Notably, on 4th Jan, Day-Ahead broke above Month/Quarter/Season-Ahead and remains at a marginal premium (see chart).

Of course, this reflects the market’s perception that very short-term delivery carries more risk than mid-term – which bodes well for delivery prices Feb and beyond.

At this morning’s open, near-term delivery contracts were down versus Friday’s close, most likely off the back of a LONG system (supply outstripping demand) and improved wind outputs to start the week.

Down the curve, gas contracts are also lower, with a test of 70p/therm potentially on the cards.

Despite inevitable storage withdrawals over the recent cold spell, European storage remains in unseasonably great shape at an impressive 80% versus the 5-year average of 69%.

Will this bearish trend have the momentum to break 70p/therm for near-term delivery?

Well, on the bullish side, Qatar has now stopped exporting via the Red Sea due to escalating tensions and worsening rhetoric across the Middle East.

China’s LNG import capability is forecast to increase y-o-y until beyond 2026 – no doubt increasing competition (and cargo values).

It looks like we’re in for a sub-zero temperature spell, with heating demand and gas-for-power burn likely to exceed seasonal averages all week.

Fortunately, rising temperatures accompanied by wet and windy conditions are expected into the weekend.

Monthly Day-Ahead averages are on target this month to achieve 81p/therm (or 2.76p/kwh).

ELECTRICITY & CARBON ALLOWANCES

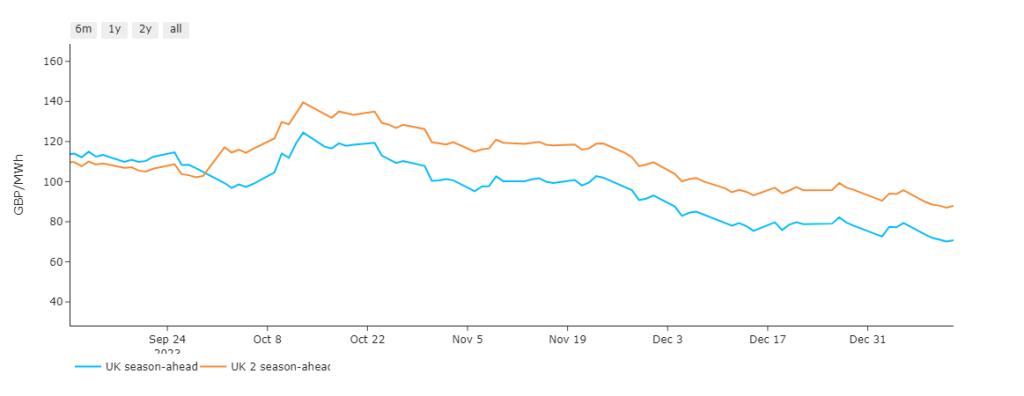

Notably, Season-Ahead and 2-Seasons-Ahead have been on the slide since mid-Oct ’23 (see chart) – flying in the face of traditional winter premiums.

Looking to the continent for price direction, European short-term delivery prices came under pressure over the weekend against a backdrop of improved renewable outputs and French nuclear availability – this despite temperatures lingering below seasonal norms.

The European markets look likely to find some support this afternoon from expectations of a drop in wind outputs for tomorrow.

Escalating concerns about potential attacks on commercial shipping in the Red Sea continue to support longer-term delivery prices.

Nonetheless, gains are limited as the fundamental drivers remain comfortable i.e., robust supply and sustained weak demand.

Carbon prices fell this morning, with participants eyeing milder and windier weather forecasts for the end of Jan (along with the resumption of the EUA auctions scheduled for Thursday this week).

Back in the UK, our generation mix is neutral to bearish, with gas-for-power burn at 45%, renewables at 40%; low carbon at 5% (nuclear and imports).

Monthly Day-Ahead averages are on target to achieve £79/mwh (or 7.9p/kwh).