Not surprisingly, European markets ‘gapped-up’ (opened already higher than Friday’s close) this morning following America’s bunker-busting attacks on Iran’s nuclear facilities over the weekend.

The risk being built-in to prices by market participants are being driven by fear over how Iran may respond i.e., will they carry out their threats to close the Strait of Hormuz (SoH)?

Iran’s state-run television reported that parliament has voted for the closure of the SoH – potentially impeding the transit of around 20% of global LNG export.

For the time being however, vessels are still crossing the waterway whilst Iran’s Supreme Leader mulls over his next move.

If he were to sanction the closure of the Strait, Iran would lose vital oil revenues, as well as seriously damage their relationship with China (it’s primary oil customer).

Moreover, any decision to disrupt oil and gas deliveries would likely offer America even more reasons to seek to bring about regime change (given Trump’s well-touted goal of lower inflation, which of course requires lower oil prices).

So, for Iran, whilst they’ve now been subject to direct attack by the Americans, their dilemma is unchanged since Friday – as such, whilst prices have certainly crept up, the rise has been tempered by an underlying belief amongst traders that closure of the Strait of Hormuz by Ayatollah Ali Khamenei could turn out to be an own goal.

Looking at key fundamental drivers for a moment, the UK system opened long this morning (supply outstripping demand forecast) helped primarily by the conclusion of seasonal Norwegian maintenence.

Norway’s Langeled pipeline is nominating flows at 150% the levels delivered on Friday – this amid very good wind outputs and low gas-for-power generation.

In other words, if the UK were not so heavily reliant on the vagaries of LNG delivery, we’d likely be seeing prices drop-off today.

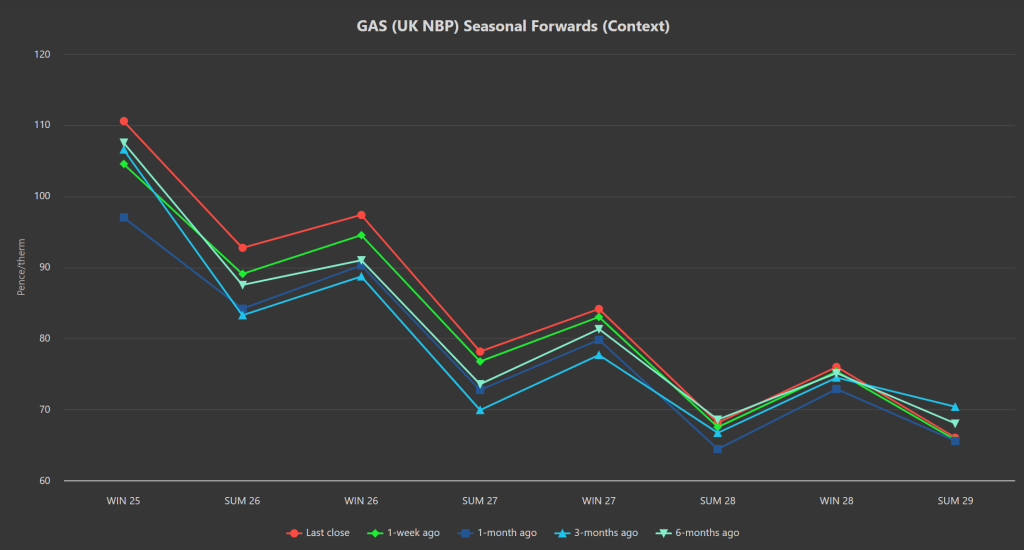

However, geopolitical impacts that potentially limit LNG arrivals to Europe (or heighten global competition for cargoes) have driven Winter-25 gas prices back up to 110p/therm (last seen in Feb-25).

European storage is expected to benefit from good renewables outputs (amid improved Norwegian flows) this week, so all things being equal we should see good injections and fullness levels creep up this week (currently at 56% versus the 5-year average of 63%).

On the trading side, clients running flexible capability are mostly watching from the sidelines as the Israel-Iran conflict unfolds.

This month’s UK gas Day-Ahead averages are at 89p/therm (or approx. 3p/kwh excluding non-gas) – so benchmark prices have been rising day-on-day for most of the month.

Seasonal Forwards are up versus 1-week; 1-month; 3-months; 6-months ago – please see chart below.

ELECTRICITY & CARBON

Electricity prices are mirroring gas increases.

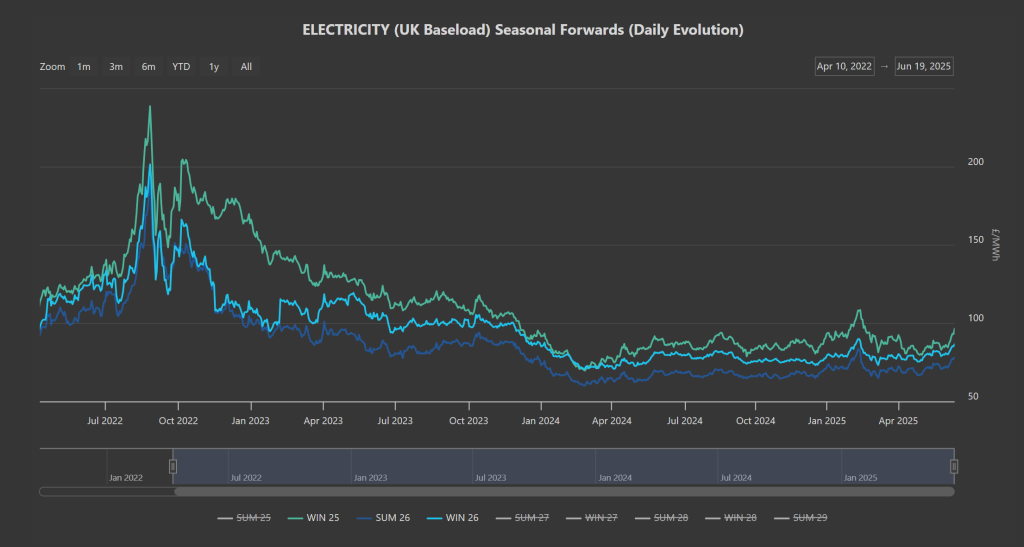

Winter-25 is at £96.8/mwh (so an increase of 20% versus the lows we saw back on 1st May).

To put recent increases into a longer-term perspective, please see chart below detailing the evolution of prices for the front-seasons (Winter-25/Summer-26/Winter-26) dating back to the energy crisis of Aug ’22 i.e., we’re thankfully still seeing prices all the way down the curve below £100/mwh (or approx. 10p/kwh excluding non-energy).

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

As such, prices have dropped steeply from last week’s highs off the back of improved renewables and an expectation that Europe’s 2040 carbon reduction target this week will get lost in the noise of global conflict.

Today’s UK electricity generation mix is very bearish in nature reflecting benign ‘summery’ weather conditions, limiting gas-for-power burn – specifically, renewables are contributing 68%, thermal at 6% (gas and coal) and low carbon at 16% (nuclear and imports).

Electricity Day-Ahead averages for the month have actually fallen over the last few days – currently at £66/mwh (or approx. 6.6p/kwh excluding non-energy).

On the trading side, clients running flexible capability are mostly watching from the sidelines as the Israel-Iran conflict unfolds.