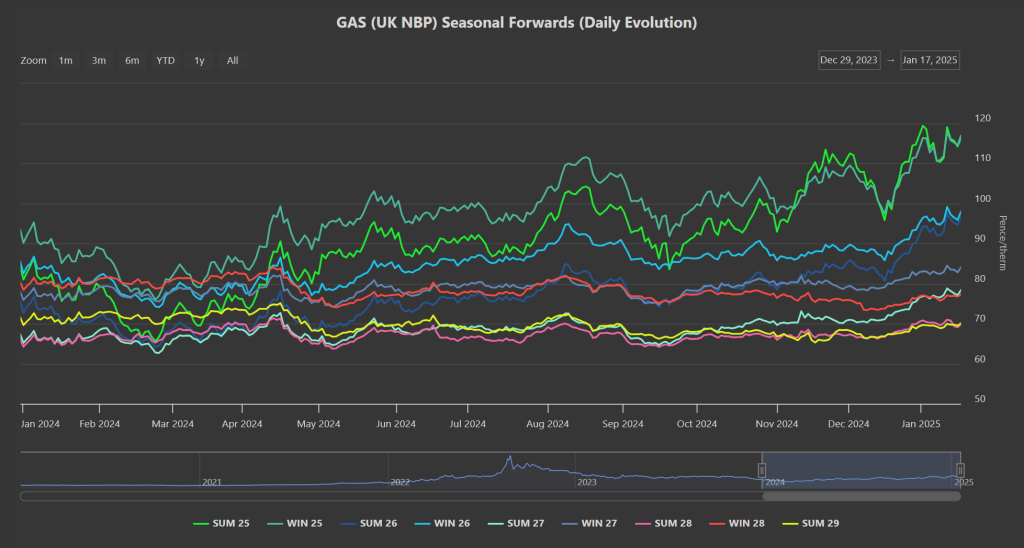

Front-end gas prices remain supported amid a short UK system (demand forecast outstripping supply) and poor wind outputs (increasing gas-for-power burn and storage withdrawals).

Whilst Israel and Hamas have agreed a shaky truce for now, markets nonetheless should start to price-in reduced risk derived from improved supply security.

As we’ve reported previously, Trump’s return to The White House should mean more supply – so improved supply/demand dynamics.

LNG arrivals into Europe/the UK are nice and steady off the back of depressed demand across Asia attributed to unseasonably mild conditions and lower demand (so lower gas prices).

As such, cargoes continue to follow the money to Europe with at least six cargoes this month originally destined for Asia being rerouted to Europe (which should help plug the gap of the lost flows heading into Europe via Ukraine now that the transit deal has come to an end).

All eyes remain on European storage fullness (now at 61% versus the 5-year average of 68%, but still in the middle of the 8-year range).

So, whilst Europe continues to burn through inventories during cold spells (when wind outputs are low), Month/Quarter-Ahead contracts appear to be holding steady – suggesting that risk-premium associated with fears over replenishing gas reserves this coming summer have already been baked into prices.

In the face of supply shortage worries, it’s worth remembering there are many projects underway globally to ensure that LNG exports continue to grow as much as 40% over the coming decade – with the lion’s share likely to be produced in the US and Qatar.

The European Commission stated last week it was looking at “various options” to ensure sufficient gas is in storage once the EU’s existing gas storage regulation (which was adopted in June 2022 and requires member states to meet mandatory storage filling targets) expires at the end of 2025.

The front 6 Seasons are up versus /1-week/1-month/3-months/6-months ago – so it’s safe to say Forward prices are at the top of the market.

The front 4 Seasons are all up versus this time last year following a summer of geopolitical turmoil.

Day-Ahead prices remain more expensive than Month/Quarter-Ahead, reflecting sentiment that prices are likely to fall as we approach the summer shoulder (Mar-25).

Monthly Day-Ahead averages for this month saw an expensive weekend off the back of low temperatures/poor renewables generation – 120.194p/therm (or approx. 4.101p/kwh excluding non-gas).

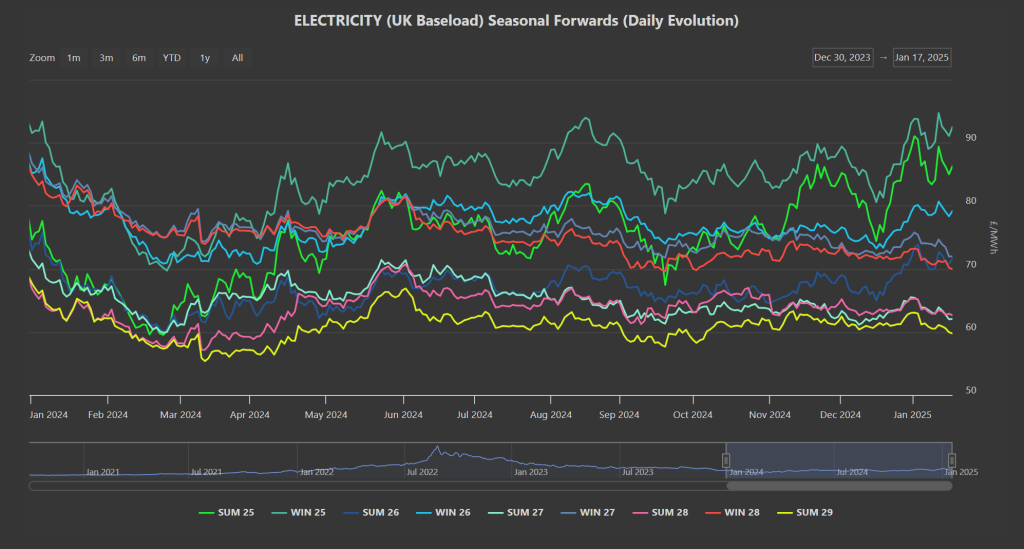

ELECTRICITY & CARBON

As is always the case (to a greater or lesser degree), UK electricity prices are mirroring gas moves – though swings are less impactful (given that end-users pay more for “non-electricity” these days, than for the commodity itself).

Today’s UK’s electricity generation mix is again bullish (and price supportive) in nature with renewables contributing only 12%, whilst thermal is at 59% (gas and coal) and low carbon at 15% (nuclear and imports).

Monthly Day-Ahead averages for this month so far reflect wind generation still well below seasonal norms (and increased gas-for-power burn) – £118.063/mwh (or 11.81p/kwh excluding non-energy).

On the Carbon markets, UKAs remain at a yawning discount versus EUAs – reflecting less scarcity of credits (with free allowances not scheduled to fall in the UK until 2027).

As we predicted, the illiquid bullish holiday period UKA rally lost steam as soon volume returned to the market – though prices have bounced off last week’s lows having bottomed out at £31.10/tn on the mid-price.

As the time of writing, the mid-price is now back up at £33.05/tn.