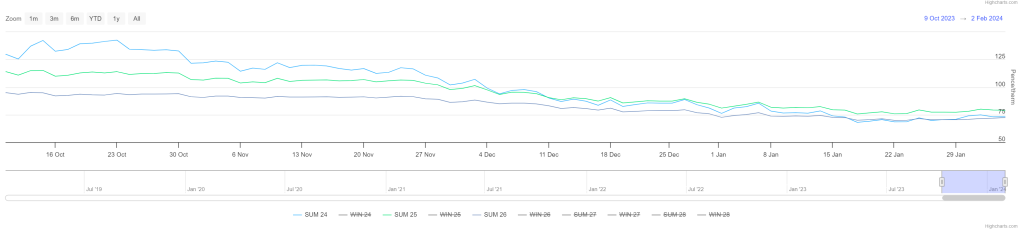

Prior to 12th Dec ’23, one has to go all the way back to early 2021 to find a day when Summer-24 was cheaper than Summer-25/Summer-26 delivery (see chart) – evidence, surely, that markets have priced-in significantly diminished risk for the mid-term (versus increased risk thereafter).

Prices were a little firm at this morning’s open off the back of a short UK system (demand outstripping supply) – though, at the time of writing, prices all the way down the curve have drifted back below Friday’s close.

In short, we’re in a tight trading range with key drivers well-balanced i.e., European storage is high (69% versus 5-year average of 58%) but Norwegian flows are weakened by unscheduled outage; underlying confidence persists that we’ll finish Winter-23 with more than 50% storage left in the tank but geopolitical tensions persist in Russia and across the Middle East.

Demand is below seasonal norms today against a bearish backdrop of 51% renewables output (48.5% wind) and only 10% gas-for-power burn.

Things are heating up between the US and Iran with three US soldiers killed and about 40 others injured in a drone attack by Iran-linked groups on the military base known as Tower 22 near the Jordan-Syria border on Sunday.

We’re told to expect “waves” of US retaliation…

Monthly Day-Ahead averages are on target this month (so far) to achieve 70p/therm (or circa. 2.4p/kwh).

ELECTRICITY & CARBON ALLOWANCES

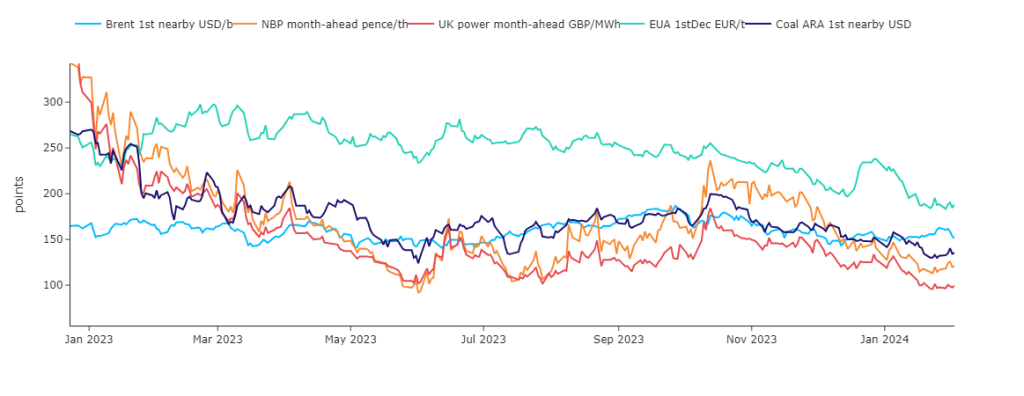

When comparing relative values of the wider UK energy complex beginning Jan-23 (measured in Base 100), gas and baseload electricity still remain below oil/coal/carbon (see chart).

Looking to the continent, near-term delivery prices closed down on Friday off the back of forecasts of soaring wind outputs and above-average seasonal temperatures.

On the horizon, attention is keenly focused on forecasts of colder weather and a fall in wind generation for the back-end of Feb.

Temperatures will likely drop to 2.5°C below seasonal norms from 15th Feb, while wind outputs in Germany are expected to hover at or below 20GW during that period – no doubt resulting in heightened thermal power production (gas-for-power/coal).

Carbon observed the correlation coefficient with gas on Friday, with the EUA Dec-24 benchmark contract tracking rising gas prices to climb above its 5-day moving average (and eventually close the week with little change from the previous one).

Over the coming week, European/UK emissions markets are likely to focus on both weather and regulatory developments – the European Commission is expected to disclose its proposal for the EU 2040 emissions reduction target.

Prices have been rangebound over the past few weeks – supported/pressured by short traders and the bullish impacts of risk.

Several market participants noted that speculators might have maxed out their net short position for now – forecasts of colder and calmer weather explains the well-balanced consolidation of prices.

Back in the UK, monthly Day-Ahead averages are on target this month (so far) to achieve £51/mwh (or 5.1p/kwh).