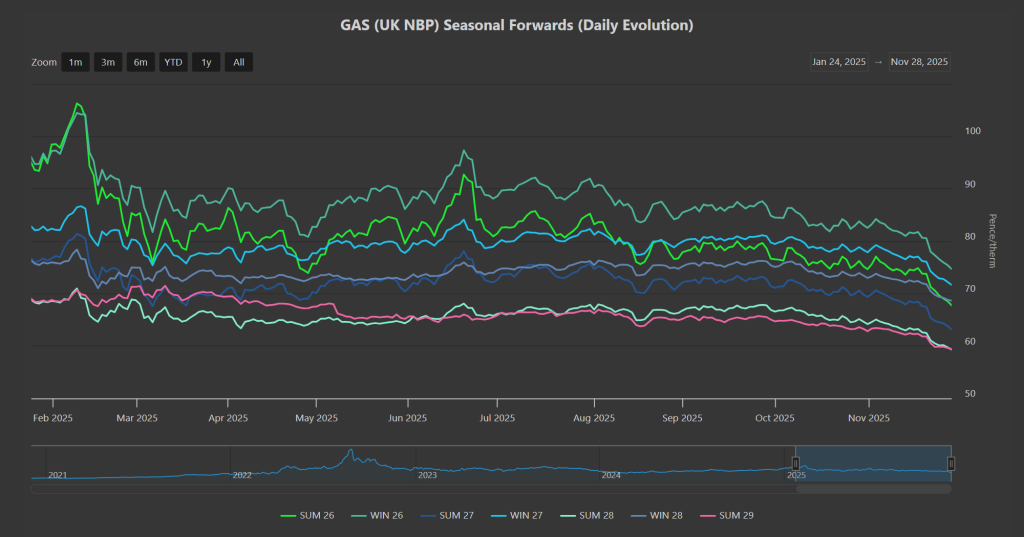

Seasonal Forwards are generally around 30% lower than the prices printed at the height of last winter, and very clearly on the slide again today (for the 7th consecutive session) – please see chart below.

This morning, near-term delivery (Day-Ahead/Week-Ahead/Month-Ahead) opened lower off the back of a long UK system (supply outstripping demand forecast).

The primary bearish drivers are steady supply, milder weather, ongoing Ukraine/Russia talks, and rumours of an LNG glut come next summer.

Temperature forecasts are predicting near or above seasonal norms across most of Europe for the coming fortnight, inevitably lowering heating demand (and gas for power burn/storage withdrawals).

European storage fullness is at 76% versus the 5-year average of 87%.

Monthly Day-Ahead averages for November came in at 76p/therm (or 2.6p/kwh exc. non-gas).

Monthly Day-Ahead averages for December so far are at 73p/therm (or 2.5p/kwh exc. non-gas).

ELECTRICITY & CARBON

Electricity Seasonal Forwards all the down the curve are mirroring bearish gas movements.

On the Carbon side of things, UKAs continue to trade below the increasingly important resistance level of £58.50/tn, but have failed to fall back (yet) to the increasingly important support level of £55.50/tn – however, as per the chart below, prices on the 15-minute charts have just fallen through key support following a week of bulls failing to break-above key resistance levels.

Next stop is likely to be a retest of £55.50/tn.

Today’s UK electricity generation mix is neutral in nature, neither bullish not bearish – specifically, renewables are contributing 36%, thermal at 28% (gas and coal) and low carbon at 20% (nuclear and imports).

Monthly Day-Ahead averages for November came in at £77/mwh (or 7.7p/kwh exc. non-energy).

Monthly Day-Ahead averages for December so far are at £74/mwh (or 7.4p/kwh exc. non-energy).