With the onset of Summer-25 now only 8-days away, temperatures across Europe/the UK this week are forecast to remain at or above seasonal norms.

Indeed, the sun is shining, and warmer/windier conditions prevail for the time being – limiting gas-for-power burn and storage withdrawals amid improved renewables outputs.

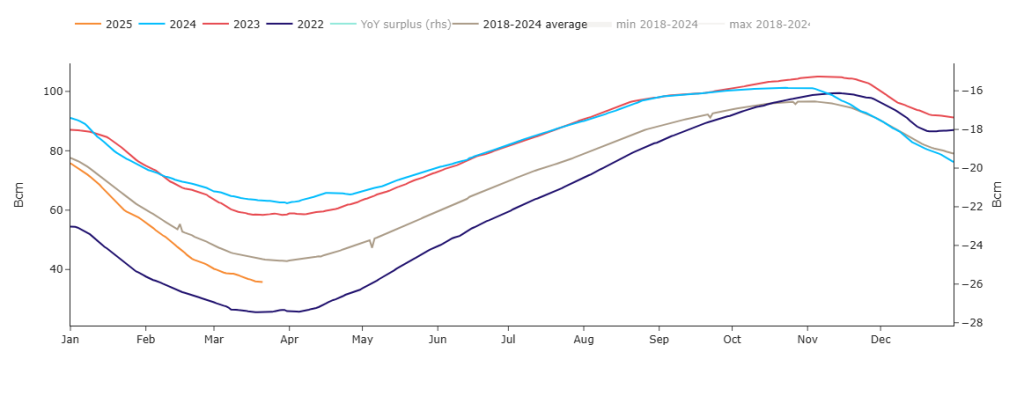

Whilst Europe’s storage fullness remains on the low side, early signs of summer conditioning (and an end to the “heating season”) has meant several countries have now started injecting gas back into storage (please see chart below detailing current storage below the 6-year average at 34%).

The stresses and strains caused by the end of the Russia-Ukraine transit agreement (at the turn of year) persists – increasing still further our reliance on LNG arrivals over the coming months to replenish gas inventories in time for Winter-25.

However, for now, LNG arrivals remain in good shape – though with the falling prices in Europe, the JKM spread increasingly points toward Asia becoming a more profitable destination for cargoes – so Industrial buyers need to bear in mind over the coming weeks/months that prices can only realistically fall just so far (as we need to keep prices high to ensure continuous LNG imports).

That said, the US is unlikley to be sending LNG to China given the high costs to do so (in light of Trump’s tariff war) – so Europe should be a welcome benificiary.

All eyes remain on the US/Russia negotiations in Saudi Arabia again today – if Russian pipeline comes back online any time soon, global competition for LNG will subside and prices will inevitably fall.

Nonetheless, last week’s price volatility caused by a major explosion at the Sudzha metering station on the border between Russia and Ukraine makes the prospect of a quick resumption of Russian flows via Ukraine less likely in the near-term.

Rumours abound that Naftogaz (the Ukrainian state-owned gas producer) is looking to partner with private UK businesses to help increase natural gas production across Ukraine – so efforts continue to be made to identify new gas reserves across Europe to further weaken Putin’s ability to spread disharmony.

Monthly Day-Ahead averages for this month so far are on track to improve on last month’s final number (124p/therm), with averages holding steady at 103p/therm at the time of writing (or approx. 3.5p/kwh excluding non-gas).

ELECTRICITY & CARBON

Electricity prices continue to mirror gas movements, with summer delivery prices down the curve looking increasingly attractive to buyers with FLEX capability.

Today’s UK electricity generation mix is marginally bearish in nature, with renewables contributing 39%, thermal at 31% (gas and coal) and low carbon at 22% (nuclear and imports).

On the Carbon markets, EUAs and UKAs (European and UK mandatory allowances for heavy emitters) had reversed all last month’s gains off the back of multiple bearish drivers including milder temperatures, slowly improving renewables outputs, rumours of a potential Ukraine-Russia peace deal, increased tariffs and soft macroeconomic data.

However, with the partial resurgence in near-term gas prices last week, Carbon followed suit.

As it played out (and as we predicted), bearish divergence late last week on the RSI (relative strength index, a momentum indicator) signalled a potential period of consolidation or trend reversal.

Accordingly, prices have indeed fallen back with the mid-price now at £45.11/tn (please see chart below).

UK electricity Monthly Day-Ahead averages so far for this month are holding steady below £100/mwh at £92/mwh (or approx. 9.2p/kwh excluding non-energy).