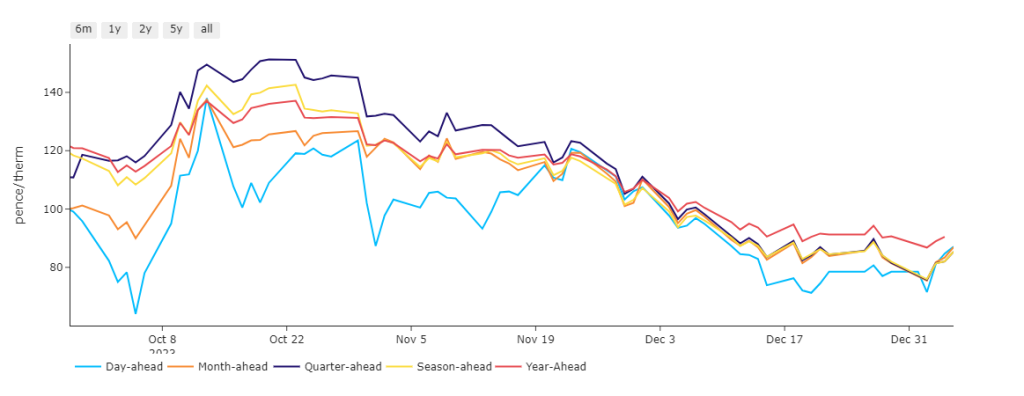

Day/Month/Quarter/Season-Ahead are at parity (see chart), with prices at the end of last week finding support driven by the prospect of a sustained period of lower temperatures and weaker wind outputs.

However, despite the fact that the UK’s gas system opened marginally short this morning (demand outstripping supply), prices at this morning’s open are actually down on last week’s close – reflecting an underlying confidence in supply dynamics.

Now that recent storm conditions have abated, LNG vessels have been able to berth and degasify at UK ports, significantly increasing flow into UK inventories.

Whilst we’ve inevitably seen some storage withdrawals over the last few days (given weaker renewables and higher gas-for-power-burn), storage numbers remain historically high – European fullness is at 85% versus the 5-year average of 72%.

Down the curve, contracts are also down on last week’s close, again reflecting market participants’ optimism that storage is sufficient (and supply is stable enough) to make it through the cold spell.

Norwegian gas flows remain above five-year averages with no outages reported across the gas fields.

Thanks to the re-opening of the Texas Freeport LNG terminal in Feb ’23 (and a newly operational terminal in Louisiana), America was named the world’s largest LNG exporter last year – shipping 15% more than record set in 2022.

Back in the UK, monthly Day-Ahead averages are on track this month to achieve 82p/therm (or 2.8p/kwh).

Outlook is NEUTRAL.

ELECTRICITY & CARBON

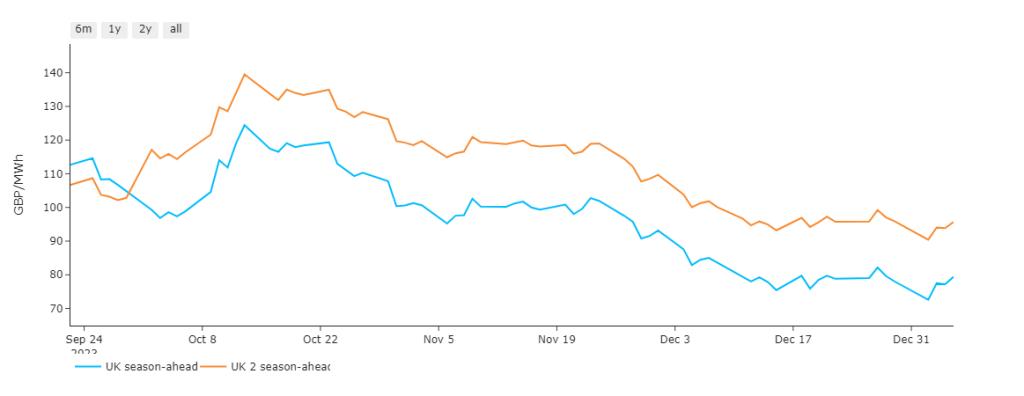

Following the chaos of ’21 and ’22, an orderly shape has now returned to Summer/Winter price differentials (see chart), with Summer-24 holding steady at a consistent discount to Winter-24

Looking to the continent, forecasts of rising solar generation and French nuclear availability offset part of some of last week’s bullish pressure.

Further weakening of wind generation and lower temperatures across Germany, the Netherlands and Belgium is likely to support Prompt (near-term delivery) prices today.

However, improved French nuclear availablity toward the end of the week should see bearish pressure keep a lid on any sustained upside.

Back in the UK, monthly Day-Ahead averages are on track this month to achieve £73/mwh (or 7.3p/kwh).

Outlook is NEUTRAL.

Carbon was little changed last week, with UK Allowances mirroring the ultimately directionless volatility of EUAs.

Notably, the COT (Commitment of Traders Report) showed a cut in speculators’ short (sell) positions in UKAs, but an increase in Industrial’s hedging actual allowances to offset their emissions.