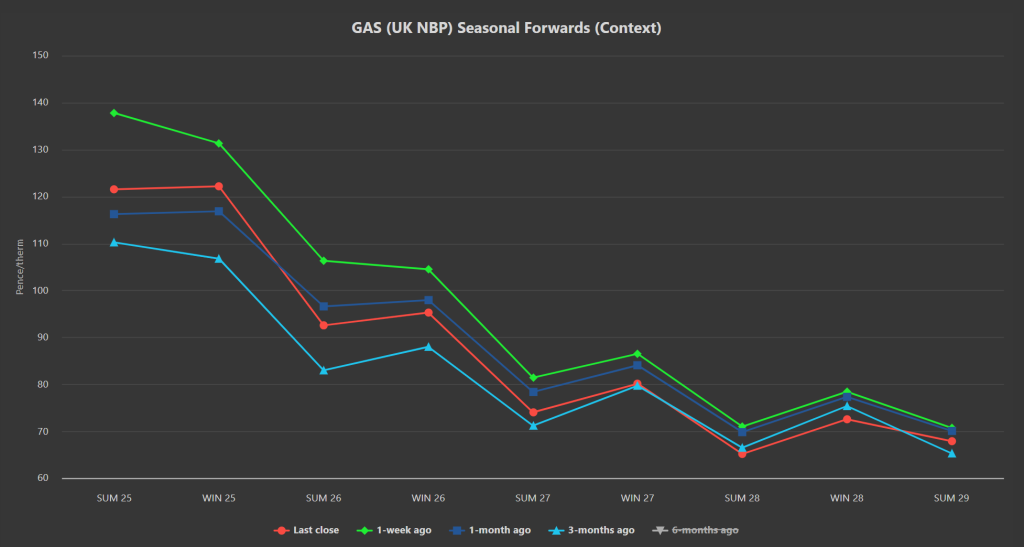

Seasonal Forwards are down on the week for delivery periods all the way out to the end of the curve (please see chart below).

The prospect of reduced storage constraints and of a peace agreement in Eastern Europe continue to exert downward pressure on European/UK gas prices.

The unwelcome anomaly of higher Summer-25 delivery prices than Winter-25 has been a key theme of this winter’s price-action so far – and once again, Summer-25 delivery has thankfully flipped below Winter-25 reflecting a diminishing fear over Europe’s ability to replenish gas stocks sufficiently in time for Winter-25 delivery (as per Summer-25/Winter-25 spread 1-week ago/3-months-ago on chart below).

Near-term delivery traded bearishly for the fourth day in a row on Friday driven primarily by weaker demand forecasts for the next few weeks (off the back of milder weather and improved renewables outputs).

Notably, UK Day-Ahead closed at a discount to benchmark European Day-Ahead prices last week for the first time since October – reflecting surely a looser supply/demand balance in the UK (which should lead to increased Interconnector exports to the continent, offsetting our generation costs).

Peace talks between Russia and Ukraine continue to be trailed, with European leaders jostling to stay relevant now that the US has seemingly taken the initiative (against a backdrop of European inertia).

Not surprisingly, talk of a peace deal has led to whispers of Russian gas flows into Europe resuming – of course, if this were to come to pass, both near- and far-term prices would fall off a cliff.

Encouragingly, Europe (primarily Germany and France) are urging a fresh look at mandated storage levels, suggesting the current 90% target by 1st Nov ’25 sends a signal to the market that European buyers are obliged to buy, driving up prices.

As such, a loosening of the mandated level looks likely (which should help to keep a lid on any remaining wintry, bullish fervour).

This, in addition to rumours that EU leaders may also be willing to impose a price cap, looks to have been enough to encourage speculators to reduce “long” (buy) positions (with the onset of Summer-25 now only 42 days away).

European inventories are at 45% fullness (still below the 7-year average) after weekend temperatures stayed below seasonal norms, sustaining further withdrawals.

However, toward the end of this week we’re expecting temperatures to flip to significantly above seasonal norms for the remainder of the month (mitigating storage withdrawals alongside strong LNG arrivals).

Monthly Day-Ahead averages for this month so far are at 133.786p/therm (or approx. 4.565p/kwh excluding non-gas).

ELECTRICITY & CARBON

As you’d expect, electricity prices are tracking gas delivery with Seasonal Forwards down all the way out to the end of the curve.

On the Carbon markets, emission prices are falling in line with gas too.

Talk of Starmer’s intentions to merge EUAs/UKAs has abated for now, and UKAs look heavy – having failed to retest the upper expremity of the confirmed bullish trend channel which began formation at the end of ’24.

Today, prices are falling again on low volume, with an internal bullish trend channel providing support at £45/tn, and an internal bearish trend channel having formed suggesting prices will fall to £44/tn – please see chart below.

Today’s UK’s electricity generation mix is neutral with renewables contributing 35%, thermal at 39% (gas and coal) and low carbon at 19% (nuclear and imports).

Monthly Day-Ahead averages so far for this month are at at £118.137 (or approx. 11.82p/kwh excluding non-energy).