Well, the week has started with four seasons in one day – with prices being significantly up at the open, then sideways through the morning, now sliding to well below Friday’s close, and it’s only mid-afternoon!

Traders and risk-managers alike have been left scratching their heads as sentiment swings from hope to despair, then back again – right now, it would seem Iran’s latest 14 point proposal to end the stalemate (submitted to Pakistan) has taken a bit of the heat out of this morning’s panic.

As is his MO, Trump used the weekend to make his comments, this time it was to remind Iran that the “clock is ticking”.

Then yesterday, the UAE said a drone strike had triggered a fire near its nuclear power station, calling the incident a “dangerous escalation”.

Thereafter, Saudi Arabia confirmed it had intercepted three drones that had seemingly been sent from Iraqi airspace.

So, not surprisingly, when the markets opened this morning (amid more bad news news that the Australian LNG strike will be going ahead as of 20th May) the prices went off like a rocket.

About 20 minutes ago in a media briefing, Iran’s Foreign Ministry reiterated that nuclear enrichment is a right that “already exists”.

So, evidently, back-channel negotiations persist – as such, this morning’s bullish rally has run out of steam, and we’re back to square one.

We maintain that the US stands to gain more than anybody else from the status quo (with Qatar’s production out of action).

With Asian demand on the rise given higher temperatures (and so higher HVAC), the US looks set to cash-in (so long as the Strait remains closed).

However, we can’t ignore that Trump’s approval ratings continue to slide, with mid-terms now only 5 months away.

We’re told the US is ramping up oil and gas production to mop up the slack, with smaller independent drillers leading the domestic push by quickly hiring more fracking fleets, while refiners are also boosting their output of gasoline, diesel, and jet fuel.

In other measures designed to help the world/profit from the shortages caused by the war, Trump’s Administration is urging regions like Alaska and the Gulf Coast to pull out all the stops and drill, baby, drill!

In addition, The US Department of Energy has released over 53 million barrels of oil to the international market – though I’m confident markets would forego all of the US’ help in favour of the Strait re-opening.

European storage is at 36% versus the 5-year average of 45% – so injections are starting to slow a little bit.

Lower than seasonal norm temperatures across Europe are increasing gas-for-power burn (pressuring withdrawals, limiting injections).

FLEX buyers with open volumes for June delivery remain on the sidelines pending a meaningful dip in price.

Monthly Day-Ahead Averages for the month have crept up to 117p/therm (or 4 p/kwh exc. non-gas).

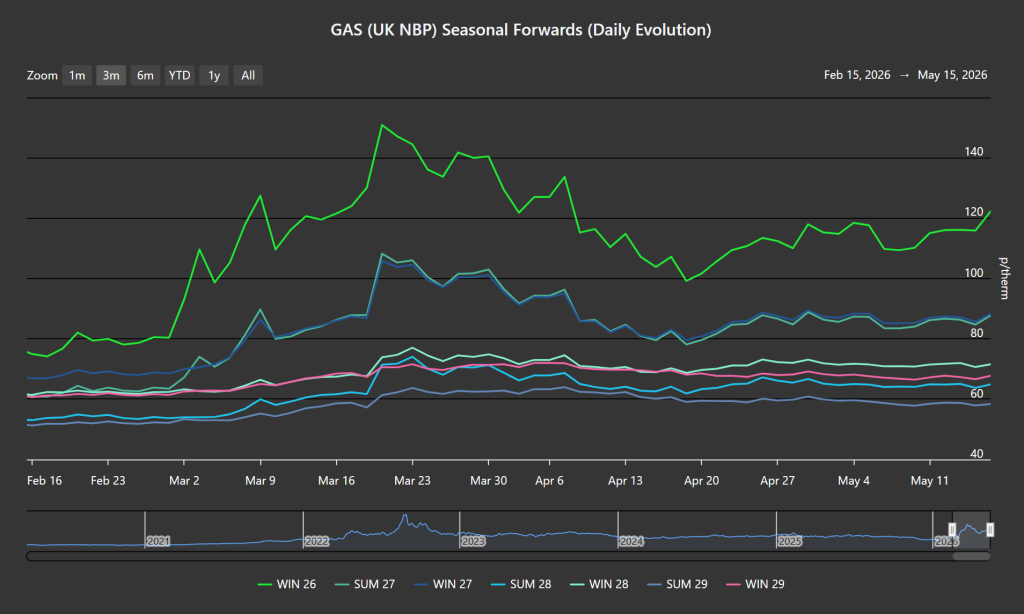

As per the chart below, the front 3-Seasons are feeling the brunt of the uncertainty, with Seasonal Forwards thereafter only marginally inflated versus pre-war levels.

ELECTRICITY & CARBON

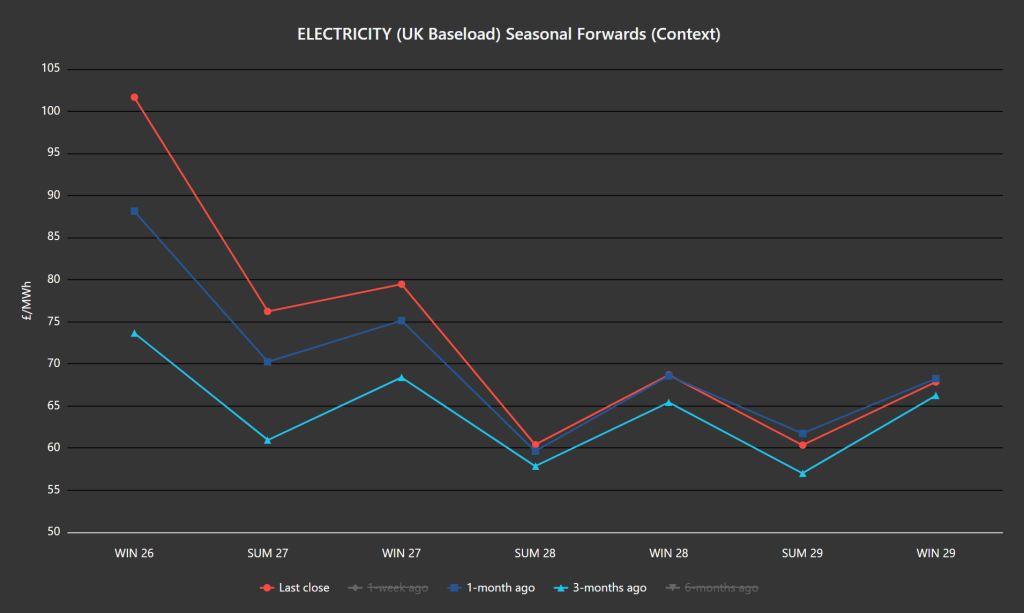

Whilst UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb, I’m afraid the bulls are starting to impact value marginally for Winter-26 delivery.

Today’s UK electricity generation mix is a little bullish in nature – specifically, renewables are contributing 32%, thermal at 34% (gas and coal) and low carbon at 22% (nuclear and imports).

FLEX buyers with open volumes for June delivery remain on the sidelines pending a meaningful dip in price.

The chart below details Seasonal Forwards versus 1-month/3-months ago.

As you can see, the risk-premia is built into the front 3-Seasons – beyond which, FLEX buyers are still able to access comparatively solid value beginning Summer-28.

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets.

However, correlation shifted to equities throughout March (which continue to enjoy a strong, tech-led upwards momentum).

At the time of writing, UKA mid-price Dec ’26 delivery is at £51.37/tn (and the spot is at early-50s).

Monthly Day-Ahead Averages for UK electricity for May so far are holding steady at £101/mwh (or 10.1 p/kwh exc. non-energy).