Prices have been marginally firmer today versus last week’s close.

Temperature-related low demand over the coming fortnight should keep a lid on European prices – though a bullish undercurrent is brewing as the impacts of the climax of the Norwegian scheduled maintenance season take hold.

100 mcm (million cubic metres) is now offline and this level of depleted flow is expected to persist for several weeks.

Over the weekend, Yemeni Houthis launched a missile at an Israeli-owned vessel in the Red Sea – as we’ve seen before, if the frequency of these attacks increase (and is not isolated to Israeli transit), cargoes will be forced to head around the Cape of Good Hope (delaying delivery times, and tightening supply).

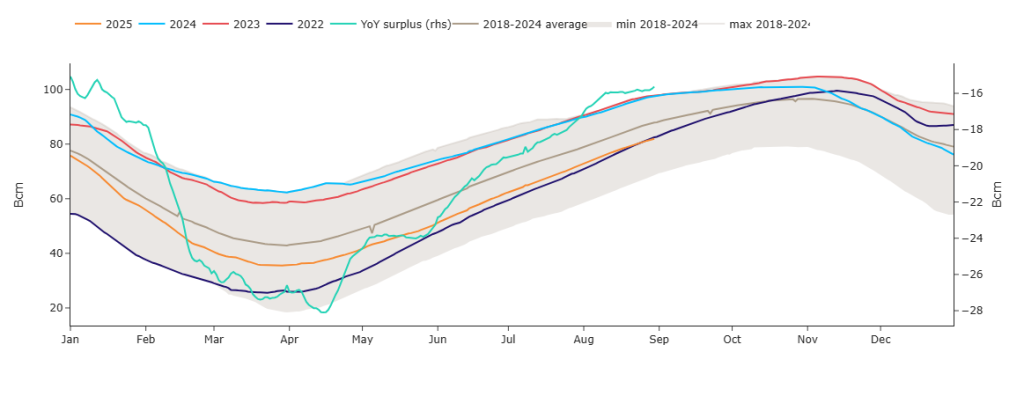

European storage fullness is now at 82% versus the 7-year average of 88% (please see chart below) – though injections will slow over the final weeks of Summer-25 due to Norwegian pipeline maintenance.

Any late buyers of Winter-25 delivery are still advised to get in BEFORE the 2nd week of September at the very latest.

Monthly Day-Ahead averages for August achieved 79p/therm (or 2.7p/kwh exc. non-gas) – this month has begun at the same level.

ELECTRICITY & CARBON

Prices have firmed a little today in line with firmer gas Forwards.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices have broken to the topside off the back of impending closure to the summer season – prices are back up at £54.36/tn on the mid-price (so a restest of the highs of Jun-25 looks likely -please see chart below).

having fallen below support to start the week but now retesting resistance – in short, it’s rangebound price action with prices having traded within a 15% bracket since the onset of Summer-25 (1st Apr).

Today’s UK electricity generation mix has been very bearish in nature – specifically, renewables are contributing 71%, thermal at 7% (gas and coal) and low carbon at 18% (nuclear and imports).

Any late buyers of Winter-25 delivery are still advised to get in BEFORE the 2nd week of September at the very latest.

Monthly Day-Ahead averages for August achieved £71/mwh (or 7.1p/kwh exc. non-energy) – this month has started at £68/mwh (or 6.8p/kwh exc. non-energy).