This morning, following the Easter weekend, European prices opened lower but are rising incrementally as the morning wears-on – with Trump’s deadline looming.

The US President has either painted himself into a corner, or is entirely committed to his course of action – this time tomorrow, we’ll know for sure.

The latest, and heavily-trailed, deadline for Iran opening the Strait of Hormuz ends at midnight tonight (GMT).

Following a weekend of social media posts replete with expletives, and blanket global media coverage, should Trump fail to follow through with his threats to “decimate” Iran’s bridges and energy infrastructure, then surely his authority will be irreparably discredited – both at home and abroad.

Over the course of the last five weeks, Trump has set deadlines, made demands, and issued threats – but, to date, none have been as explicit as what’s been coming out of the White House over the last twenty four hours.

And so, with the world watching, and with markets holding their breath, we await to see how things play-out at midnight – at best, Trump backs out amid more urgent diplomacy.

At worst, the US attacks and Iran fires missiles across the Gulf aimed at key LNG infrastructure.

Many maintain, however, that Trump’s bellicose rhetoric is just that – rhetoric.

And privately, he’s still casting around desperately for an off-ramp/end-game that will not expose him to accusations of war crimes (should he go ahead with the deliberate destruction of civilian infrastructure).

“They have till tomorrow,” Trump said last night – “we’ll see what happens. I believe they’re negotiating in good faith. I guess we’ll find out” – and yet, Iran continues to deny any meaningful negotiations are happening.

Since the US/Israeli offensive began back on 28th Feb, Iran has yet to allow even a single LNG carrier to transit the Strait of Hormuz.

Tracking data shows LNG vessels just idling in the area, underscoring the sustained (and worsening) disruption to global gas flows.

Brent crude is back up to £113 this morning – reflecting increased risk-premium across oil futures.

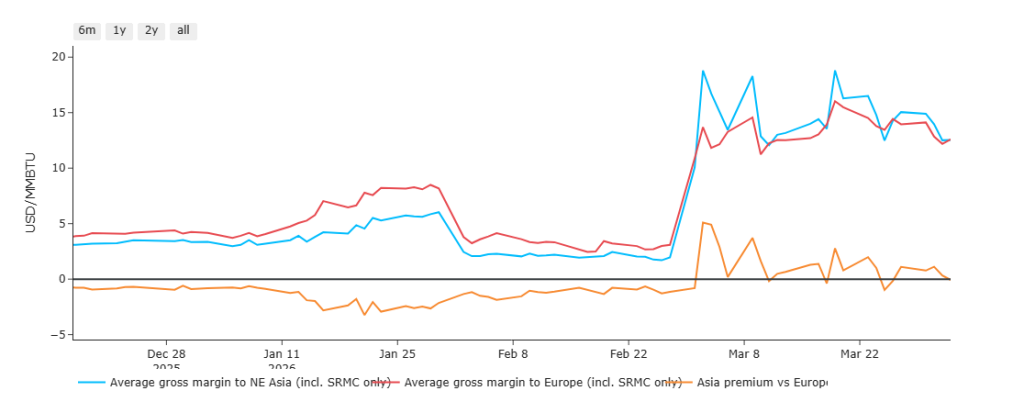

The chart below details the profitability of cargoes heading to Asia versus Europe – worryingly, beginning early March, vessels can expect to make more money heading to Asia than they can to our shores.

This is of course a direct outcome of the Strait of Hormuz remaining closed (given that most of the LNG heading through the waterway is headed for Asia).

Monthly Day-Ahead Averages for UK gas for the month so far are holding steady at 124p/therm (this versus last month’s final Monthly Day-Ahead Average of 130p/therm).

ELECTRICITY & CARBON

Thankfully, UK electricity prices remain at a significant discount versus gas prices (given summer conditions/improved renewables outputs/falling gas-for-power burn).

On the Carbon side of things, Dec-26 UKA delivery remains uncoupled from gas volatility with prices touching levels that are 34% below those printed in mid-Jan amid fears that Trump’s war on Iran is slowing global economies (and, in so doing, Industrial outputs).

At the time of writing, UKA mid-price Dec ’26 delivery is at £40/tn (and the spot is at mid-39s).

Since the US/Israeli offensive began, gas price falls are met with rising UKAs – and vice versa.

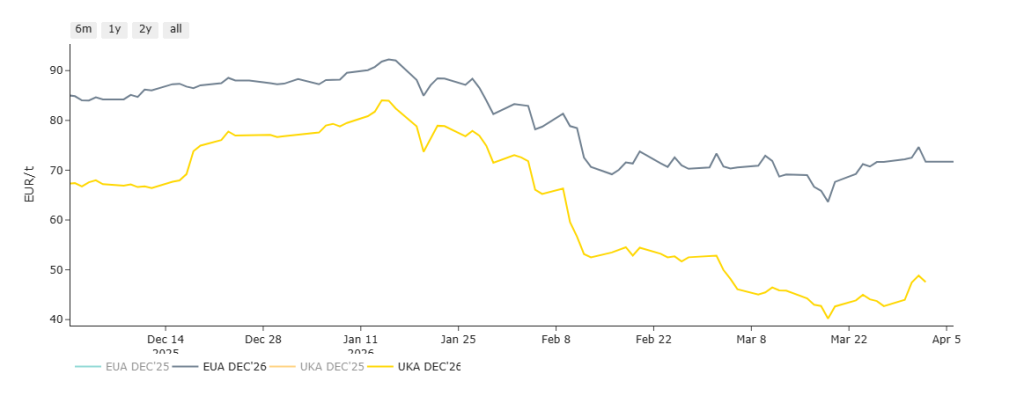

The chart below shows UKAs still at a significant discount versus EUAs.

This morning, UKAs are marginally lower than last week’s close – so expect a higher gas close!

Monthly Day-Ahead Averages for UK electricity for the month so far are at £86/mwh (versus last month’s final Monthly Day-Ahead Average of £105/mwh).