No surprises today, with near-term delivery prices still soft off the back of Storm Isha’s contribution to renewables outputs, with wind generation at 48% and gas-for-power burn down at 22%.

Down the curve, seasonal contracts continue their downtrend with milder, windier conditions forecasted.

Geo-political risk persists in the form of Middle East escalations and lingering worries over supply disruption in the Red Sea/Suez Canal.

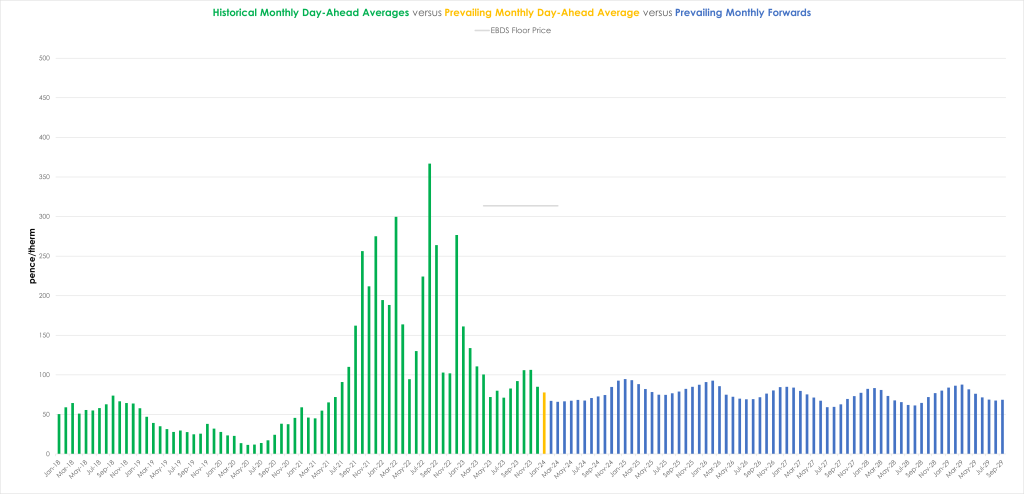

Monthly Day-Ahead averages are on target this month to achieve 79p/therm (or 2.7p/kwh).

ELECTRICITY & CARBON ALLOWANCES

Looking to the continent, European near-term delivery prices have plummeted, driven down by a steep rise in renewables outputs and higher temperatures expected to persist over the coming days.

Mild and windy weather will keep prices under pressure until at least Thursday when wind outputs are forecasted to fade.

Today’s overall bearishness of the wider energy complex hasn’t spared the EUAs (European Carbon Allowances), with the Dec-24 benchmark contract testing the two-year low – driven in the main by anticipation of less need for thermal power plants.

Likewise, consensus is building that UKAs (UK Carbon Allowances) may settle as low £30/tonne this week at Wednesday’s auction.

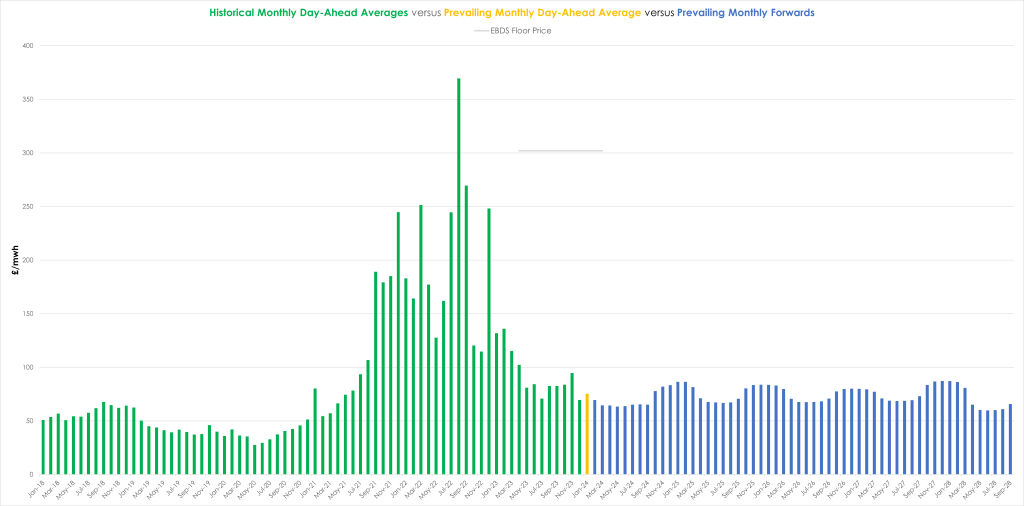

UK electricity monthly Day-Ahead averages are on target this month to achieve £75/mwh (or 7.5p/kwh).