Markets are thin and spiky to start the week – this despite a long UK system (supply outstripping demand forecast) and ‘summery conditions’ (warm and windy).

This is always a danger when markets fail to probe lower, market participants will then test the upper envelope of the tight trading range to gauge where the risk is.

European month-ahead gas prices this morning are knocking on the door of a two-week high (though it’s been a relatively flat two weeks).

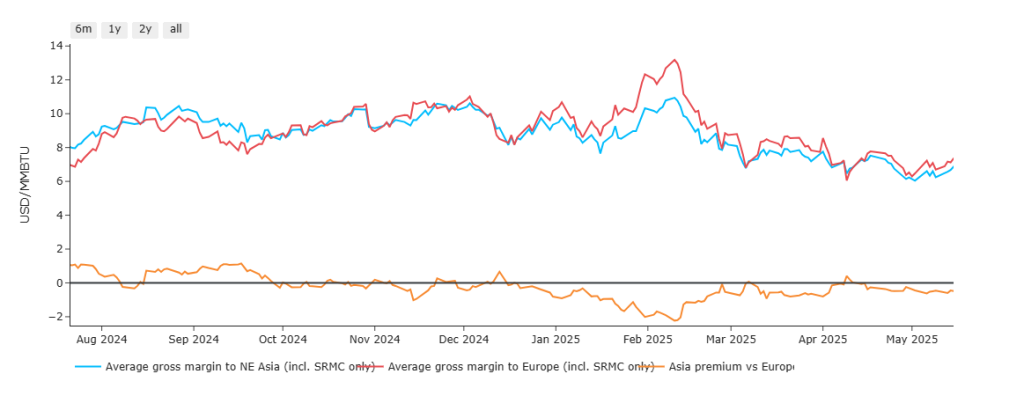

Whilst US LNG cargoes are still making more money by heading to Europe over Asia (please see chart below detailing US LNG Netbacks – Asia versus Europe), it’s worth noting that demand across Asia has been inching up this past week to accommodate cooling demand.

By way of explanation, SRMC (Short Run Marginal Cost) denotes the cost of producing an additional unit of LNG in the short term, and netbacks represent the effective price received by an LNG producer after accounting for transportation and other costs.

Looking forward, fundamentals are set to soften, with the second half of the year seeing an extra 7 million tonnes of LNG per annum (mtpa) coming online from the second phase of Plaquemines in the US, as well as another 14 mtpa from LNG Canada.

On the storage side of things, Europe’s inventories are now at 63% versus the 5-year average of 69% – so not drastically off the pace.

We’re in for another round of scheduled summer Norwegian maintenance in the coming days/weeks, which always contributes to jitters over supply tightness.

Nonetheless (for now), the UK system remains well supplied and demand is only marginally above seasonal norms.

As per our advice last week, when markets fail to make lower lows despite bearish market drivers, buyers need to take notice (as markets may very well now be too supported to facilitate any further downside this summer).

Monthly Day-Ahead averages for the month so far are holding very steady at 81p/therm (or approx 2.75p/kwh excluding non-gas).

ELECTRICITY & CARBON

Electricity prices are marginally up, but the increase lacks conviction/trade volume – nonetheless, Seasonal Forwards are up versus 1-week ago.

Winter-25 is at £87/mwh (last printed 30th May) – so down 10% versus the highs of 19th Jun; and up 10% versus the lows of 29th Apr (very range-bound!)

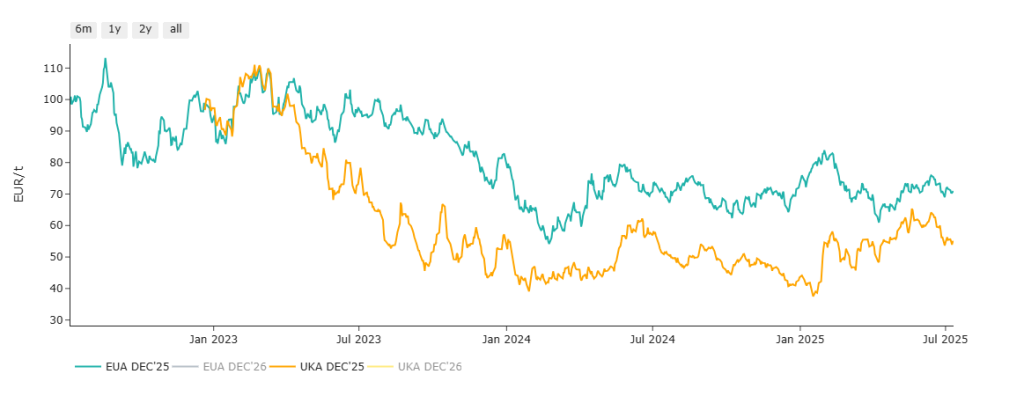

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

However, when comparing EUAs with UKAs (measuring both in Euros), UKAs remain ‘heavier’ and have yet to return to parity with EUAs (and continue to enjoy a significant discount – please see chart below).

At the time of writing, Dec ’25 UKA benchmark prices are at £47.77/tn on the mid-price (a drop of 12% versus 13th Jun) – next meaningful area of support is £44/tn but rumour has it that significant BUY orders are building at £45/tn – so a prudent trade would be a BUY entry at £45.50/tn (so as to not miss the opportunity to get in).

Today’s UK electricity generation mix is bearish in nature reflecting benign ‘summery’ weather conditions, limiting gas-for-power burn – specifically, renewables are contributing 48%, thermal at 8% (gas and coal) and low carbon at 27% (nuclear and imports).

Monthly Day-Ahead averages for the month are at £76/mwh (or approx 7.6p/kwh excluding non-energy).