Traffic through the Strait of Hormuz has slowed following Friday’s flare-up (but not stopped).

As such, markets opened marginally higher, but are now treading water.

Prices remain confined within the comparatively tight range seen throughout the back end of last week.

Market participants are mostly adopting a wait-and-see approach, looking for greater clarity around potential peace negotiations, and whether Qatar will/can increase its export volumes.

At the same time, with each day/week/month that passes, pressure is building on Europe to restock gas inventories ahead of the Winter-26 heating season, with storage levels still notably below the seasonal norm (now at 48% versus the 5-year average of 60%).

For now, both the US and Iran have agreed to pause hostilities – again.

As far as we can tell, the most likely cause for Iran’s drone attack on a Singapore-flagged oil tanker on Friday was frustration – not at the US, but at Oman.

Oman’s decision to open a shipping corridor through the Strait of Hormuz is weakening Tehran’s leverage over the strategic waterway – so they opted to bomb a ship as it exited the Strait (that had used Oman’s corridor to achieve safe transit).

The US then retaliated by attacking multiple strategic targets across Iran.

Then, Iran retaliated by launching missile attacks toward US bases in Kuwait and Bahrain.

In reponse, the US attacked still more strategic targets across Iran yesterday.

As of this morning, the uneasy truce resumed, and it’s as you were.

On the FLEX side, traders continue to buy in the dips – we expect for markets to soften as the week progresses (as we don’t think it’s a coincidence that all parties seem prone to act when markets are closed at weekends!)

If you’re waiting on Trade Confirmations, please bear with us whilst our Trading Desk times market entries/buys in the dips.

Looking at the big picture, the gas market remains underpinned by strong supply-side fundamentals, with rising Norwegian flows and resilient system length (supply outstripping demand forecast).

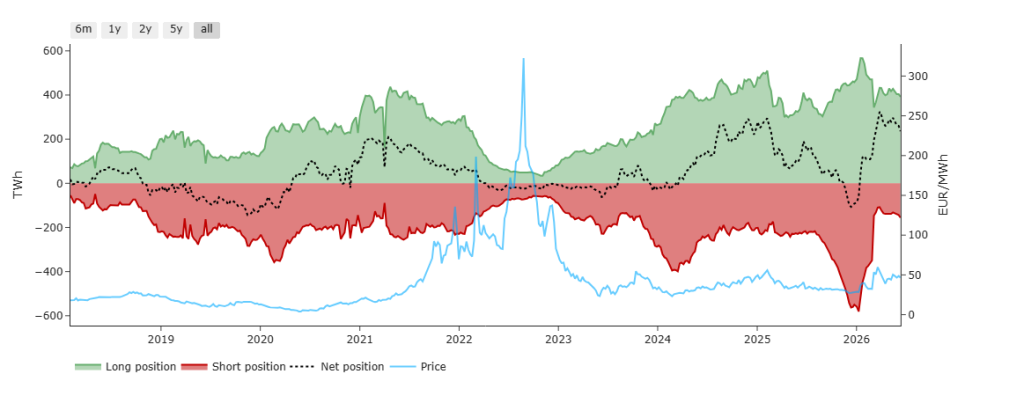

Last week, I commented that even though traffic through the Strait of Hormuz was resuming, the smart money (Investment Funds) were likely to wait for a rise in Qatari LNG exports, and/or a significant rebound in European LNG imports before we see a further sell-off – as per the chart below detailing Investmenet Fund Net Position vs TTF (European gas benchmark), that sell-off remains pending.

UK gas Monthly Day-Ahead Averages for June so far have fallen to 109 p/therm (or 3.7 p/kwh exc. non-gas).

ELECTRICITY & CARBON

UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb – primarily due to summery conditions, solid renewables outputs (meaning lower gas-for-power generation).

Indeed, today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 43%, thermal at 21% (gas and coal) and low carbon at 21% (nuclear and imports).

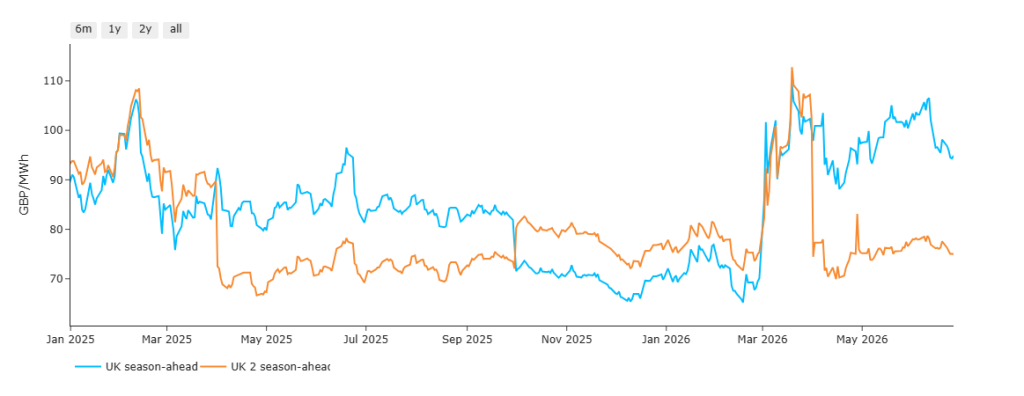

The chart below details UK electricity Season-Ahead and 2-Seasons-Ahead prices at Friday’s close.

By way of explanation, right now, Season-Ahead is Winter-26 and 2-Seasons-Ahead is Summer-27.

Notably, when compared to this time last year, 2-Seasons-Ahead is almost at parity (whilst Season-Ahead is significantly higher than this time last year) – reflecting an underlying sentiment amongst market particpants that markets will return to pre-war levels.

On the FLEX side, traders continue to buy in the dips – we expect for markets to soften as the week progresses (as we don’t think it’s a coincidence that all parties seem prone to act when markets are closed at weekends!)

If you’re waiting on Trade Confirmations, please bear with us whilst our Trading Desk times market entries/buys in the dips.

On the Carbon side of things, mid-price Dec-26 UKA delivery is at £56.42/tn (and the spot is at early 55s) mirroring softer gas prices.

There are also whispers that a potential broader EU policy shift may already be underway – favouring global competitiveness over the limitations of climate action.

UK electriity Monthly Day-Ahead Averages for June so far are holding steady at £93/mwh (or 9.3 p/kwh exc. non-energy).