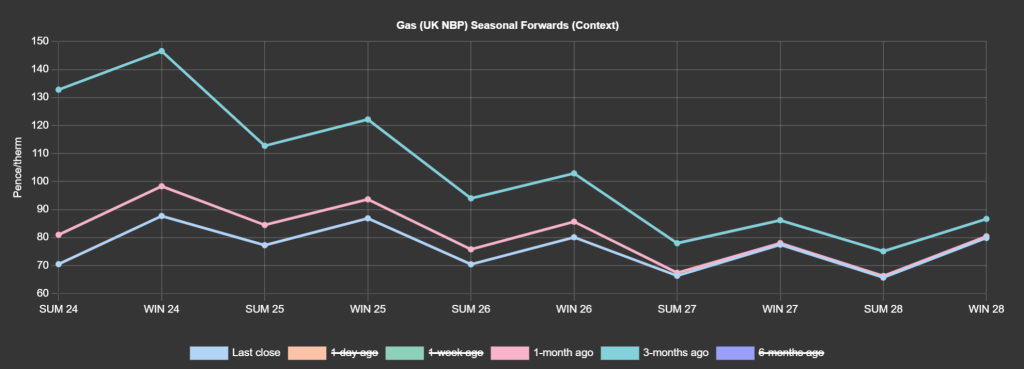

Despite our being at the height of Q1 winter conditioning, Seasonal Forwards are down versus 1-month ago/3-months ago (see chart).

However, markets have been marginally firmer today off the back of a short system (demand outstripping supply) amid news that the Freeport LNG terminal in Texas expects Train 3 to be out of service for about a month due to an electrical fault.

In other bullish news, unscheduled maintenance at the Cygnus gas field in the UK is likely to last until the weekend.

Controversially, President Biden has announced a pausing of any new licences for LNG projects – lest we forget, Europe’s supply mix has grown increasingly reliant on LNG in the absence of Russia’s pipeline flows so it’s likely markets are finding support at the risk of increased scarcity.

Temperatures and wind outputs above seasonal norms are forecast to continue into early February and should keep a lid on any meaningful upside caused by geo-political risk across the Middle East.

Monthly Day-Ahead averages are on target this month to achieve 75p/therm (or 2.5p/kwh).

ELECTRICITY & CARBON ALLOWANCES

Looking to the continent, near-term delivery prices remain fairly uniform across NW Europe – though we may see regional disparities over the coming days with higher wind outputs in certain areas.

Also, temperatures are forecast to be close to 4°C above seasonal norms – reducing heating demand and gas-for-power burn.

European carbon prices are trading in a tight range after losing over €17/tonne since the beginning of the year and finding decent support around €60/tonne.

Last week’s COT (Commitment of Trader’s Report) highlighted that market participants are doubling down on their short positions despite already oversold conditions – leading some contrarian traders to warn of upside caused by a short squeeze!

However, bears are hoping we could see prices retesting the lower €60/tonne levels thanks to milder weather over the coming weeks and, of course, limited need for thermal generation.

Back in the UK, our generation mix is bullish with 50% gas-for-power burn and 18% renewables.

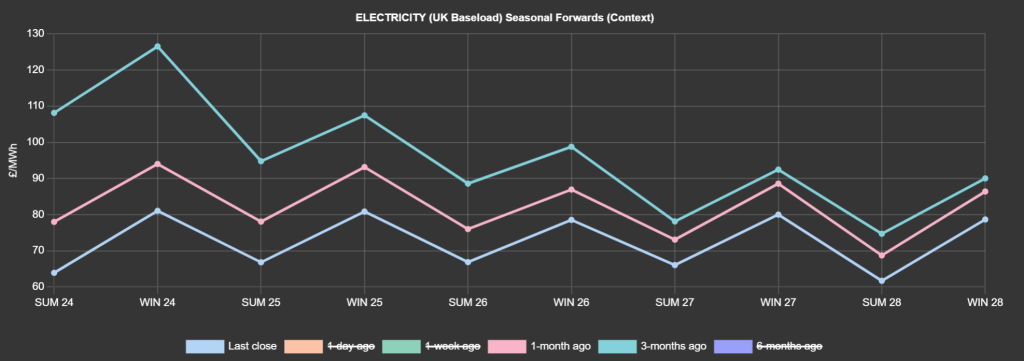

UK electricity monthly Day-Ahead averages are on target this month to achieve £72/mwh (or 7.2p/kwh).