As has been our assertion across Winter-24, the hysteria over gas storages has been overcooked – Summer-25 is upon us, and prices are sliding across the board.

Trump’s tariffs (if sustained) will inevitably lead to global economic slowdown.

Stock indices across the world are revaluing downwards, investor safe havens (gold/bonds) are seeing higher values/lower yields, and gas (& electricity/carbon) are very much on the slide (anticipating Industrial demand destruction).

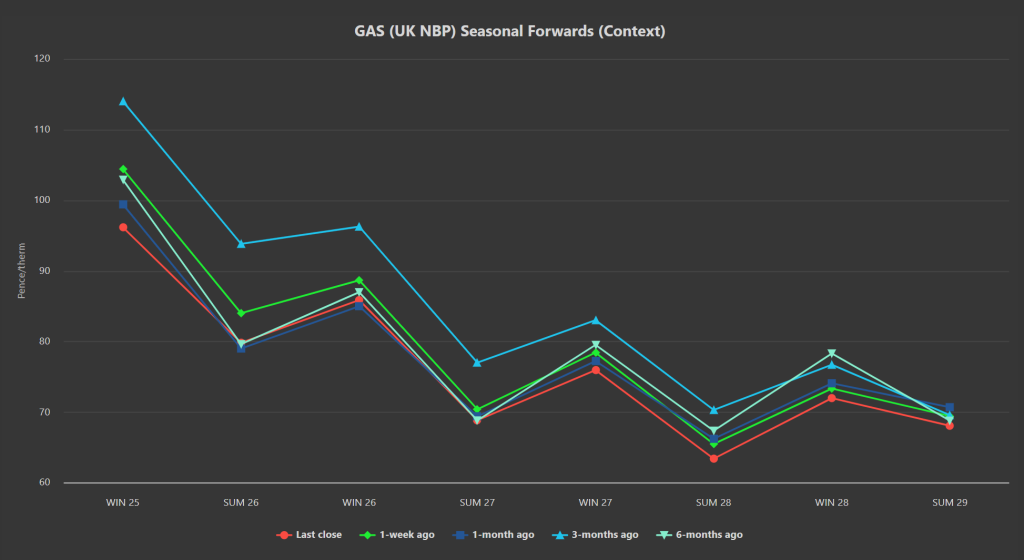

For the first time since Q124, Seasonal Forwards all the way from front to back are down versus 1-week/1-month/3-months/6-months ago (please see chart below).

China has stopped importing US LNG amid retaliatory tariffs, falling demand (and decidely shaky economic numbers) – as such, LNG cargoes are heading to Europe (and European prices can afford to fall if competition from Asia is subdued).

In addition, the UK system opened long this morning (supply outstripping demand forecast) and temperature forecasts have been revised upwards for the back half off this week (limiting heating demand).

Before we get too excited at the prospect of lower prices for Industrial buyers, poor wind outputs look to be accompanying the warmer weather – so storage withdrawals will persist for a little while yet.

European storage fullness is at 35% versus the 5-year average of 42% (so not too far off the pace).

The spread between Summer-25/Winter-25 prices is slowly widening, making it more viable for traders across EU nations to stockpile in advance of the mandated 90% by 1st Nov.

All things being equal, if we can have a lighter maintenance season across Norway this summer (than has been the case over the last few years), then the coming months will inevitably see significant prices falls across the board.

FLEX clients are under no pressure to pull the trigger immediately, though we encourage buyers to assess the solid comparative values currently available down the curve, and to start drawing lines in the sand for respective periods of delivery (i.e., how do prevailing Forward prices compare to current hedged prices, and what are your price targets for near/mid/far-term?)

This month’s gas Day-Ahead averages are at 93p/therm (or approx. 3.2p/kwh excluding non-gas).

ELECTRICITY & CARBON

Electricity values look increasingly solid, with ALL Seasonal Forwards below £85/mwh (or 8.5p/kwh) at the time of writing.

As per our technical prediction for Carbon last week (given the persistent correlation to fossil fuels), EUAs and UKAs have now fallen through support – not great news for the institutional investors/speculators who remained net long!

With the slide now picking up momentum, stop losses are being wiped out and the bear rally is gaining traction (as a rule of thumb, markets fall twice as quickly as they rise).

Compliance buyers will be eyeing up value at £38/tn at the bottom of the current bearish trend channel (see chart below).

Today’s UK electricity generation mix is neutral, with renewables contributing 26%, thermal at 32% (gas and coal) and low carbon at 25% (nuclear and imports).

So far this month, electricity Day-Ahead averages are on target to achieve £74/mwh (or approx. 7.4p/kwh excluding non-energy).