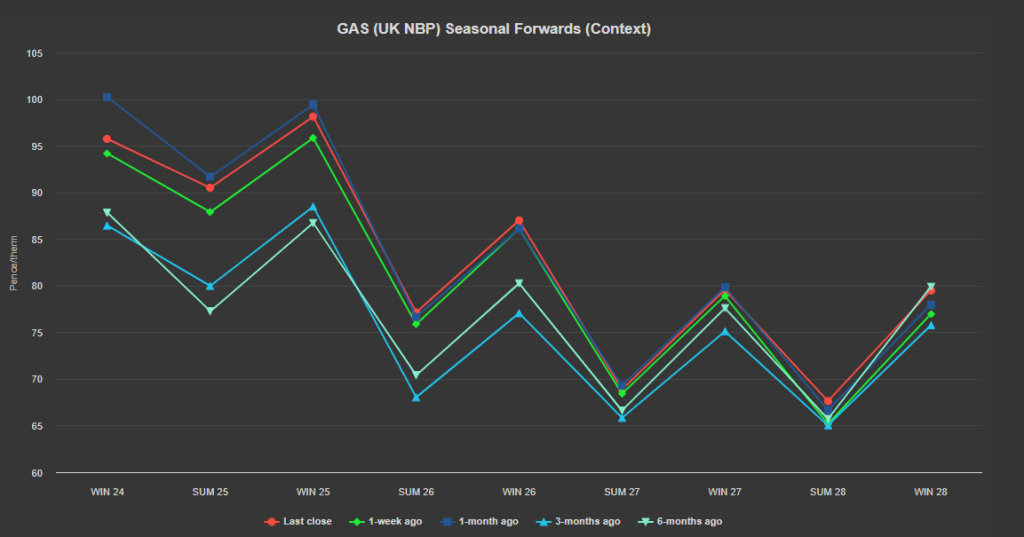

Seasonal Forwards remain down on the month, but up on the week/3-months/6-months ago – see chart.

Markets saw very marginal gains last week off the back of supply tightness fears – primarily attributed to the lingering doubts over Freeport LNG’s production outputs.

That having been said, over the weekend the numbers coming out of the facility look to have improved a little.

Whilst prices opened this morning unchanged from Friday’s close, they’ve since firmed amid concerns that Middle East tensions are about to escalate.

Likelihood of further conflict have been heightened following more missile strikes in the region.

Israeli authorities have claimed that at least 11 people were killed and 37 others injured in the northern part of the occupied Golan Heights on Saturday – Hezbollah is being blamed, though has yet to claim responsibility.

The increased tension and fears over further impediment to LNG transit through the region is adding more risk premium this morning.

By way of limiting upside, the UK is set for some above seasonal norm temperatures over the coming days – mitigating gas-for-power burn.

Looking at the big picture, with demand low, and supply comfortable, replenishing gas stocks is not posing any problems.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24) – though LNG delivery remains tight against a backdrop of sustained high temperatures across Asia (and the associated cooling demand).

European storage is at 84% fullness versus the 5-year average of 72%.

On the hedging side, we’re now on the other side of Summer-24 – with 120 days having elapsed, and 64 remaining.

Clients with open volumes for Winter-24 are increasingly scaling-in so as to avoid any loss of prevailing value.

Monthly Day-Ahead averages so far this month are on target to achieve 75p/therm (or circa. 2.5p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices rebounded on Friday, mainly supported by the expected drop in renewable generation this coming week.

On the Carbon markets, EUA prices increased slightly on Friday, trying to maintain the uptrend that started from 22nd July in the wake of rising gas prices.

Back in the UK (and despite EUA’s technical repositioning), UKAs (UK Carbon Allowances) continue to fall (as indicated by RSI divergence and confirmed descending trend channels) – now trading at circa. £39/tn.

At the time of writing, our electricity generation mix is bearish in nature today with renewables contributing 43%, thermal at 12% (gas and coal) and low carbon at 29% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £69/mwh (or circa. 6.9p/kwh excluding non-energy).