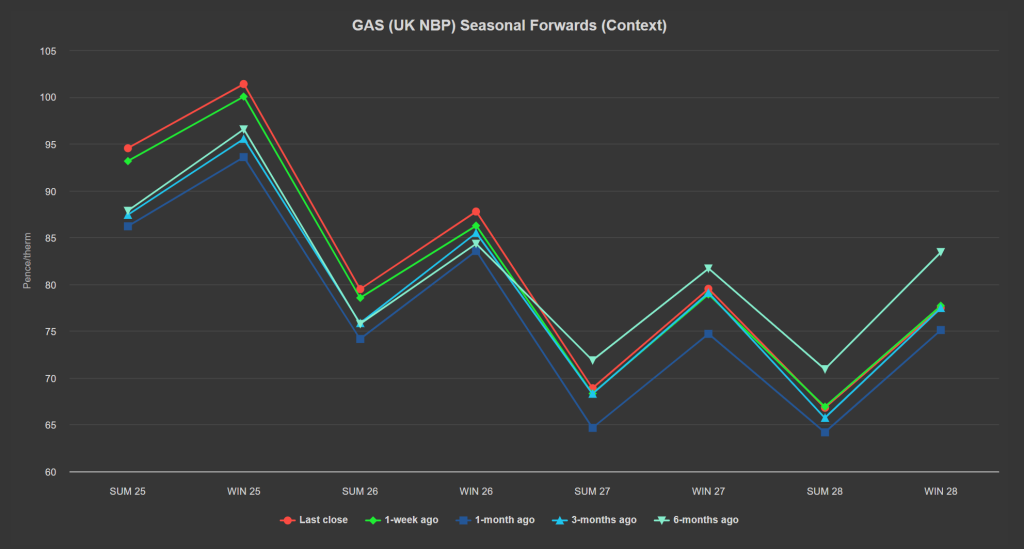

With the onset of Winter-24, Seasonal Forwards have seen a minor boost with prices up on the week/month/3-months/6-months (see chart below).

Low temperatures, subdued wind outputs and relentless geopolitical disquiet are the primary supportive elements contributing to renewed (but modest) bullish momentum.

Our system opened short this morning (demand forecast outstripping supply) with total demand above seasonal norms.

Unscheduled Norwegian maintenance has taken 30 million m³ offline – with Oseberg Field Centre in the North Sea the latest field to fall foul of compressor failures.

The Middle East escalation continues apace with a drone strike on an Israeli military base overnight contributing to fears over impending supply disruptions.

Conversely, oil has dropped off a bit to start the week in response to more weak economic data coming out of China – new bank loans have fallen to a 15-year low, export growth has slowed and factory outputs are significantly down amid muted domestic demand.

Increasingly, Chinese economic indicators are reinforcing fears of deflation and underline the need for meaningful stimulus measures – though the Communist Party remain reluctant to devalue the yuan and trigger capital flight (which seems inevitable).

Looking into next week, milder weather forecasts point above seasonal averages against a backdrop of very healthy European MRS (mid range gas inventories) – currently at 95% versus the 5-year average of 90%.

Monthly Day-Ahead averages so far this month are on target to achieve 96.839p/therm (or approx. 3.304p/kwh excluding non-gas).

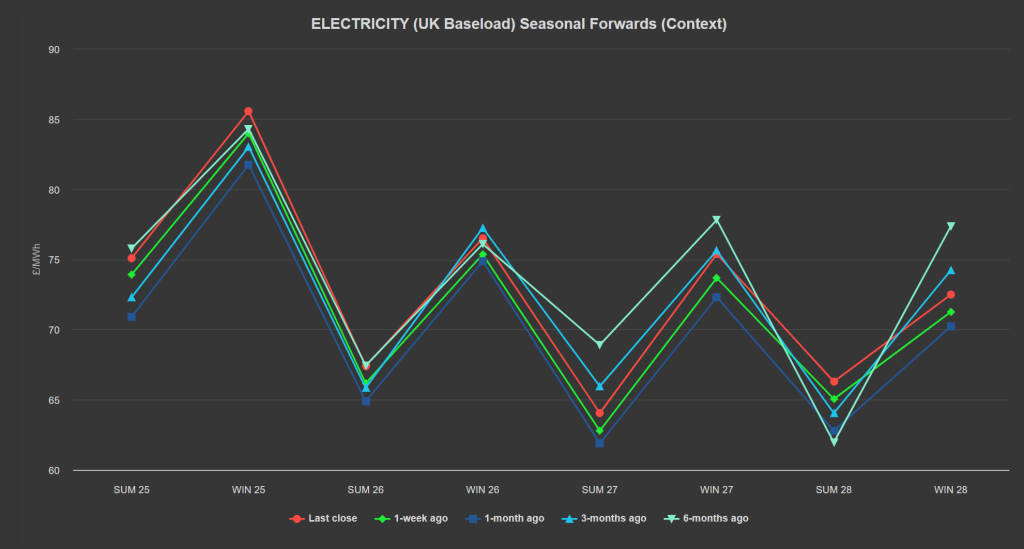

ELECTRICITY & CARBON

Starting with Carbon today, EUA found resistance last week at €65/tn.

Prices closed on Friday at €64.62/tn, but went as low as €63.75/tn intraday.

Whilst EUAs Dec ’24 benchmark contract gained 4.14% last week past week, this was not sufficient to offset the previous’ week losses of -6.45%.

So, it’s fair to say we’re seeing increased volatility on the emissions markets.

UKAs are on a bullish retracement having tested £35/tn on the mid-price – now at £38/tn – though Wednesday’s auction settlement (if low) will bring about a continuation of the downtrend.

UK electricity prices remain comfortably below £100/mwh front to back, all the way down the curve.

Our electricity generation mix is bullish in nature today with renewables contributing 18%, thermal at 52% (gas and coal) and low carbon at 13% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £82.101/mwh (or approx. 8.21p/kwh excluding non-energy).