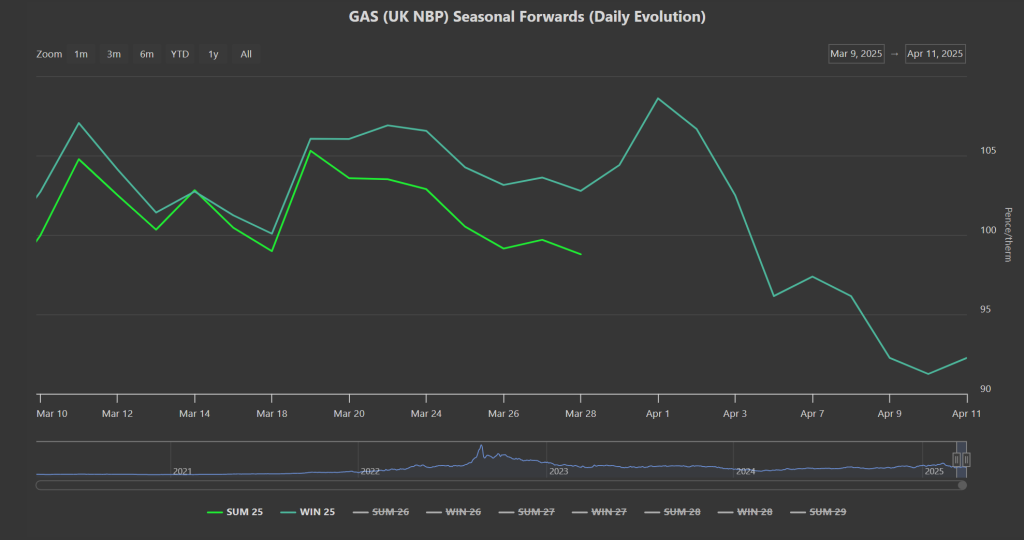

Notably, prices for Winter-25 delivery have now fallen below the closing price for Summer-25 delivery that was posted on Fri, 28th Mar (the last trading day before the onset of Summer-25 on 1st Apr) – please see chart below.

So how far can prices fall, and when is the best time to start hedging Seasonal Forwards?

Well, looking at the bigger picture, prices all the way down the curve are well below 100p/therm – something we’ve not seen since last summer.

But in the midst of the volatility caused by Trump’s tariff stand-off, how wise is it to continue to watch from the sidelines?

To answer that question, we need to consider what might make prices go back up.

Certainly, the primary bearish driver right now is that China will not be competing with Europe any time soon for LNG delivery (given the prohibitive cost of tariffs).

As such, Europe/the UK is under less pressure to raise prices to ensure LNG arrivals to our shores.

However, if Trump were to reverse course where China is concerned, prices would undoubtedly re-assume risk-premium and shoot up.

Another important bearish driver right now is the chance that Russia might turn the taps back on if a “peace deal” can be reached.

Whilst the tariff headlines have taken centre-stage for now, an underlying sentiment amongst market participants believes that ongoing (granted, bilateral) talks between the US and Russia will surely culminate in a favourable outcome for wider Europe (though likely at the expense of Eastern European security).

However, were the talks between the US and Russia to end suddenly in a blaze of insults and recriminations, we’d likely see a bullish response on the gas markets.

And so, the bearish sentiment is fragile.

As such, buyers need to be mindful that the bottom of this market may only come about if/when it becomes clear that we’ll successfully replenish gas stocks in time for Winter-25, and/or Putin and Trump engineer a means of getting more Russian gas flows into the European system – and so buyers would be wise to consider taking a “nibble” out of outstanding Forward volumes whilst the market is soft, with a view to hedging more if/when we see further downside.

This month’s gas Day-Ahead averages so far are falling as the month progresses – now at 88p/therm (or approx. 3p/kwh excluding non-gas).

ELECTRICITY & CARBON

Electricity values are holding steady all the way down the curve at sub £85/mwh.

On the Carbon markets, UKAs have reacted bullishly to Trump’s climb-down on reciprocal tariffs (with investment speculators still net long and emissions increasingly developing a correlation with equities).

However, if gas prices see a sustained bear run over the coming months, how long can Carbon resist a fall?

However, for today at least, Dec-24 UKAs are back up at £46.63/tn and re-testing the upper extremity of a long term bearish trend channel – please see chart below.

Today’s UK electricity generation mix is bearish in nature, with renewables contributing 42%, thermal at 19% (gas and coal) and low carbon at 26% (nuclear and imports).

So far this month, electricity Day-Ahead averages are on target to achieve £77/mwh (or approx. 7.7p/kwh excluding non-energy).